Flip/Assign Vs Rent

Is It Better to Flip/ Assign or Hold & Rent? Here’s Why Buy and Hold Is Best

Expertise: Landlording & Rental Properties, Personal Development, Real Estate News & Commentary, Business Management, Flipping Houses, Mortgages & Creative Financing, Real Estate Deal Analysis & Advice, Real Estate Wholesaling, Personal Finance, Real Estate Marketing, Ask Home Leader Realty inc, Real Estate Investing Basics

There are many ways to make money in real estate. You can wholesale, fix and flip/ assign, develop, broker properties, and more. But there’s a difference between making a living in real estate—aka simply having another job—and investing in real estate. You might be asking, “Is it better to flip/ assign or rent?”

Want more articles like this?

Create an account today to get Home Leader Realty’s best blog articles delivered to your inbox

In my opinion, there’s only one answer. If you want to make real, life-changing money, you need to invest in real estate. You need to buy property and hold onto it.

When you wholesale or flip / assign a property, you’re working for the asset instead of letting the asset work for you. It’s a job versus an investment. Yes, if flipping is your day job, then great. But buy and hold needs to be part of your strategy from the beginning.

Besides you may not fully take advantage of TAX implications on your investments. (Ask us for more information on this).

Ready to invest in rental property? Home Leader Realty’ guide to the buy and hold strategy will teach you how to analyze rental markets, budget for your investment, choose the best property, and finance your purchase. Ready to start investing in rental property? Here’s how.

The 5 Advantages of Buy & Hold Real Estate: IDEAL

Over the years, I’ve wholesaled and flipped properties, and I’ve worked with clients who have been very successful in doing this. I can honestly tell you that I regret selling almost everything I’ve ever sold. The only sales I don’t regret are the ones I exchanged into other properties. Here’s why.

I: Income

Most investments offer either a consistent return (i.e. annuities) or the potential for equity appreciation (i.e. stocks). Real estate offers both. Good buy and hold investments offer positive cash flow from rents that not only offset the expenses and debt service, but also provide a monthly income. The average annuity only pays out 3.27 percent per year.

A halfway decent buy and hold investor can beat that any day.

D: Depreciation

Flipping is a great business, but one of the biggest cons is that the tax man always gets theirs. Not so with buy and hold.

The CRA allows you to write off the value of any property over 27.5 years. Yes, this depreciation counts as negative income—but it’s only negative on paper, since the costs of keeping a property in good condition can be paid for out of the rental income.

Thus, the depreciation “losses” wipe out the positive cash flow from the property and remove any tax obligation. Unfortunately, due to the Tax Act, only active investors can take advantage of this.

E: Equity Build Up

With pre-construction investment you are building up the most part of your equity before your put the key to the door (TBD).

With a mortgage, unfortunately, comes the obligation to pay it back. Fortunately, the cash flow mentioned above allows an investor to pay back that mortgage without spending any of their own money. Instead, the tenant pays for it.

Furthermore, each month—assuming you don’t have an interest-only loan—part of the principle is paid off, too. For a 30-year Mortgage, about 15 to 25 percent of each loan payment goes directly toward the loan’s principle. That adds to the equity you have in the property.

Plus, accelerating equity pay down—the simple concept that, with each payment, you pay more to principal and less to interest—helps build up equity faster the longer you own a home.

A: Appreciation

Real estate, like any other asset, can go up or down in value.

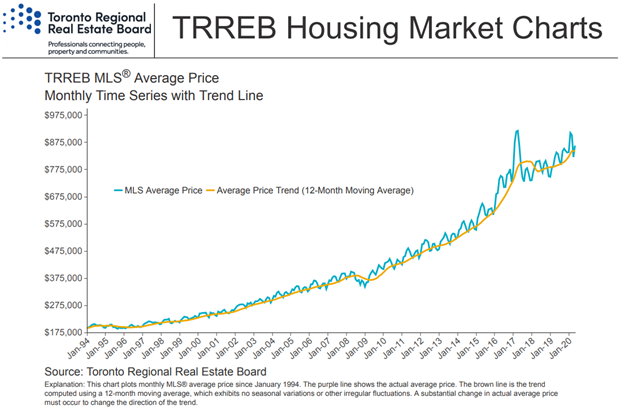

Many have been scared off by the crash in 2008. Worried history might repeat? A look at long-term real estate prices may encourage you. The trend is consistently up. In fact, over the past 26 years, real estate has gone up an average of 15.9 percent per year. Combined with accelerating equity pay down, this means that your equity grows exponentially the longer you hold a property.

Some have pointed out that the stock market generally has a better return than real estate. True—but deceptive. Real estate is generally leveraged at a rate of four or five to one. Stocks, on the other hand, are rarely leveraged, especially after the massive losses taken by those “buying on the margin” before the Great Depression.

