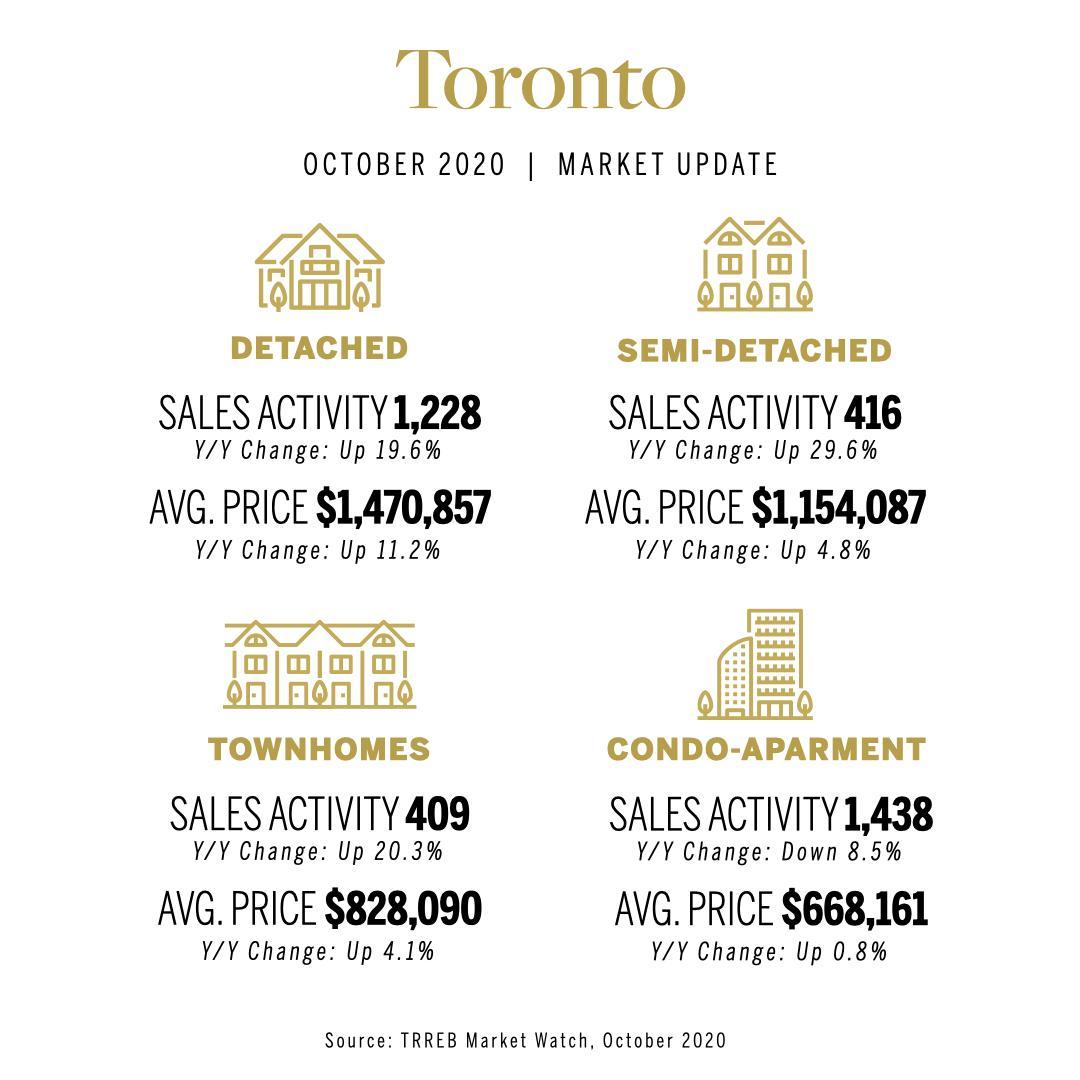

he temperatures may have cooled down, but the Greater Toronto Area (GTA) real estate market continues to heat up, with home sales up over 25% compared to October 2019, marking the fourth month in a row of year-over-year growth, according to the latest data from the Toronto Regional Real Estate Board (TRREB).

According to TRREB’s October housing market report, resale activity in the GTA is showing no signs of slowing down, after having another record-setting month, during which, a total of 10,563 sales were made — a 25.1% jump from the 8,445 sales recorded in the previous October.

The record-level sales were paired with record listings, with 17,802 recorded across the region compared to 13,053 in October of last year. However, despite the overall growth in listings, TRREB said the number of listings “diverged” in some markets, such as the detached home segment, where the pace of annual sales growth greatly outpaced listings. On the other hand, the condominium segment experienced over double the listings seen in October 2019, while sales only increased by 2.2% in the same period.

