Altus Group data reveals 2017 was another record year for new condominium apartment sales in the GTA and seventh consecutive record year for investment property transaction value

TORONTO, Jan. 26, 2018 (GLOBE NEWSWIRE) — Altus Group Limited (“Altus Group”) (TSX:AIF), a leading provider of commercial real estate services, software and data solutions, today released results of the 2018 GTA Flash Report, which provides a comprehensive review of the real estate market in the Greater Toronto Area (“GTA”) based on 2017 Altus Group data. The report highlights another record breaking year for total investment property sales volumes, and looks at the performance of commercial leasing, land and residential sectors in the GTA.

Investment property sales, including land sales, as well as sales of office, retail, industrial, hotel and rental apartment properties, reached a total of $23.5 billion in 2017, a 38% increase from 2016 and a record for the seventh consecutive year. Residential land sales contributed a record $8.5 billion to the total, up $2.8 billion over 2016.

In the office leasing sector, the GTA-wide office vacancy rate fell in 2017 to 8.9% (including vacant but leased space), even with the completion of 13 new office buildings that have added two million square feet of inventory. Most of the new office supply under construction is in the downtown submarket, where the vacancy rate at the end of 2017 was below 6%.

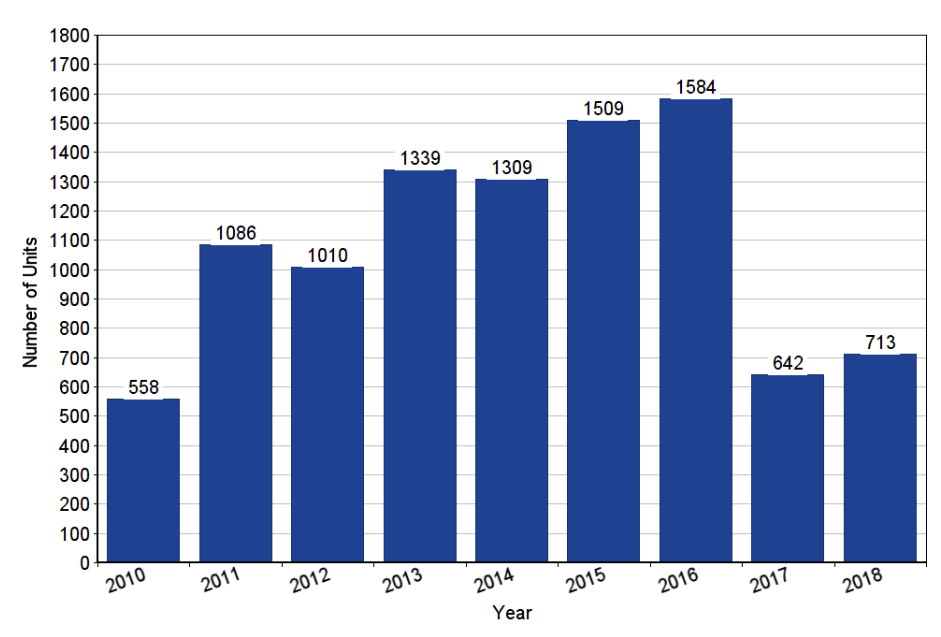

Turning to the new home sector, Altus Group’s data shows that total new home sales in the GTA reached just over 44,000 units in 2017, the fourth highest level on record. New condominium apartment sales, which includes apartments in low, medium and high-rise buildings, lofts, and stacked townhouses, smashed the previous annual record set in 2016 with just over 36,400 units in 2017. Conversely, new single-family home sales, including detached, link, semi-detached and traditional townhouse units, plummeted by 58%, with declines across all product types and in all five regions of the GTA. With just over 7,700 units, this was the lowest number yet recorded by Altus Group.

“Altus Group data show that homebuying intentions remain strong in the GTA, despite the many roadblocks that have been put in potential buyers’ way due to factors such as price escalation in recent years, rising interest rates, tighter lending criteria and additional stress testing,” said Matthew Boukall, Senior Director at Altus Group.

New condominium apartment inventory at the end of 2017 represented less than three months of supply, based on the monthly pace of sales over the previous 12 months. Average asking prices for available new condominium apartments increased rapidly during 2017, with the December average up 41% compared to the previous year, at just over $716,000.

The inventory levels of new single-family homes have risen from the low point in April 2017, although there were still relatively few available to purchase on average in 2017. Asking prices for new single-family homes averaged just over $1.2 million at the end of 2017, which is 23% ahead of a year earlier, although most of the increase occurred prior to Spring 2017.

The buoyancy in the GTA real estate sector in 2017 is poised to continue this year according to Altus Group experts. Below are key predictions for 2018:

- Office Shared Work Spaces:

- The trend of renting workstations within a larger office space will grow in the GTA as low vacancy rates lead to higher rents. Look for this segment to grow not just in the downtown market, but throughout the GTA, as employers look to accommodate staff pushed further out in search of more affordable housing options.

- Land Sales:

- Residential land sales are expected to be strong in 2018, although higher prices and various policy changes have introduced more uncertainty to the land market. High-demand areas are likely to remain expensive, which could push some developers to seek more affordable options outside traditional core areas.

- New Homes Market:

- New condominium apartment sales are expected to remain elevated in 2018. However, surpassing 2017 levels will be a challenge. While investor interest continues to be strong, some end user buyers who have been looking to the new condominium apartment sector for more affordable homes are now starting to be priced out of this segment as well.

- Some modest increase in new single-family sales is possible, however sales in this segment will continue to be challenged by lack of available product, in particular options that are affordable to a broader range of buyers.

- Industrial and Retail:

- Demand for industrial space will remain strong as online and traditional retailers seek warehouse space to support their e-commerce business strategies.

- Retailers will continue to shrink their brick and mortar footprint and traditional retail space will continue to evolve as retail centres focus on consumer experiences, especially food themes, to draw in traffic.

- Investment Property:

- Investor appetite will remain strong in 2018. With interest rates moving up, there is potential for some shift away from debt-financed buyers toward more cash-focused institutional buyers.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2