On a sunny afternoon two years ago, as panic about the overheated housing market in Canada’s big cities was spreading, three key policy-makers hunkered down in Toronto to figure out what to do.

Federal Finance Minister Bill Morneau, Toronto Mayor John Tory and then-provincial finance minister Charles Sousa emerged with an acknowledgement that the housing market was indeed in a precarious state. They made a vow: they would try to take some action, but they would certainly not do anything that would make matters worse.

Morneau put a finer point on it. Government measures that would bolster the demand for housing were verboten. That’s because government helping out buyers would only drive prices up further, exacerbating the problem.

That vow hasn’t aged well, and now the federal government is thinking of jumping into the fray with budget measures on Tuesday to help young people to get into the housing market for the first time.

On the surface, there shouldn’t really be much of a public-policy problem any more. The housing market has cooled significantly in Toronto and Vancouver. Talk of a housing bubble wiping out homeowners’ wealth has quieted.

But to conclude that all is as it should be would be wrong.

In its most recent analysis of overheating in major cities across Canada, the Canada Mortgage and Housing Corp. (CMHC) concluded that there was a “high degree of overall vulnerability” at the national level, for the 10th quarter in a row. Vancouver, Victoria, Toronto and Hamilton are particularly susceptible.

More concerning — and this is where the federal budget comes in — is affordability. Real estate markets in the big cities may have backed away from the precipice, but prices are stabilizing at high levels. At the same time, the federal government has made it more difficult for homebuyers to qualify for a mortgage. And mortgage rates have risen.

At RBC, where economists have been measuring how affordable houses are at a national level and in big cities, its index is at the highest point since 1990. Put another way, homes are at their least-affordable point in almost 30 years. Average homeowners in Canada are putting 54 per cent of their family’s income towards carrying a house. In Vancouver, it’s 87 per cent. In Toronto, 75 per cent.

This means that moving to the big cities for a good job is unfathomable for many, unless they commute long distances or find substandard accommodation. There’s a growing concern that urban housing exacerbates income inequality, favouring those who already own homes in the cities to the detriment of newcomers, and to the detriment of companies hoping to hire new talent.

The federal Liberals believe the affordability problem is even worse for millennials, and point to recent research from CMHC that shows first-time homebuyers in the millennial age-bracket are stretched to the max. This group also happens to be fertile ground for Liberals looking for votes. Justin Trudeau’s victory in 2015 was thanks in part to new, young voters. And polling shows support among that demographic is still strong.

But the solutions are tricky, especially given the vow made two years ago to steer clear of bolstering the demand side of the equation.

The bubblelike conditions of Toronto and Vancouver are not yet a distant memory, and so policy-makers would want to avoid pushing markets in that direction so soon. And anything that would encourage homebuyers to take on debt is imprudent right now because the country’s dramatically high levels of household debt are probably Canada’s number one economic risk.

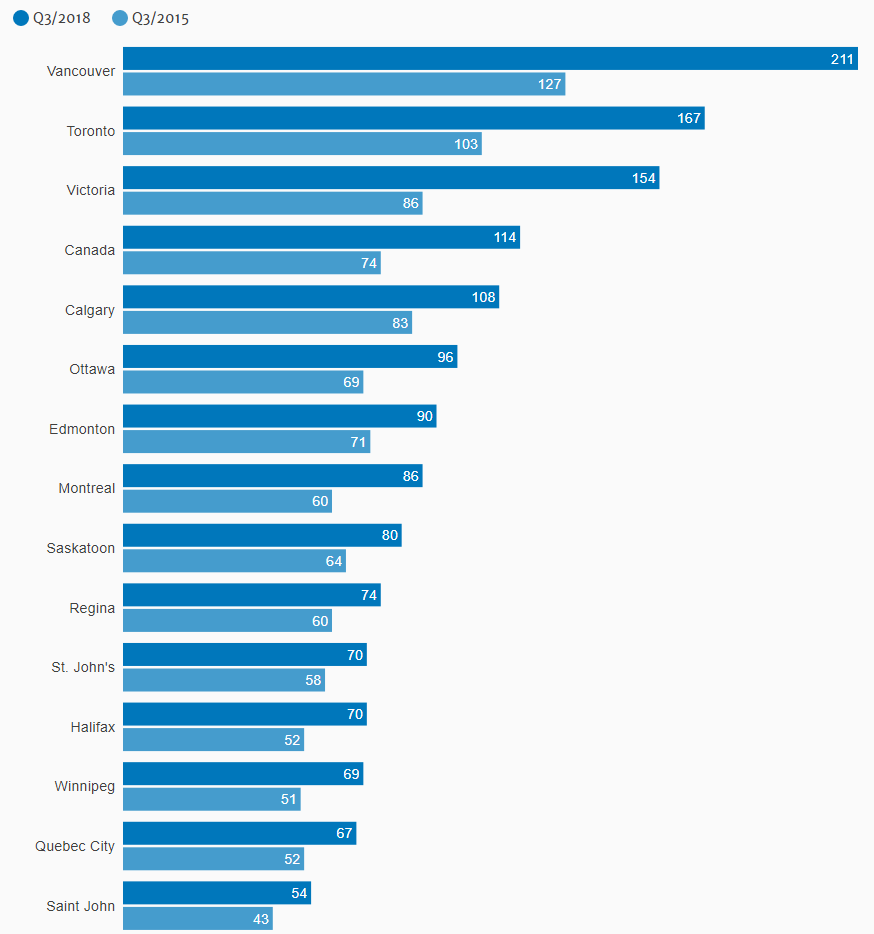

Canadian households now need much higher income to qualify to buy a home

Income required to cover the costs of owning an average home with a 25% down payment and clear the mortgage stress test, in thousands

However, pouring more federal money into building more homes — bolstering supply — is extremely expensive. The federal government has already earmarked $40-billion for housing over the next decade. Adding more, or speeding up its delivery, wouldn’t necessarily hit the specific demographics that the Liberals have in mind.

So the vow has been quietly revised, internally. Instead of “don’t touch demand,” it’s now “if you boost demand, you also have to boost supply.”

Some of the ideas have been around for a while: enhancing the ability of first-time homebuyers to use retirement savings for a down payment; or extending the length of time buyers can stretch out their mortgages.

There’s a new idea decision-makers are eyeing too: shared equity mortgages. Government would partner with certain first-time homebuyers in taking on a share — say 30 per cent — of a mortgage. When the time comes to sell the house, government would reap part of the reward, taking profits in proportion to its equity stake.

Unless, of course, there is no profit, and instead there’s a loss — posing a risk to the federal balance sheet. Given the political points to be gained, it’s a risk the Liberals may well be ready to take.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2