“Competition between buyers of single-family homes, and particularly detached houses, remained strong last month and continued to support double-digit annual rates of price growth in many GTA neighbourhoods,” said TRREB President Lisa Patel.

“In contrast, condo buyers have benefitted from much more choice compared to last year. Pre-COVID polling had already pointed to an increase in investor selling in 2020. The pandemic only added to this trend with a stall in economic growth and a halt to tourism impacting cashflows for many investors.”

Home prices have been steadily inflating over the past several months, and last month was no different. The average selling price for all combined home types rose 13.7% year-over-year, up to $968,318 from $851,877 in October 2019.

“Year-to-date home sales through October were above last year’s level. The economic recovery in some sectors coupled with low borrowing costs has kept home purchases top-of-mind for many GTA residents. With this being said, we have not accounted for all of the pent-up demand that resulted from the spring downturn. Expect record or near-record home sales for the remainder of 2020,” reads a statement from Jason Mercer, TRREB’s Chief Market Analyst.

Looking ahead, TRREB is remaining positive, with CEO John DiMichele stating that “beyond COVID-19, it is clear that the high demand for housing will continue.”

“The federal government has set immigration targets above 400,000 people for each of the next three years. The GTA will undoubtedly continue to benefit from this population growth. All of these people will need a place to live, whether in the ownership or rental markets.”

In October, the feds announced they are increasing the country’s immigration target between 2021 to 2023 to make up for this year’s pandemic-induced shortfall.

Canada’s Immigration Minister, Marco Mendicino, said the country will welcome more than 1.2 million new immigrants over the next three years, with up to 401,000 new permanent residents in 2021, 411,000 in 2022, and 421,000 in 2023 — an increase of 50,000 each year compared with the previous targets. The previous plan had set targets of 351,000 in 2021 and 361,000 in 2022.

Zain Jafrey, a real estate agent with Coldwell Banker, agreed with DiMichele and said the upcoming increase in immigration matched with low housing inventory and low-interest rates will continue to push prices post COVID. “An increase in population throughout the GTA will continue to increase demand for properties as people will require a place to live and will very well push prices in both the rental and ownership markets. The current pent-up demand will become greater due to the increased competition for limited properties.”

During the COVID-19 pandemic, Canada closed its borders to the majority of immigration hoping to ease the spread of the virus. “Once lifted, this new influx of immigrants and the pent-up immigration being held off by COVID-19 will pick up where strong demand — due to lowered interest rates — taper off,” said Broker Matthew Adam Cracower, who specializes in Yorkville real estate.

“The resiliency of the Toronto and GTA market proved itself during the pandemic and this shows how strong the bounce-back will be once COVID-19 is eliminated.”

Shaun Denis, CEO and broker for Umber Realty, believes that in addition to immigration, there are still a number of factors supporting the housing market in recent months — including low-interest rates, pent-up demand, government support. “As we project a strong positive net migration in the coming years, we expect overall demand will continue to rise into 2021. It is important to note that the lingering effects of COVID-19 will cause disproportionate demand between property classes in the city,” added Denis.

Dorian Rodrigues of PSR Brokerage also believes the current demand will continue into the new year, but partially because “there are many people who are still trying to plan their living situation based on their work scenario.”

“Many buyers have been trying to move from condo life to a house and or move out of the city for more outdoor space. The interest rates also have been low for a number of years now and obviously having them stay low will provide more opportunities to buyers moving up in the market, which we have been seeing a lot.”

While these brokers all echo similar sentiments, some economists have a different point of view.

Benjamin Tal, deputy chief economist at CIBC, recently said he believes “the housing market will slow down,” and subsequently, the economy, too, despite the current overall confidence in the Canadian housing market.

“Even the governor of the Bank of Canada is telling us, listen, don’t expect any growth basically over the next six months. The party’s over. You can’t have a o% increase in the economy with the housing market continuing to boom,” said Tal.

Tal also added that another factor influencing his forecast is that the damage to the labour market will be “much more significant in terms of the impact of the economy and the impact on the economy.” “Normally you would see more higher-wage jobs disappearing or at least you would have less job security there. And that’s very, very important,” explained Tal. “So, I believe that this optimism is not actually going to last for too long.”

Tal said that if you ask any real estate developer or investor in the condo space, they’ll tell you the market isn’t actually that “hot.” As such, Tal says all the focus is now on the low-rise segment of the market where there is no supply.

“The demand is there because of the nature of the crisis and this means that we soon will reach, I believe, a price resistance, even in this segment of the market and it will start softening.”

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2