Many people have pointed out that the COVID-19 pandemic has magnified several negative trends that were already underway, from income inequality to disfunction in care for seniors.

And for renters and landlords, this may turn out to be the case as well.

Over the past five years, the number of people who turned to renting over ownership started reversing to more historical ratios, industry observers say, while more apartments were coming on the market, slightly easing the tight vacancy rates.

Then the pandemic hit. As the lockdown put people out of work, slowed migration in the GTA to a trickle, and essentially shut down demand for Airbnb units, the effect on rental units has been rapid. Not only has there been a slowdown in people looking for rental apartments, creating less demand, but with more condos and purpose-built apartments available, there is also more supply.

Rental prices were already starting to flatten since August, those tracking the data say, and they have dropped in April, compared with a year ago.

All of this spells trouble for condo owners and relief for renters.

The question is, is this a short-term or a long-term trend?

We’ll get to the long-term question soon, but the short-term trend is clear.

“As rental demand declines as job losses mount, incomes are reduced, and immigration shrinks, the slowing in the GTA rental market that appeared in the last half of March will progress for at least the next few quarters given the current economic outlook,” said Shaun Hildebrand, president of Urbanation, in the real estate consulting firm’s most recent report from April 17.

Leases down, listings up

Lease activity is down more than 70% compared with April last year, says Pauline Lierman, director of market research for Urbanation.

The financial impact of the pandemic, which hits renters harder, according to John Pasalis, president of Realosophy Realty, combined with the increase of supply, will create more vacancies. Although there are emergency measures now to help people stay afloat, such as the CERB and relief on rents, it’s not clear how long that will last.

“Toronto’s labour market will be hit hard by the pandemic this year,” according to a recent Conference Board of Canada report. “Over 42,600 jobs will vanish, lifting the unemployment rate to 8.0 per cent. In the second quarter alone, employment is anticipated to fall by 5.0 per cent, while the unemployment rate is expected to hit 13.9 per cent.”

This will push some to move in with family or roommates, adding to the supply of apartments. And, as Urbanation points out, at the same time that there are fewer leases there are also more listings, adding to the overall supply.

In fact, there is a particular type of listing that has skyrocketed compared with last year…

The Airbnb factor

Furnished apartment listings in April were up about 90% compared with April 2019. This is a direct result of the ‘Airbnb impact’. (Generally unfurnished apartments are intended for longer-term rents.) The average rental price of furnished apartments is down about 10% from April last year, according to Urbanation’s data.

“Investors are not like owners” who live in units, says Pasalis. “They don’t want (their units) sitting empty.”

And there are more units owned by investors slated to come online. There are already about 400-500 units sold primarily to investors in buildings still to be completed just in downtown Toronto, according to Urbanation’s Lierman.

While the city is looking to curtail short-term rentals through regulation, many experts don’t see these as having a major effect on the rental market, or on decisions by people whether to buy in a condo for investment purposes. It is mainly the freeze on travel and its effect on short-term rentals that are seen as pushing investors to put these units up for long-term rental instead.

This will likely affect studios and one-bedroom condos most, says Scott Ingram, a sales representative with Century 21 Regal Realty Inc. Though Lierman notes that the health aspect of the circulating virus may push individual buildings to create stricter rules and enforce them once travel opens again.

Investor-owners are also facing competition from a growing number of purpose-built units coming online in 2020.

More units still to come

There have been a record number of building completions in Toronto, says Ingram. “And there are still buildings expected to be completed this year,” he adds. The first quarter of 2020 – just to the end of March – saw 7,150 unites completed, with an expected 10,000 units coming online in the second quarter, although some of those may now be delayed.

According to Lierman, before COVID hit, an anticipated 25,000 to 29,000 units were expected to be available by the end of 2020. That amount of units represents up to 100% increase over 2019 when 14,468 units were completed.

Even with delays, Lierman still expects about 20,000 new units to hit the market this year.

In line with this thinking, Brian Brown, Principal at Lifetime Developments, confirms that “We have still seen strong interest in our projects especially the project that we launched just before the pandemic, Liberty Market Tower. Sales have continued through the lock-down.” He adds, “We have experienced a slowdown but not a shutdown.”

Though, as units come online, one of the major sources of demand for them is currently AWOL due to COVID. That source? Immigration.

Immigration frozen

Migration is one of the major sources for renters, whether immigrants, foreign students, temporary workers or people moving from another province. All of this is frozen, though for how long is difficult to determine, experts say.

Once borders re-open, Canada will continue to rely on immigration as an economic driver, as the population ages, Immigration Minister Marco Mendocino told the Canadian Bar Association’s Immigration Law Section on May 5.

Before instituting border restrictions due to the spread of COVID-19, Canada pegged its immigration target at about 1 million between 2020-2022. The GTA has received about one-third of the country’s migrants, or about 100,000 people, in the past couple of years, Lierman says.

But a May 12 report from The Conference Board of Canada estimates the number of people coming into the region will drop to 65,710 due to the pandemic in 2020. While the government aims to announce a post-COVID immigration plan before its annual announcement this fall, a 35% decrease in the number of migrants in the GTA will certainly impact the rental sector.

Swing back to renting

When you look at longer-term trends, the ratio of renters to owners is shifting back to what it was earlier, says Peter Norman, vice-president and chief economist, Altus Group, which provides data to the real estate industry.

During the early 2000s, there was a long downward trend in interest rates and there was still relatively affordable housing. Younger people, in the 20-29 age group, were skipping rental and buying condos. The ownership rate was about 33%, with about 66% renting. By 2011, about 40% owned and 60% rented, Norman says.

But with ballooning housing prices, that trend started turning around. In the past five years, it has started reverting to earlier ratios. Now the demand for rental housing is about one third. Over the past five to six years there has also been a shift away from owning condos as an investment, Norman adds, with condo sales moving back to owner-occupier.

Now, the recession from the economic freeze due to the pandemic is expected to slow the rental pool of young people leaving their parents’ homes.

Price break for renters

Average rents in Toronto were flat compared with the same time last year at about $2,375 for the first quarter, or until the end of March, of 2020, according to Urbanation.

However, April was down about 3.5%, compared with April of 2019, according to Pasalis. This comes on top of rents that have been trending downward since August, he adds.

