Finding a stable, affordable and comfortable place to live is what Torontonians are after, Toronto’s Deputy Mayor Ana Bailão tells Toronto Storeys.

Bailão, who is also the city councillor of Ward 9, says “Housing affordability and affordable supply are the issues that concern Toronto residents the most.” And while Bailão says there isn’t a mandatory obligation for tech companies to create these options, she hopes that “tech companies will adopt a role in supporting the creation of affordable housing” working with the city and community.

Bailão points to investment, which tech companies can plug into the housing market to support the growth of the housing supply. Or tech companies could help build directly and explore new real estate strategies, creating places to house their workers after work too. After all, with investment also comes the ability to recruit high calibre talent to the city, and when they come they will require somewhere to live. But is it the responsibility of, say, Google or Microsoft, to handle employees’ housing situation in addition to delivering their paycheques?

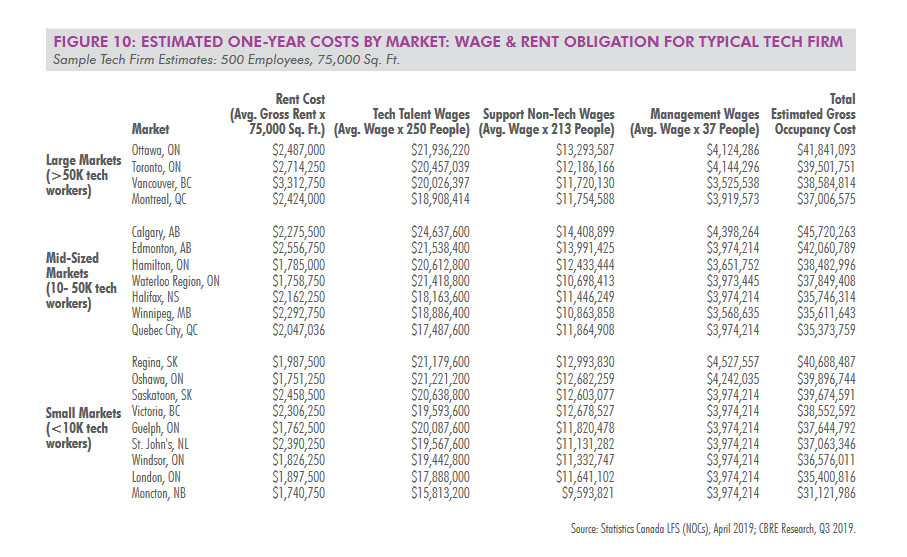

According to the 2019 CBRE “Scoring Canadian Tech Talent” report, Toronto was the top ranked city when measuring tech availability to quality of labour to cost competitiveness, receiving an 88.1 percent score. Ottawa (73.1), Vancouver (71.4), Waterloo (69.4) and Montreal (69.3) rounded out the top five, with 20 Canadian cities evaluated.

The 2019 report states that across three cities – Toronto, Vancouver and Montreal – there’s been a 2.8 million sq. ft of new build pre-leasing carried out by tech firms. Also, Toronto and Vancouver have the lowest downtown vacancy rates in all of North America, according to CBRE, and the tech industry has accounted for 17.1 percent of office leasing activity since the beginning of 2018.

Many tech startups turn into profitable tech enterprises, and this can happen fast, so finding a space that also moulds to changing needs can be difficult for those with less cash flow than Google and Shopify, both of which have announced their plans for new office setups in the city, slated to open in 2022.

Tech companies have moved, and are continuing to move, into Toronto. They are shaking up how they do it too, now occupying full floors with varying operations throughout. Take Google’s multi-year deal with IWG Spaces (WeWork’s rival) this past fall, which will see the tech mammoth house 24,000 sq. ft of the Royal Bank Plaza downtown – so two floors dedicated to Google, held in the corporate plaza with neighbours like the Fairmont Hotel, and located directly in the city’s financial district.

