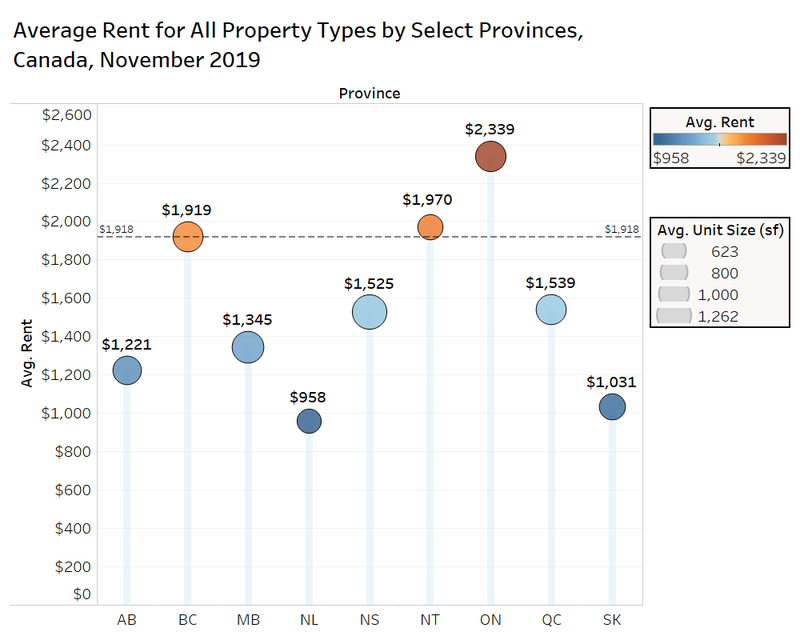

New year, no vacancy. Renters in cities across Ontario will spend another year struggling to find rental housing as prices continue to rise in the face of tight market conditions.

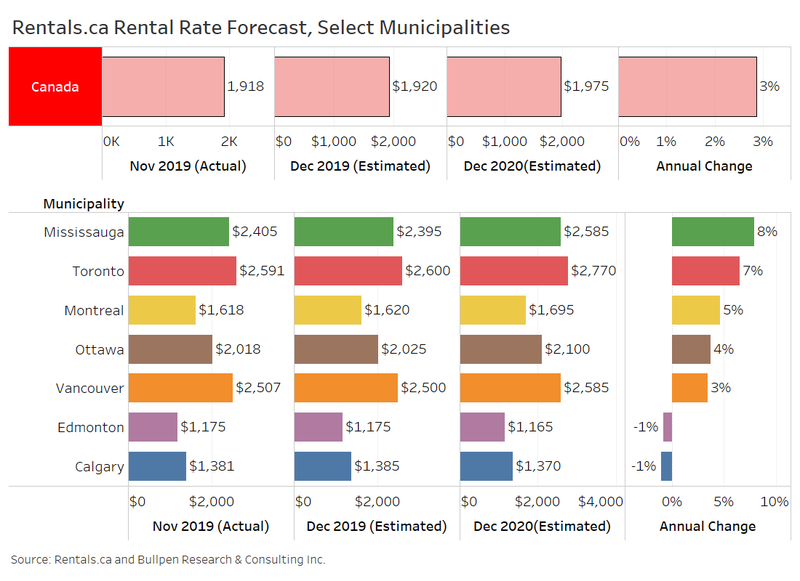

In 2019, the vacancy rate was 1.6 percent and it will likely drop further through 2020 to a near record low of 1.5 percent, according to Central 1 Credit Union economist Edgard Navarrete. For context, the vacancy rate for Ontario’s rental market averaged 2.6 percent between 1991 and 2018.

In his 2019-2022 housing forecast published at the end of 2019, Navarrete noted that the province has seen a substantial uptick in completed new rental units over the last three years. Through the same 1991 to 2018 period, the average number of new rental units added to the market was 1,500. From 2017 to 2019, the average increased to 7,000 units.

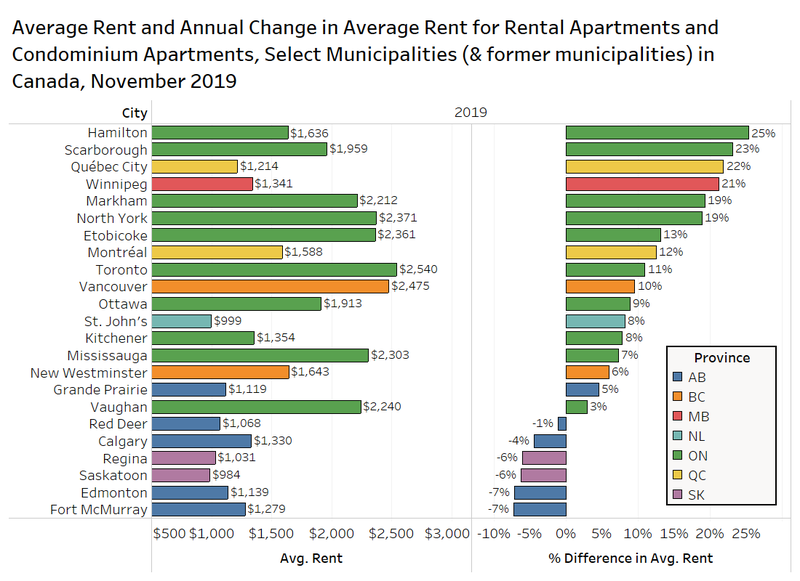

The trouble is that increase still doesn’t satisfy the demand for rentals in some of the province’s most competitive markets, especially Toronto, which is said to have the worst rental supply deficit in Canada.

“Government investments in rental housing will continue to add to the rental universe but expect [the province’s] rental vacancy rate to remain stubbornly lower than the long-term average due to continued strong demand from immigrants settling in Ontario and existing renters opting to remain in rental longer until they have a sufficient down payment to qualify for a mortgage loan,” wrote Navarrete in the Central 1 Housing Forecast.

Unfortunately, the main takeaway here for Ontario renters is monthly rents will continue to climb above inflation as long as this sharp disparity exists between rental supply and persistent demand. Navarrete singles out Toronto, Ottawa-Gatineau, London, Kitchener-Cambridge-Waterloo and Hamilton as markets where rental prices will log especially steep increases and bidding wars will keep intensifying. These cities will feel the strain on their rental markets particularly acutely because they are set to absorb the most new residents to the province.

There is hope for a rental unit supply uptick in the next few years, but for those looking for a new rental this year, it’s unlikely to offer much relief. The provincial government under Premier Doug Ford rolled back the rent control measures introduced by the Wynne Liberal government just a couple years earlier. With more flexibility to price rental units in response to market demand, investors are more likely to see condos as a solid long-term moneymaker and purchase units to add to the rental market.

These investor-owned condos are known as the “secondary rental market” since they are not built for the sole purpose of being added to the rental pool. Purpose-built rental units are known as the primary rental market.

The caveat is that the positive market changes this policy shift from the Ford government intended to inspire won’t be felt for at least a few years.

“If we see a large number of investors entering the market today, with the average completion time of high-density housing such as condo apartments anywhere from two to three years from the time shovels hit the ground, it wouldn’t be until after 2022 when the increased rental market supply will alleviate some of the pressures from the primary rental market,” wrote Navarrete.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2