Though Urbanation’s Lierman would not be surprised to see average rents down about 5% in 2020.

There have been two to three years of rapid rental increases, says Altus’s Norman. “This recession will halt the upward movement on rents.”

Longer-term lens

The long-term trends beyond the direct impact of COVID-19 are still positive for Canada, Lierman says. Big investors, like REITs, look at revenue in a longer time frame and, though they may slow development, the longer-term outlook for rental still makes sense for these investors.

“This is not a recession in the traditional sense of a recession,” says Brown. “This is a health crisis that carries with it some of the similar financial challenges but the rebound effect should be much quicker and stronger.” He adds: “We are still dealing with an undersupply of homes in a market with high demand.” He notes that, “Real estate investments are still seen as a stable investment with strong future growth.”

The bottom line

Longer-term, the Conference Board expects Toronto’s labour market to recover to some extent next year, with employment growth of 2.7%.

And once the immediate crisis is over, Canada will likely continue to need large numbers of immigrants to replace an ageing demographic and help the economy recover and grow. As the country’s largest economic engine, the GTA will likely continue to attract a sizeable number of immigrants, who make up a significant percentage of those who rent. This, combined with more people looking at renting over ownership because of job losses and a recessionary economy, will likely mean the demand for long-term rentals will stay strong, and large investors are not indicating a retreat from purpose-built apartment buildings at the moment, industry experts say. And those condo investor-owners who are prepared to rent their units longer-term will likely benefit from a market that is still unlikely to meet future demand.

All these figures come together to paint a future that looks a little brighter for renters and a little worse for condo investor-owners who had counted on income from short-term rentals like Airbnb.

There is something unsettling about a quiet city.

The empty streets, squares, and taped-off playgrounds that were full and vibrant only a few months ago now sit silent, stirring a seemingly endless series of questions about our recovery.

At The Bentway, Toronto’s urban park built under an active downtown expressway, ambitious plans for Spring programming have been temporarily shelved. Elbow-to-elbow ice skaters have been replaced by lone joggers and occasional dog walkers. The park, surrounded by high density towers, pulses with the promise of freedom and escape, but remains responsibly tranquil. Even the gentle hum of the highway above has slowed and softened.

Like The High Line in New York (and as the sole Canadian member of The High Line Network), The Bentway was founded on a public-private partnership that sees the site operated, developed, and animated by an independent not-for-profit. For organizations like ours, public space is a passion and a set of principles, of course, but also a profession and an everyday reality.

This disease is challenging the very value system and best practices that have guided our work for so long. Though time moves slowly these days, the vocabulary we have developed to respond to the COVID-19 crisis is changing rapidly. We are no longer discussing days, but months and years. We are no longer planning for a “return to normal” but are rather scrambling to predict the “next normal”.

What does shared space look like in the post COVID-19 city? What role will public space play in the next normal? These are the fundamental questions at play.

Resisting our defensive instincts

Here in Toronto, parks and public spaces have remained accessible, though the City has closed park amenities like playgrounds, picnic tables, and skateboard parks. Police and bylaw officers are now on patrol to enforce physical distancing, with reports of hefty fines issued for lingering on benches “beyond necessary resting purposes.”

Reasonable arguments can be made to justify severe restrictions in these troubled days but as the city prepares to reopen these spaces one must ask, what comes next? Amid the myriad of speculations are loud and familiar calls for more restrictive public infrastructure. A culture of fear produces well-intentioned features like contactless pathways, barriers to entry, reactive architecture and other moves away from open congestible space.

This is neither the first nor the last time that designers will be asked to generate defensive strategies for public space. The 1970s saw a wave of built space practices aimed at deterring vagrancy, reducing crime, and minimizing other high risk activity. Spiked gates, short benches, and studded surfaces became common tools employed in the service of so-called public safety. While these strategies were not visually disruptive, they shrewdly defined a ‘right way’ and a ‘wrong way’ to engage and exist within public space, and, moreover, produced a ‘right user’ and a ‘wrong user.’ Ultimately, defensive design practices targeted (and still target) the city’s most vulnerable individuals, who rely on and benefit from public space heavily. These include seniors, lower-income individuals, racialized people, people with disabilities, and un-housed people.

One group that was singled-out directly by these tactics was the skateboarding community, whose members had found new ways to incorporate urban furniture and concrete landscapes into their explorations of the city. Metal knobs and abrasive edges, were aimed at curbing this unanticipated activity. They served as subtle but clear signs of what had been deemed tolerable behaviour in communal areas.

In 2018, The Bentway aimed to reframe this seemingly ‘unwanted’ practice and its negative connotations by working directly with the skateboarding community on the development of public space strategies and a pop-up park. That summer, we were introduced to a responsible and respectful family of boarders who cared for The Bentway space because they knew they were welcome. The temporary ramps have since moved elsewhere, but the skaters remain and continue to safeguard a space in which they are invested.

In recent years, designers and city-builders have largely come to reject defensive strategies and the exclusionary policies from which they stemmed. Great public spaces are now built with flexibility and approachability in mind, offering ample amenities and public resources.

Yet, even in the best of times, the creation and operation of public parks, squares and community hubs remains both an honourable and difficult pursuit. The Bentway team encounters and struggles with the challenges of running an open space daily and in real time, but we have made the choice to learn from the communities that use our space rather than make decisions for them.

Spaces without walls and doors, that are open to all, are successful because of their mixed use and mixed audiences – their lack of predictability and control. They are places that belong to everyone, irrespective of socio-economic and cultural divides. They rely on a strong social contract – the same social contract that this crisis has brought to the forefront.

Public spaces and community hubs depend on trust that the members of the communities they serve will care for and respect the property, the programs and, most importantly, their fellow users.

Finding answers together

COVID-19 has demonstrated, at a global scale, that we are willing to make enormous sacrifices for our neighbours. It has demonstrated the importance of creating inclusive cities that are shaped by love rather than fear.

However, the true test of our resolve is yet to come. As we plan for the next normal, we must ensure that the design decisions that shape the next generation of public spaces are not simply reactive but also responsive in the most equitable way. This goal will require more expansive and integrated design teams, including public health officers, experts in social services, and community leaders among architects and engineers. It will require flexible strategies that are anchored by preparedness plans. It will also require a careful consideration of the past mistakes we made in the interest of public safety.