Now that they are here, and as Toronto’s talent and output continues to grow all while Toronto’s low housing vacancy rate continues and people struggle to find and keep a livable home – should we be looking to tech firms to solve the housing crisis we have on our hands here? Could they help?

We asked four valuable sources to give us their take on tech and housing in Toronto, and if in fact “tech can help save Toronto” from its housing problem.

Featured are Toronto’s Deputy Mayor, Ana Bailão; Jason Mercer, chief market analyst for the Toronto Real Estate Board (TREB); Matt Daigle, founder and CEO of Rise, a business focused on sustainable home improvement; and Claire Buré, manager at MaRS Solutions Lab.

Below we touch on topics around housing supply, innovation, and emerging building technologies in the housing market. We also ask if there is a responsibility for lucrative tech businesses to invest in housing infrastructure for the communities they serve.

Ana Bailão , Deputy Mayor and City Councillor, Ward 9, Davenport

“Tech companies have been an integral part of our city’s prosperity and continued economic growth,” says Deputy Mayor Ana Bailão . However, Bailão also realizes that “some of the impact of the tech sector on the housing market is, of course, difficult to qualify.”

Bailão notes Sidewalk Labs’ proposal as an example of a technology firm seeking to participate directly in the housing market. “We need to work with tech companies to leverage our processes to ensure that affordable housing is a part of their considerations and a product of their prosperity in our city,” explains Bailão. But these developments also need to be made for and with the community, created for everyone who chooses to live here. And done safely.

Bailão says the public policy debate over whether or not there is a civic duty, or responsibility, of businesses to ensure that the people who choose to work in Toronto can actually live here, existed long before tech was around.

“I do think there is a responsibility to occupy a role” in making ‘livable’ happen, she says, “They are their employees after all.”

Bailão says there is “unquestionably” a role for tech companies moving forward; they should be part of the solution to housing challenges faced in this city. “However, not just tech companies but all larger employers and others” should be chipping in here too.

“It is entirely consistent that large pension funds, public or private, should be investing in the affordable housing market as the beneficiaries of this kind of investment is their clients who are employees of companies within the city,” furthers Bailão.

Still, the Deputy Mayor reiterates that investment within the housing market is the most impactful way tech can play a role in helping solve concerns around housing in Toronto.

As for Sidewalk Labs? Bailão thinks if properly managed it could have a positive role in Toronto, but only if key issues like data management are handled responsibly.

“Our city is taking steps such as our recently approved Housing T.O. 2020-2030 Housing Action Plan, our Housing Now initiative, changes to planning policies, and other steps,” to address housing challenges and future demand in the city. “However, the most effective way to ensure that all of this is successful is by having all sectors and individuals working together,” she adds.

Jason Mercer, Chief Market Analyst, Toronto Real Estate Board

TREB’s Jason Mercer says supply is a big problem in the city, and we haven’t seen any movement – whether talking about ownership housing or rental housing, market-based housing or more affordable housing provided by a level of government agency. There are buyers looking to buy but are now “up against basically a flatline in supply,” he says.

“We live in a region that creates jobs across a number of different sectors, including the tech sector, which continues to be a growing sector in the GTA and the Golden Horseshoe,” says Mercer. “This attracts people from all over the world and they require a place to live – we certainly haven’t seen the level of supply to keep up with demand.”

Mercer also notes that we haven’t been building the “transitionary housing” that people require; moving from a condo apartment to a duplex, then maybe a town house, for example, creating life-cycle housing options.

“I’m not saying it’s a magic bullet and if you provide those types [of transition housing] then everyone is going to be able to find affordable housing but I think given more choice at different price points, it would certainly be a step in the right direction.”

Mercer adds that there’s certainly a place for industry stakeholders, traditional (like TREB) and non-traditional (like tech firms) to work together to solve housing issues, also noting the Sidewalk Labs proposal. But he doesn’t think they should be taxed in order to do so.

“It’s one thing to say, ‘hey, we are going to solve the housing supply problem by taxing this group’ – it’s really easy policy. But with a vibrant and growing population where tech grows too, people will need to live in the city they work in and tech companies can’t help if there is nothing there in supply in the first place.

