Despite a strong start to the spring housing market in the Greater Toronto Area (GTA) in February, evolving conditions around the COVID-19 pandemic have had a profound short term impact on housing activity in the region. Among a slew of measures being announced at all three levels of government – including a number of initiatives in direct support of homeowners and renters – Ontario declared a state of emergency across the province on March 17 to help contain and minimize the spread of the virus.

As a result, housing market activity began to slow in reaction to these escalating measures and buyers and sellers began holding off on home sales and purchases amid uncertain health and economic circumstances. Using data from the Toronto Regional Real Estate Board (TRREB), Zoocasa reviewed how real estate market activity evolved in tandem with these emergency measures being put into effect.

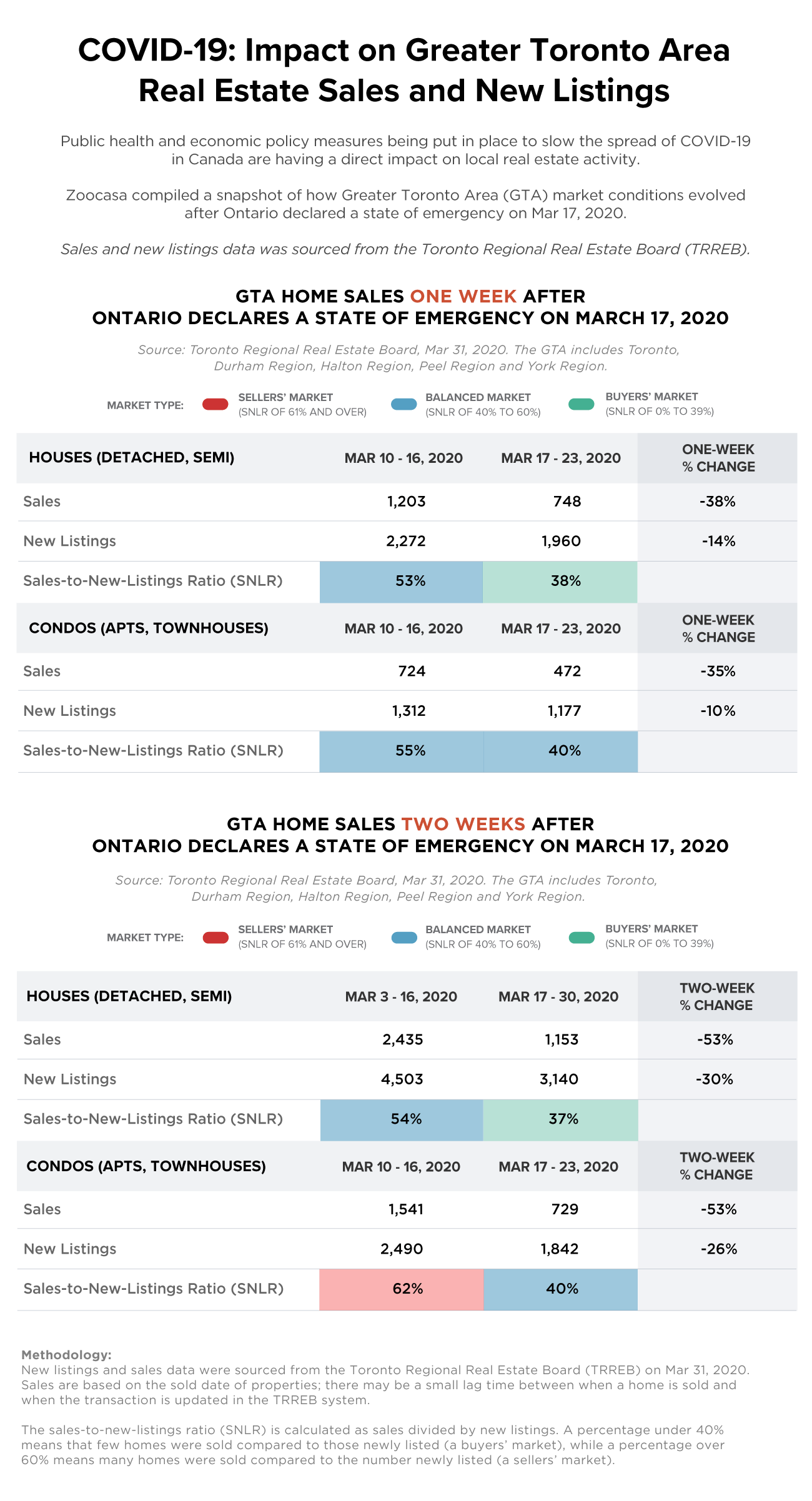

According to our calculations, the sales-to-new-listings ratio (SNLR) – a measure of market competition calculated by dividing the number of sales by the number of new listings – dropped to 38 per cent for detached and semi-detached homes in the GTA between March 17-23; compared to 53 per cent for the week prior to the emergency declaration. For condo apartments and condo townhouses, the SNLR dropped from 55 per cent to 40 per cent for the same time period. When the SNLR is between 40% – 60%, this indicates a balanced market, while above and below that threshold reveals sellers’ and buyers’ markets, respectively. As such, these numbers represent a visible shift in market conditions over a very short period of time.

Here’s a closer look at how GTA market conditions have evolved as we enter our third week under a state of emergency in Ontario.

One Week After: GTA House Market is Now a Buyers’ Market

With increased social distancing measures in place following the state of emergency declaration, there was a resulting 14 per cent dip in new listings for detached and semi-detached houses between March 17-23, compared to one week earlier. Sales were down 38 per cent from 1,203 to 748 sales on a week-over-week basis.

We saw a similar trend of fewer sales and listings unfolding within the condo market, which was enough to nudge the market slightly closer to buyers’ market conditions. For the week following the announcement, sales dropped 35 per cent for the same period, from 724 to 482, and there were 10 per cent fewer listings for condo apartments and townhouses compared to the week prior, dropping from 1,312 to 1,177, based on the listing entry date.

Two Weeks After: GTA Condo Market Borders on Being a Buyers’ Market

While real estate fundamentals indicate that housing demand will bounce back over the long term in major urban centres like Toronto, COVID-19 has caused an immediate slowdown in housing market activity and across the economy more broadly. Just two weeks following the announcement of a state of emergency, there was a noticeably visible impact on the house and condo market in the GTA.

Stronger health advisories coupled with directive recommendations to cease all in-person interactions from real estate bodies including the Ontario Real Estate Association, encouraged a 53 per cent drop in detached and semi-detached sales for the period between March 17-30. There were 1,153 sales during this period, compared to 2,435 between March 3-16. New listings dipped from 4,503 to 3,140, representing a 30 per cent drop.

In the condo market, sales dropped a whopping 53 per cent from 1,541 to 729, and new listings were down 26 per cent from 2,490 during the week of March 3-16 to 1,842 in the two weeks following the announcement. This was a swift shift from sellers’ market conditions between March 3-16 when the SNLR was 62 per cent, to market conditions bordering those of a buyers’ market just two weeks later where the SNLR was 40 per cent.

Take a look at our infographic below for a snapshot of GTA sales and new listings activity one and two weeks following the state of emergency declaration from the Province of Ontario:

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2