Even as the city reopens we must continue physical distancing, to protect our neighbours and do our part to end this crisis. Yet, if one thing is clear in this time of uncertainty, it’s that we won’t find the answers we seek behind closed doors. When our cities re-open, we will need public space more than ever. We will need places where city-dwellers can seek reprieve, find hope in one another, heal together and redefine the next normal collectively.

Before this crisis, we had already seen a significant shift in cultural production and consumption patterns. Artists, designers, educators and the public alike were increasingly interested in direct engagement with the city and were not afraid to confront urban challenges head on. Our public spaces had emerged as more than simply backyard parks but vital cultural, educational and recreational hubs where we could come together to learn and share.

Over the last two years, The Bentway has sought to find ways to celebrate city life, to create unforgettable civic experiences and to convene community discussions about the future of our city, and cities everywhere. We have worked with creative partners to tackle issues such as climate change, mental health, lost histories and industrial reuse. We’ve collaborated with and learned surprising lessons from skateboarders, artists, break dancers, environmentalists, historians, and poets. We have seen the power of public space first-hand and its ability to create new community connections.

COVID-19 has challenged this model of programming and civic life. It will take some time for us to find our bearings once the city reopens.

As we work together to redefine our expectations and experience of public space, set new comfort levels and discover new ways of coming together, we must also re-evaluate what success looks like. For too long, we have relied almost exclusively on measurables: attendance counts, demographics, eyeballs, tags, likes, etc. However, hard data has only ever been a small part of the real story. The next normal will see an even greater reliance on qualitative metrics — the intangible community and creative benefits that aren’t reliant on huge crowds, but instead are characterized by more intimate, meaningful interactions with our neighbours that help us to see the city and each other anew. Public space operators must align our future goals with those of a healthy city, considering all the factors that contribute to wellness.

There is no doubt that change is coming. The post COVID-19 city looks different from what we knew before; and public space is no exception. However, if we continue to uphold our social contract to each other and prioritize equitable design strategies, we will adapt and emerge even stronger than before. Public space has always been important because it belongs to all. This is a principle worth fighting to preserve.

Despite the uncertainty the COVID pandemic has caused for Toronto’s real estate market, residents are still interested in buying a new home in the coming months, according to a new survey from the Toronto Regional Real Estate Board (TRREB).

To get a better understanding of how the COVID-19 pandemic has impacted consumers, TRREB contracted Ipsos Public Affairs to conduct an online survey on home buying and selling intentions along with consumer opinions on preferred government policy directions related to the housing market.

Even with home sales and new listings down, 27% of survey respondents in the GTA said they are very likely or somewhat likely to purchase a home in the next 12 months. However, while buying intentions were down compared to spring 2019 (31%), they remained relatively in line with the five-year trend, especially after taking into account survey credibility intervals.

Here in Toronto, home buying intentions were above those in the GTA, with 34% of respondents saying they are very likely or somewhat likely to buy a new home within the next year. What’s interesting to note is home buying intentions were stronger for younger people aged 18 to 34 (45%) and for those with children (37%).

As for those who said they didn’t want to buy a home over the next 12 months, general affordability issues were a top concern, while 62% of respondents said they liked their current home and 16% said they didn’t want to move due to COVID-19-related issues.

“While COVID-19 has temporarily impacted home sales and listings in the GTA, the Ipsos survey results that show home buying intentions have remained quite stable certainly suggest that many people will be looking to satisfy pent-up demand for ownership housing once recovery starts to take hold,” said TRREB president, Michael Collins.

“As people gradually return to work, consumer confidence will improve, and a growing number of people will look to take advantage of very low borrowing costs to purchase a home. Home purchases will continue to be aided by the use of technology available to REALTORS®, including live-stream open houses,” said Mr. Collins.

When it comes to selling, 17% of existing homeowners said they were likely to list their home in the next 12 months, compared to 32% of homeowners in spring 2019.

According to the survey, a very large proportion (80%) of respondents indicated that they were unlikely to list their home for sale simply liked the home in which they are currently living in, while 22% said they weren’t going to list due to COVID-19-related issues.

“The supply of listings was an issue before the onset of COVID-19, with market conditions tightening and price growth accelerating throughout the first quarter of 2020,” said Jason Mercer, TRREB’s Chief Market Analyst.

“The Ipsos survey results suggest that the supply of listings will continue to be an issue as the economy and housing market recovers. Policymakers have acknowledged that there is a lack of a diverse housing supply in the GTA. While the supply issue has understandably taken a back seat to COVID-related issues in the short term, it should once again be top-of-mind once recovery takes hold,” said Mercer.

With consumers still concerned about affordability, the survey results also showed that public support for government assistance for homebuyers hasn’t changed since the pre-COVID-19 period.

According to TRREB, 82% of respondents support increased and more flexible access to Registered Retirement Savings Plans through the Home Buyers’ Plan; 75% support relief from municipal and/or provincial land transfer taxes; 73% support relief from municipal property taxes; 71% support relaxation of federal mortgage insurance rules to allow homebuyers the option of qualifying for a mortgage with smaller down payments; and 65% support relaxation of the federal mortgage “stress test.”

“Homeownership affordability is and will continue to be, a top concern as the economy recovers from the impact of the COVID-19 pandemic,” said TRREB CEO John DiMichele.

“With this in mind, it is not surprising that there is public support for government assistance in this regard. There is a definite role for governments to play in addressing affordability concerns, but policymakers at all levels should proceed with caution and assess the impact of pent-up demand and the potential lack of listing inventory during the initial recovery period,” said DiMichele.

Home sales collapsed as anticipated in April as unprecedented job losses, economic volatility and strict physical distancing measures sapped the momentum behind what should have been Toronto’s busiest home buying stretch of the year.

But as sales dropped 67 percent in April over the same time last year, home prices in the Toronto region still managed a 0.1 percent increase over April 2019.

While that modest increase is a significant deceleration in price growth achieved in previous months, market observers and industry members are hoping that a fall in home listings that roughly aligns with the decline in sales will keep prices from falling steeply during this turbulent period.

The April sales and pricing figures, released today by the Toronto Region Real Estate Board (TRREB), represent the first full month of data to showcase the disruptive impact of the COVID-19 pandemic on the region’s real estate market.