“If you look at the new listings reported by the TREB over the last decade, they are essentially flat – 150,000 to 160,000 listings – yet sales have been trending upwards. It doesn’t make any sense,” he adds.

Mercer continues to stress the need for supply, and while tech companies are not responsible for creating these, they certainly can start becoming more involved in the oversight process given they are becoming an increasing presence in Toronto’s economic and real estate infrastructure.

“It’s not just housing for the sake of housing, it’s to remain competitive on the global stage,” says Mercer.

Matt Daigle, Founder and CEO of Rise

“I don’t know that tech companies are the ones that are going to solve the biggest problems because they already have their own businesses going,” says Matt Daigle, whose online home improvement portal is for anyone looking to build with sustainability in mind. He’s about “baking sustainability into the DNA of home improvement”.

He notes companies are trying to industrialize the way they build a home, using “CNC [computer numerical control] machinery to build out your wall panels,” or “completely rethinking how we actually build a house” with technology elements in mind.

Daigle says, however, “we’re still building to a similar code that we did 100 years ago,” which he thinks is a big barrier. “I think there are already building standards that you can work with but building with sustainability in mind is the way forward.”

Daigle says governments should incentivize solutions that are better for energy efficiency, and that building technologies (like air recirculation and ventilation systems) are increasingly becoming used and asked about. We should be looking at “building better homes using technology,” which might even cost less than we thought, he says.

Daigle is from Fredericton, New Brunswick, and his company serves the interests of Canadians and Americans, helping people cost appropriate and understand the ‘home’ – from decks to lighting to solar air and water space heaters.

“Technology, hardware or software, is at the core of where the housing industry is going,” says Daigle, who notes 3D printed homes is an emerging area, but that, “tech companies don’t owe anyone more than what other companies should be doing when it comes to housing.”

Daigle says technology can certainly help improve housing conditions and efficiency, and there are innovative models already underway. He highlights German building standard Passive House, whose code is focused on building a well insulated shell of a home so your heating and cooling load remains minimal, with less money spent on energy bills, and “you can leave your house for two months without turning the heat on and your house and pipes don’t freeze,” he says.

Rethinking partnerships around affordable housing is important too. Facebook and Google have already done it in the United States, and granted government and community approval, Toronto could adopt a similar model. Seeing what happens with Sidewalk Labs and its development will also set the groundwork for future visions on housing.

If the codes and ways we build are modified, there’s more room for tech companies and other businesses to help out.

Daigle says more availability and attention should be granted to the prefabricated housing market as well.

Claire Buré, Senior Manager at MaRS Solutions Lab, leading work in affordable housing

+

Co-founder of Commons11, a Toronto collective fostering social change through technology, co-design and co-creation.

Transit-oriented affordable housing is Buré’s focus, which she explains is about “innovating within the procurement process for transit infrastructure investment.” So, developing affordable housing as part of the new transit development that is currently being built in Toronto.

“It’s a complex problem with many barriers to innovation, but also many opportunities to do better,” she adds.

Buré says we often treat technology as though it can solve all our problems, however, “we need to remember that we are the ones who create the technology.”

While tech companies could help with the housing crisis, is it safe for them to? And who are they working with (and for) to make this happen? Should they be required to allocate 20 percent to specific housing projects, or community builds to serve more Torontonians looking for somewhere affordable to live?

Buré says either way you look at it tech companies have an enormous power, especially the big five: FAANG (Facebook, Amazon, Apple, Netflix, Google).

“Taxing tech companies and ensuring payment, like the European Commission has done, is one way to generate and redistribute revenue,” says Buré, but we need to be asking: “Who is extracting and who is contributing value to society? And how can we enable greater value for communities, including for housing affordability?”

Buré adds that we need tech companies to ensure diversity and adhere to community values, rather than focus on financial gain.

So, whether or not the tech industry can save Toronto’s housing crisis might also boil down to: do we want it to?

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2