L: Leverage

If you invest $20,000 into the stock market, and it goes up 10 percent, you’ve made $2,000. If you invest that same money into real estate, you can buy a $100,000 property with an $80,000 loan. Let’s say it only goes up five percent. Well, you’ve made $5,000. Or in other words, you’ve made a 25 percent return!

Technically, yes: the stock market has a higher return on average. But that’s immaterial. Your returns with real estate are based on a much higher amount than your principal investment.

One might think this makes real estate more risky than stocks, but that isn’t so either since, as Zack Finance points out. “Stock prices are typically more volatile than real estate prices,” he says. A buy and hold investor who invests right can make it through major downturns like the 2008 crisis—which saw stocks drop as much as real estate, by the way—with the positive cash flow from the property.

In the long run, real estate and stocks both go up. So if you can survive the downturns with positive cash flow, you’ll be just fine in the long term.

Is It Better to Flip or Rent Properties?

This really shouldn’t be phrased as a competition—after all, flipping is a great business, and flipping and holding aren’t mutually exclusive. Flipping can be a fantastic way to raise the money necessary to hold real estate.

That being said, there are several major benefits to holding:

- Tax advantages, such as writing off depreciation

- Passive income—whereas once a flip is done, the income potential of the property has ended

- Easily scalable, because if you flip 10 houses one year, the next year, you still start with zero. Hold 10 houses? The next year you start with 10.

- Equity, which allows you to refinance out and buy more properties, creating the opportunity of exponential growth

Common Buy and Hold Criticisms

Buy and hold isn’t perfect, and most successful investors use a blend of different strategies. But if you’re wary of dedicating your time and energy to buy and hold because of these common criticisms, think again: They’re easily refuted, and I’m happy to explain why.

“Stock Market Returns Are Better”

In addition to the reasons we’ve already explained, stock market and buy and hold returns simply can’t be compared on a one-to-one ratio. Stock market returns don’t include cash flow and principal paydown, either, in addition to their inability to be leveraged.

Home appreciation doesn’t beat inflation by much, but that doesn’t matter. Let’s use an example with a 30-year loan—and say it doesn’t cash flow one cent. You still pay down $8,000 in five years on $100,000 loan, which averages out at about 1.6 percent return per year. Since appreciation and inflation cancel out, you’ve still beaten inflation by 1.6 percent.

But of course, you only put down $20,000. So you need to multiply 1.6 percent by five—making it eight percent. Now you are beating the market by eight percent each year, and that’s without cash flow or appreciation.

“Leverage Is a Two-Edged Blade”

Yes, leverage can be a two-edged blade—small increases in a property’s value can produce great returns, but small decreases can create big losses, too. Leverage is a powerful friend and a powerful enemy simultaneously.

Let’s say you have an 80 percent loan-to-value mortgage and the market goes up give percent. You actually made 25 percent on your money. But if it goes down five percent, you’ve lost 25 percent.

This is the reason that the stock market is efficient—more or less—and the real estate market is inefficient. You won’t find a smoking bargain on the Dow Jones, but you’ll find plenty down the street.

Those great deals let you take advantage of the benefits of leverage while insulating yourself from its risks. That’s why buy and hold isn’t as risky as it might see. Let’s say you buy a property worth $100,000 for $80,000, putting $20,000 down. If it goes up five percent, you make an additional $5,000—or a 25 percent return. And if it goes down five percent… well, you can cry yourself to sleep knowing you’ve now only made $15,000 instead of $20,000.

Liquidity is convenient, but it is real estate’s illiquidity that give investors the advantage. Illiquidity allows real estate investors to find great deals and thereby dull the other side of leverage’s blade.

“Property Management Sucks”

The final criticism is the only one I agree with. What if you have the tenants from hell? Being a landlord is hard. Perhaps you can find a good property management company—but there are plenty of bad ones. Or perhaps you can do it yourself, but that’s a lot of work, and not all of it is pleasant.

Property management is one of two major cautions I would give someone regarding buy and hold. The other: buy and hold in a stable city—preferably a growing city, but at least a stable one.

If you are willing to do this, then there simply is no better investment around than buy and hold.

Purchasing your first rental property is just the beginning of your real estate journey, because being a good landlord is almost as important as making good deals. Home Leader Realty’s free guide How to Become a Landlord: Managing Rental Properties for Real Estate Investors will teach you everything—from setting rent to handling evictions.

Is Now the Right Time to Buy and Hold?

You may be wondering if now is the right time to buy.

I’ve bought and sold properties through good and bad times, and believe now is always the right time to buy, as long as the fundamentals of the purchase are sound. By that I mean:

- It cash flows.

- It is a good product in a decent location.

- You’re not over-leveraged.

Generally, if you’re worried about real estate cycles, don’t be. There are cycles, yes. But over the long-run, values always go up. With buy and hold, timing the market isn’t important—smart decisions are. Whatever you do for a living, if you want to make real, life-changing money in real estate, buy and hold as many properties as you can.

Maziar Moini

Home Leader Realty inc.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2