The precipitous drop in home buying activity was already evident in the second half of March as businesses shut down and social distancing measures were widely introduced. The decline in activity became more pronounced when TRREB published data for the first half of April that showed sales falling 69 percent over the same period a year ago. Unsurprisingly, this trend continued for the remainder of the month.

That said, there are still transactions happening across the Toronto region, as illustrated by the 2,975 properties that changed hands in April. In a media release published along with the data, TRREB noted that weekday sales were in a steady range throughout the month, averaging 130 a day.

Following sales on their march downward in April were new listings, which fell 64.1 percent over the previous year to 6,174. This was heralded as a positive development by TRREB, with the board’s Chief Market Analyst Jason Mercer noting that the number of available listings lined up with market demand to keep prices steady.

“When thinking about home prices, it is important to remember that the pace of price growth is dictated by the relationship between sales and listings,” said Mercer.

“So, while the onset of COVID-19 has understandably shifted market conditions and resulted in average selling prices coming off their March peak, there has continued to be enough active buyers relative to available listings to keep prices in line with last year’s levels,” he continued.

Diving deeper into the pricing data, it was sale prices achieved in the 905 area of the region that kept price growth from turning negative last month. The average sale price in the City of Toronto (known as the 416) was $881,424, down from $904,199 in April 2019. In the 905, the average sale price rose to $789,317, up from $773,736 in the previous year.

When it comes to property types, it was prices in the semi-detached and townhome segments that drove growth in April. Average sale prices in these segments rose 7 percent and 3.8 percent, respectively. The average sale price for detached homes in the region dropped 3.5 percent while condo apartments saw a 1.7 percent price drop.

With anxiety mounting throughout March as the economic impacts of the COVID-19 pandemic intensified, Canada’s central bank took swift action to slash interest rates at several points during the month.

The cut announced by the Bank of Canada on March 27th meant that the overnight rate — which influences mortgage rates — had reached a level not seen since the 2008-2009 global recession. The rate, at 0.25 percent, sits at the “effective lower bound” established by the bank, which means that it does not intend to lower it further to zero or into negative territory.

In a comprehensive housing report published earlier this month, BMO Senior Economist Robert Kavcic wrote that the central bank is unlikely to hike the rate until 2022.

The report, titled “Canadian Real Estate: Closed Until Further Notice,” Kavcic noted that the rapid cuts to the overnight rate have led five-year fixed-rate mortgages to decline to levels that match historic lows. Rates are available in the 2.4 percent to 2.6 percent range, said Kavcic, 50 points lower than rates seen last year, which were already very low by historical standards.

The BMO economist believes that the low rate environment will be the most significant, immediate support to the country’s housing market as the economy gradually reopens and business resumes over the next few months.

“[Low rates] will support demand as the economy re-opens, and we don’t believe Bank of Canada rate hikes are on the horizon until 2022,” wrote Kavcic.

The Bank of Canada’s next scheduled interest rate announcement is due on June 3rd, which is also the date that Tiff Macklem is set to assume the role of governor, taking over the position current governor Stephen Poloz has held since 2013.

It is unlikely that the bank will move the rate any lower even under new leadership, though Macklem, who was an associate deputy minister in the Department of Finance during the 2008-2009 financial crisis, has said it’s important to deliver an unprecedented response to this unprecedented situation.

One thing that appears to be certain is that mortgage rates will remain historically low for many months, or even years, to come.

Canada’s home prices are still likely to see a 5%-10% annual gain by year-end, according to Altus Group chief economist Peter Norman.

In an interview with The Financial Post, Norman said that despite the COVID-19 travel restrictions that have ground the entry of wealthy foreign homebuyers to a halt, housing will return to an upward trajectory in late 2020.

Norman acknowledged the fluidity of the situation, saying that the coronavirus might still mean worse times ahead for the market.

“Context is important for everything, and there is a lot in motion right now. It’s a difficult time to be forecasting,” Norman said. “Certainly, we see migration [being] really weak this year, and that has been a macro driver for housing in general.”

The pressures upon Canadian demographics and the economy are expected to persist throughout the second quarter and even well into the third quarter, with data in the April-June period likely to be “pretty dismal.”

However, Norman said that the housing sector’s fundamentals will pave the way for its speedy recovery once the crisis has passed.

“Don’t underestimate how fast things may come back,” Norman said. “We are not expecting prices to go down a lot. … It’s not a negative spiral; it’s not a housing crash.”

And even though prices will be “all over the map” for the next few quarters, “by the time we get to the end of the year and momentum is coming back, with pent-up demand from the downtime and supply coming back on stream in the resale market, I expect we’ll see a lot of activity,” Norman said.

As the coronavirus pandemic continues to have an impact on every industry, Toronto’s real estate market took another hit in April, with the average rent for both 1 and 2-bedroom apartments down on a year-over-year basis, according to new data from the Toronto Regional Real Estate Board (TRREB).

This coincides with rental transactions for both apartment types also dropping more than 50%.

According to TRREB, the average rent for a 1-bedroom reached $2,107, down 2.7% compared to April 2019. The average two-bedroom rent was ‘just’ $2,705, down 4.1% during the same time period year-over-year.

For context, in February, the month just before the pandemic hit, rents for one- and two-bedroom condos sat around an average of $2,300 and $2,900, respectively.

Rental transactions reported through its MLS System were also down on a year-over-year basis in April for both apartment types, with 1-bedroom condominium apartment rental transactions down by 57.9% to 754, while 2-bedroom rental transactions were down by 54.4% to 489.

With the strict social distancing measures currently in place and more residents without work as a result of the pandemic, a decline in rental market activity is to be expected. But how might the rental market look as the economy begins to reopen in the months to come?

Some experts have said the chance of a coronavirus-related housing market crash remains low, while Shaun Hildebrand, head of development-tracking market research firm Urbanation, says condo rents in Toronto could be even lower post-COVID-19.

“As rental demand declines as job losses mount, incomes are reduced, and immigration shrinks, the slowing in the GTA rental market that appeared in the last half of March will progress for at least the next few quarters given the current economic outlook,” said Hildebrand.

“The impact on rents will be something to watch, which will also be influenced by the timing of the record number of units that were expected to complete this year.”

As the province heads into its 50th day spent under a state of emergency as a result of the COVID-19 pandemic, further business shutdown restrictions have been loosened in Ontario.

Today, the provincial government announced that it would be expanding the parameters of essential construction to other activities and easing limitations on retail stores. This latest relaxation of restrictions will permit below-grade multi-unit residential construction projects to begin, along with allowing for the continuation of existing above-grade projects.

“For these buildings, below-grade work will be permitted and existing above-grade projects can continue so we can keep adding more housing and creating more jobs on the path to economic recovery,” said Premier Doug Ford in a daily press conference.

The expansion of essential construction operations means work on apartment and condominium projects can start or resume, slowly easing construction activities back to normal levels.

“With almost two thirds of the new housing units delivered each year in the GTA being in high-rise buildings, the resumption of below-grade construction is absolutely vital to meeting the region’s housing needs,” said Dave Wilkes, president and CEO of the Building Industry and Land Development Association (BILD) in a joint press release with the Ontario Home Builders’ Association (OHBA). “No work on a high-rise building can start without below-grade construction being completed.”

BILD explains that below-grade construction, which includes excavation, concrete forming, reinforcing and pouring, is used to install the foundation and systems that support high-rise structures. All expanded essential construction activities must comply with social distancing and virus prevention practices determined by the Ministry of Labour, according to the press release.

“We applaud the Government of Ontario for taking steady and consistent steps to safely re-activate residential construction work,” said Joe Vaccaro, CEO of OHBA in the joint press release. “With enhanced health and safety policies, buildings across Ontario can resume construction and move closer to completion. This decision moves thousands of families closer to getting the keys for their new homes.”

As of Monday, under the condition that they follow strict public health and safety protocol, the province has gradually started to reopen select businesses, including marinas, golf courses and landscaping companies. Today’s eased restrictions will also allow nurseries, garden centres and hardware stores to open for in-person visits over the course of the week. Retail stores with street entrances will also be permitted to provide curbside pick up and delivery services beginning Monday, May 11th.

On April 27th, a three-stage framework was released by the Ontario government outlining the gradual reopening of the province.

“We applaud the Government of Ontario for taking steady and consistent steps to safely re-activate residential construction work,” said Joe Vaccaro, CEO of OHBA in the joint press release. “With enhanced health and safety policies, buildings across Ontario can resume construction and move closer to completion. This decision moves thousands of families closer to getting the keys for their new homes.”

As of Monday, under the condition that they follow strict public health and safety protocol, the province has gradually started to reopen select businesses, including marinas, golf courses and landscaping companies. Today’s eased restrictions will also allow nurseries, garden centres and hardware stores to open for in-person visits over the course of the week. Retail stores with street entrances will also be permitted to provide curbside pick up and delivery services beginning Monday, May 11th.

On April 27th, a three-stage framework was released by the Ontario government outlining the gradual reopening of the province.

Those are among the insights offered by CIBC World Markets managing director and deputy chief economist Benjamin Tal during a May 5 Real Estate Forums webinar.

“It’s not a recession, it’s not a depression, it’s something in-between,” Tal said of the unprecedented position Canadians, and people around the world, find themselves in. “It’s basically a frozen economy.”

Tal expects a “recessionary recovery” to be long and in a “zig-zag” pattern, with volatility to be found in valuations, expectations, gross domestic product (GDP) growth and consumer confidence. The end point will be finding a vaccine or effective treatment for COVID-19.

Tal anticipates governments continuing to play a large role in the economy, as relief payments to get people through the crisis evolve into a more permanent universal basic income system.

Deglobalization will continue and two distinct trade blocs, respectively led by the United States and China, will be established. While Canada was trying to diversify its economy by lessening its reliance on the U.S. before this crisis, Tal now expects that to revert.

As well, Tal believes many companies will start thinking less in terms of profits and more in terms of resiliency.

More medical-related products and other essential goods will be produced domestically and there will be a move from “just-in-time” to “just-in-case” inventory systems.

Tal’s Canadian real estate market overview

“What we’re seeing now is not a market that’s functioning normally,” Tal said. “When you have the number of transactions going down so rapidly, and you’re basically frozen, the signal that you’re getting from the market is a misleading signal.

“It’s not a real signal because it’s biased and very small.”

Tal said real estate valuations being made now have very little value and people should be careful about making decisions based on the current economic situation.

“For the real estate market, if this recovery is going to be relatively long, it means that interest rates will remain relatively low,” said Tal. “That’s positive.

“I think the damage to the real estate market isn’t as significant as perceived.”

Tal expects the Canadian economy to emerge from the recovery phase in 2022 or 2023 and that “the demand for real estate will remain very strong.”

Impact on Canada’s housing market

Tal said the Canadian housing market was at a “very, very, very good” starting point before the current crisis.

This is easing the pain brought about by housing activity dropping 70 per cent compared to a year ago. Supply and demand are both down.

“We’re seeing some significant delays in completions, especially in the high-rise segment of the market,” said Tal.

Problems include getting materials from other countries and increased physical distancing on construction sites, which reduces productivity by 40 to 50 per cent.

A total of 30,000 condominium completions were projected in the Greater Toronto Area in 2020, but the final tally won’t come close to that.

Housing starts will slow dramatically across Canada, contributing to a lowering of the GDP. While things will improve next year, Tal doesn’t expect the numbers will return to pre-crisis levels.

There were large job losses across Canada in March and April, a high proportion of them low-paying. Most of those people live in rental housing.

Tal is adamant, however, that the Canadian rental housing market is not in danger of collapse.

Somewhat surprisingly, Tal said the rent payment rate among those low-income earners was higher than for Canadian renters in higher income brackets.

He attributes this to many low-earners now receiving a $500 weekly Canada Emergency Response Benefit payment from the federal government, which they’re using to pay rent.

Many also live in rent-controlled apartments where they’re paying well-below-market-value rents. They’ll do whatever it takes to pay to keep living there.

While reports claim 85 to 90 per cent of apartment rents were collected in April, Tal thinks that number will go down in May.

The number of immigrants and non-permanent residents in Canada will decrease this year. A large percentage of those people are also renters, which will decrease demand for rental housing.

Tal expects that to be balanced out somewhat by a reduction in supply due to a lack of apartment building completions, so the vacancy rate increase won’t be dramatic.

Commercial real estate sectors

There have been predictions of a collapse in office building values because of reduced demand owing to an increased number of people working from home.

The pandemic accelerated that trend but Tal expects it to be offset, to a degree, by the desire to dedicate more space to each employee as a means of physical distancing.

“Vacancy rates might be rising and I think that rent inflation will go down a little bit, as we have seen in every recession,” he predicted.

“But at the same time, I think that those who predicted that this market will collapse are overstating the damage. I don’t think that the move towards people working from home will be as dramatic as perceived, given the productivity aspect.

“Even if you lose 20 per cent of people working in the office, you will have to build bigger, which means that you have a situation in which the demand for space will be relatively steady or maybe reduced a little.”

The momentum of e-commerce started years ago and will continue to build, but at a faster rate. More people have started online shopping by necessity because most stores are closed and people aren’t leaving their houses.

This will have an obvious impact on retail real estate, which has already encountered challenges over the past few years.

“High-quality retail will remain in demand, and in fact it will improve,” said Tal. “I see significant damage to low-quality retail. This means that you will see e-commerce taking over.”

Tal didn’t address industrial real estate, beyond saying he’s still bullish on the sector.

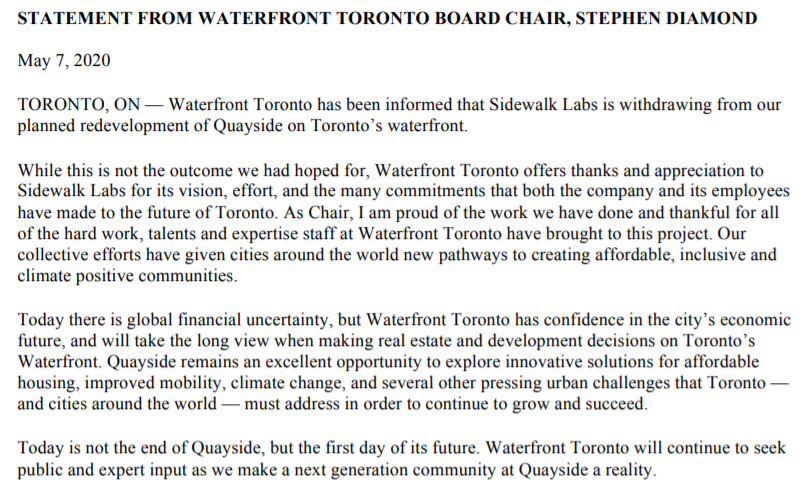

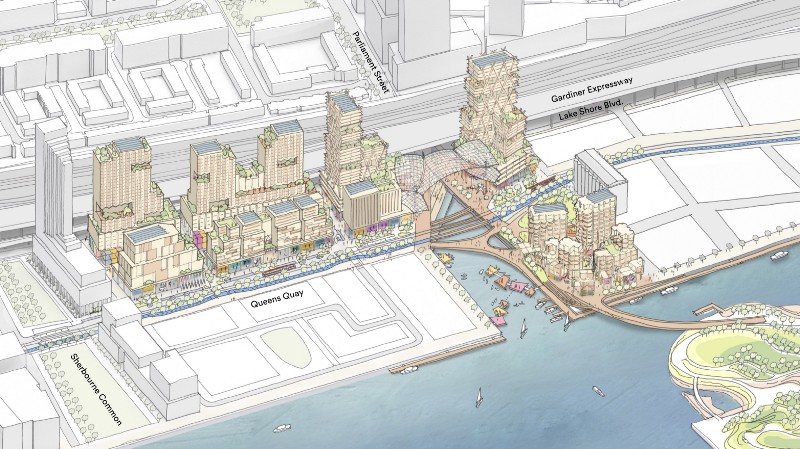

TORONTO – Sidewalk Labs‘ ambitious vision for a hi-tech neighbourhood equipped with futuristic innovations won’t be coming to Toronto’s waterfront.

The Google affiliate revealed Thursday that is walking away from its controversial, smart city plans after spending years and millions of dollars on the proposal.

”As unprecedented economic uncertainty has set in around the world and in the Toronto real estate market, it has become too difficult to make the 12-acre 1/8nearly five-hectare 3/8 project financially viable without sacrificing core parts of the plan we had developed,” Sidewalk’s CEO Dan Doctoroff said in a letter posted online that broke the news.

The day before, he had informed Waterfront Toronto, a tripartite agency in the process of deciding whether to allow Sidewalk to pursue the plan, of the decision.

”While this is not the outcome we had hoped for, Waterfront Toronto offers thanks…to Sidewalk Labs for its vision, effort, and the many commitments that both the company and its employees have made to the future of Toronto,” Waterfront chairman Stephen Diamond said in a release.

The decision signalled an end to the rocky relationship between Sidewalk and Waterfront that has festered for years as the project was met with criticism around privacy protections and intellectual property concerns from business leaders and security experts alike.

It all began in 2017, after Sidewalk won the right to develop a proposal for the swath of lakefront land from Waterfront that was underdeveloped and underserved by transit and other key city amenities.

Critics instantly complained about a multibillion-dollar, American corporation creeping into the country and getting its hands on prime land that could have been developed by homegrown enterprises. They worried about what would happen with data collected form a myriad of sensors and devices throughout the neighbourhood.

Doctoroff and Sidewalk kept forging on and in June 2018 unveiled a 1,500-page plan showing Sidewalk was willing to spend $1.3 billion on the neighbourhood.

It would adorn it with ”raincoats for buildings” that can provide cover or be opened with better weather, and heated and illuminated sidewalks, which it built prototypes of at its Lakeshore Boulevard office that employed 30 people.

Affordable housing, tall timber structures and innovations to support sustainability and environmentalism would be part of the neighbourhood too.

Sidewalk boasted that the project would create 44,000 jobs, generate $4.3 billion in annual tax revenues and add $14.2 billion annually in gross domestic product for Canada.

Instead of the nearly five hectares, most believed Sidewalk was working on a proposal that spanned 77 hectares – 16 times the original size.

Diamond and Waterfront weren’t happy. By October, they had convinced Sidewalk and Doctoroff to scale back and refine their approach to five hectares.

Sidewalk also agreed to store and process data collected from the project in Canada, pay fair market value for the land at the time of sale, team up with one or more real estate partners and allow Canadian companies to use Sidewalk’s hardware and software patents.

If the smaller project was successful, Waterfront said Sidewalk could seek to develop more land, but a formal process would need to take place.

Since that October decision, Waterfront had been weighing Sidewalk’s proposal and was meant to decide in March whether the project should move forward. COVID-19 pushed that decision back to May and even if Waterfront had given Sidewalk a green light, municipal, provincial and federal approvals would have been needed before any shovel hit soil.

Though without its tech giant partner and amid a pandemic, Waterfront still seems to want to revitalize the area.

”Quayside remains an excellent opportunity to explore innovative solutions for affordable housing, improved mobility, climate change, and several other pressing urban challenges that Toronto – and cities around the world – must address in order to continue to grow and succeed,” Diamond said in his release.

”Today is not the end of Quayside, but the first day of its future. Waterfront Toronto will continue to seek public and expert input as we make a next generation community at Quayside a reality.”

Toronto Mayor John Tory echoed those sentiments, saying the decision had not changed his mind about their being a ”tremendous” opportunity to develop the area.

”I am extremely confident there are partners eager to undertake this endeavour,” he said in a release.

”Our goal remains to ultimately build a neighbourhood focused on innovation in Quayside that will be the envy of cities around the world and a beacon for the future.”

You know what they say: The show must go on.

While that’s not true of everything amid the COVID-19 pandemic, it’s true when it comes to the biggest transit project in Mississauga’s history.

If you regularly commute down Hurontario Street in Mississauga, you should note that some delays are possible due to a grand-scale construction project.

Metrolinx recently announced that commuters can expect new construction on Hurontario in preparation for the Hurontario LRT project.

The LRT, a $1 billion higher-order transit project being carried out by Metrolinx, will span 18 km and run from Port Credit GO at Lakeshore Rd. in the south to the Brampton Gateway Terminal at Steeles Ave in the north.

The LRT will boast 19 stops and provide connections to the Port Credit and Cooksville GO stations, Mississauga Transitway, MiWay and Zum transit lines.

Initially, it was slated to run 20 km and feature 22 stops, but Metrolinx recently announced it was chopping the City Centre loop to reduce costs.

What construction is coming up soon?

News that Canadian financial institutions were offering some mortgage deferrals sent investors running to the banks in early April, asking for a stay on their payments as personal incomes and investment portfolios were being wiped out by the coronavirus pandemic. Those deferrals seem like a lifeline for investors facing a liquidity crisis, but one leading mortgage broker thinks the impacts of a deferral need to be considered closely.

Dalia Barsoum, president and principal broker at Streetwise Mortgages, says that investors should consider alternatives to mortgage deferrals. She explained that these deferrals aren’t gifts or grants, as they come with a cost, a likely increase to future payments, an impact on future financing availability and a wider implication for an investor’s credit. Barsoum says despite the pain investors are feeling, they shouldn’t just take mortgage deferment as their first line of support.

“We look at mortgage deferrals as a last resort tool for investors to utilize to help ease financial destress,” Barsoum says.

Barsoum outlined what some of those sources of financial distress are. The primary pressure on real estate investors stems from unemployment, both the loss of their own job or, if they own a rental property, the loss of a tenant’s income. The temporary collapse of Airbnb, too, has resulted in an increase to rental stock in some Canadian markets, putting downward pressure on rents. Further, softening property valuations in some markets, have made it more challenging to extract equity when it is needed most. Even committed deals, not yet closed, might be torpedoed by a borrower’s inability to get a mortgage. The financial pressures on a real estate investor are widespread, perhaps enough to make mortgage deferral seem like the right option. Barsoum says investors need to look at the long-term implications of that short-term fix.

Her first concern is cost, explaining that interest will accrue on the deferred amount for the duration of the period. Each lender, too, applies its only methodology of repayment for the accrued amount after the deferral period. Investors need to know what that post-deferral arrangement will look like before they sign off on anything.

That methodology could also result in an increase to future monthly payments. That increase will vary based on the mortgage size, interest, and duration of the deferral. An increase in the debt load will, as well, likely impact an investor’s ability to qualify for future financing, especially if their new payments are higher across several properties within the portfolio.

Though a deferral is different from a default, and should not have any negative impact on credit, that requires an adjustment to lenders’ systems allowing them to report deferrals in the right way. Barsoum thinks that the sheer volume of deferral requests has increased the risk of reporting errors.

“If you are considering a deferral and can wait on it another month, then please do so to allow time for the first round of deferrals to go through the systems and see how that turns out,” Barsoum says. “Further, if you have chosen to defer by now, then please monitor your credit report for the next 3 months.”

Current financing arrangements, too, could prove challenging to obtain for investors with an active deferred payment. The logic, as Barsoum sees it, is that in taking a deferment an investor has told the lender whether they “can or can’t” afford the payment. In such a binary situation, taking the deferment puts you in the “can’t pay” camp, which carried long-term implications.

“My suggestion is to first examine your finances, challenges and plans with your current mortgage advisor,” Barsoum says. “Come up with an action plan before jumping on mortgage deferrals as the first line of support because of panic, fear of the unknown, or fear of missing out on this support tool.”

As the real estate market continues to take hit after hit as a direct result of COVID-19, with both prices and sales down in the Greater Toronto Area (GTA), it’s hard to imagine we’ll be on the other side of the pandemic any time soon.

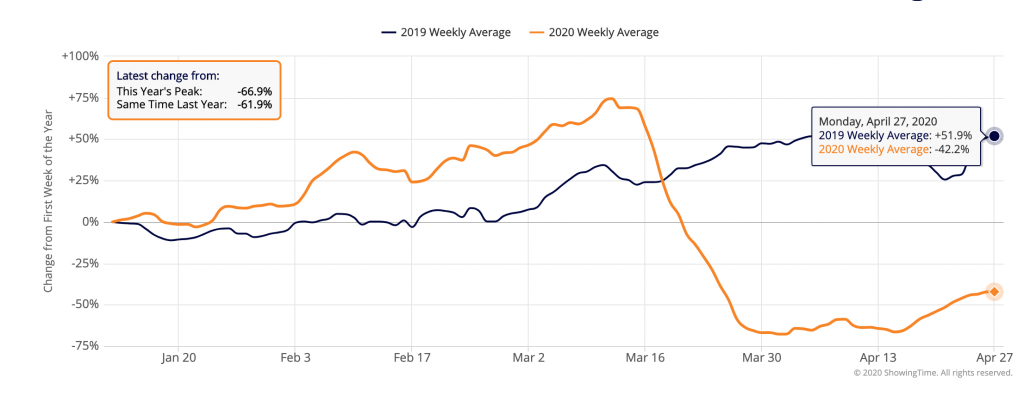

But, if it’s any consolation, Toronto home sales finally started to see some slight improvement in the past week and real estate showings are also gradually starting to increase in Ontario, proving that there is still an underlying demand from prospective buyers, albeit at a very different level than what you might typically see in the province at this time of year.

According to data from ShowingTime, a market stats and showing management technology provider for residential real estate, the initial drop in showing activity seen throughout March — as stay at home and social distancing orders were implemented — has given way to show “modest” signs of stabilization as agents are turning to virtual showings in the areas where ShowingTime operates, which includes Alberta, Ontario, and Nova Scotia in Canada, as well as many states across the US.

“Through mid-March, year-over-year showing activity was higher nationwide compared to 2019. The current volume is indicative of the industry’s response to COVID-19, which is changing daily,” said the company in a statement.

To provide daily updates charting homebuyer showing activity across the markets it serves, ShowingTime analyzes weekly real estate showing data from the first calendar week of January, through April 27, 2020, with a 7-day moving average.

Here in Ontario, you can see showing activity had been gradually increasing since the start of the year up until around March 16, when COVID-19 emergency orders were implemented and real estate showings were halted, before plunging on March 30 to the lowest weekly average of the year at -65.7%. However, as we eased into the new month, showings started to slowly pick up, before seeing a significant increase leading up to April 27 to reach a weekly average of -42.2%, nearly a 25% uptick from its lowest point.

While the showing activity shift might be minor, it’s definitely an indicator that buyers and sellers are still interested in making transactions happen – pandemic or not.

The data points represent a rolling weekly average in ShowingTime’s 100 top markets, with each market recording tens of thousands of appointments in 2019 and 2020.

space is the new luxury,” says Max Hahne, broker of record at Engel & Völkers Collingwood Muskoka.

It turns out that no matter how nice a house or condo you have in the city, during a pandemic, you’re still in the city. And the restrictions COVID-19 has placed on Toronto residents have led many homebuyers to start looking north to cottage country.

“In the third week of March we were still seeing the same number of inquires, but we’ve been seeing an uptick in the number physical showings since Easter,” Hahne says over the phone. He says much of the interest he’s seeing is coming from Toronto homebuyers who looking to permanently move out of the city to find a rural, recreational home. He also notes that Engel & Völkers follows strict guidelines in order to be able to show a home during this time, including signed declaration forms regarding health and travel, offering masks and gloves, and ensuring all parties involved maintain proper physical distancing.

COVID-19 has changed how people view both their lives and their living situations. For instance, Hahne says he has a lot of prospective buyers who, directly because of COVID-19, have realized they don’t need to be in the office every day to be successful at their jobs, or even those who have simply decided to retire earlier than they may have before the pandemic.

And, above all, buyers are interested in space.

“Most of the properties I’m showing are in the $2-3 million range and they’re almost all on larger acreage. I’m getting a lot of ‘sign calls’, people are literally sitting in front of a property and calling us up to ask us for more details.”

Hahne thinks at least some of the reasons for this is that so many people have found themselves stuck at home and they’re deciding to spend a lot of their time looking at real estate. Popping out for a four-hour return drive to get a sense of a property north of the city suddenly doesn’t seem like a huge effort when there’s not much else you’re allowed to do that day.

“Our Muskoka lines are ringing off the hook right now,” says Hahne. Mostly, it’s important to note, it’s very wealthy clientele who are reaching out. The kind of people, Hahne says, who had to cancel their European vacation and are now looking to either rent or buy a cottage where they can spend the summer with their family. The cottages these buyers are after are in the $5 million-plus range, and can easily rent for $100,000+ a month.

Which is to say, not everyone’s looking to Collingwood and Muskoka when it comes to buying a new home right now. But for those that are turning to cottage country – space is not the limit.

TORONTO — The Ontario government has announced that certain businesses and workplaces can reopen on Monday with strict public health measures in effect.

The government said businesses permitted to reopen include seasonal businesses and some essential construction projects.

“Right now, there are certain businesses and workplaces that can operate safety,” Premier Doug Ford said Friday. “That means they can physically distance their staff and customers, they can put in physical barriers, they can provide contact-free services, or they work outside and are isolated.”

The premier said allowing some businesses to reopen follows advice from the province’s chief medical officer of health. Ford said he also believes, in the near future, additional businesses will be allowed to reopen.

“We have made tremendous progress,” Ford said. “We are flattening the curve, we are heading in the right direction.”

Ford said today’s announcement marks an “important starting point” in Ontario’s path to reopening the economy.

“We can take today as a sign,” he said. “Today’s news shows us that if we stay the course, stay vigilant, and take a measured approach, we can keep moving in the right direction.”

“We can keep moving ahead with the opening up of the economy. We still have a long way to go but today is a glimmer of hope.”

The government said following proper health and safety guidelines, these businesses can reopen as of May 4 at 12:01 a.m.:

- Garden centres and nurseries with curbside pick-up and delivery only

- Lawn care and landscaping

- Additional essential construction projects that include: shipping and logistics, broadband, telecommunications, and digital infrastructure; any other project that supports the improved delivery of goods and services; municipal projects; colleges and universities; child care centres; schools; and site preparation, excavation, and servicing for institutional, commercial, industrial and residential development

- Automatic and self-serve car washes

- Auto dealerships, open by appointment only

- Golf courses may prepare their courses for the upcoming season, but not open to the public

- Marinas may also begin preparations for the recreational boating season by servicing boats and other watercraft and placing boats in the water, but not open to the public. Boats and watercraft must be secured to a dock in the marina until public access is allowed.

The news comes a day after the provincial government released a list of sector-specific guidelines industries must follow in order to reopen.

The government said the new safety guidelines provide direction to various industries including retail, health care, manufacturing, tourism, restaurant and food service, offices, construction sites, and transit and transportation services.

The premier unveiled a three-phase plan on Monday to reopen following weeks of shutdown.The plan, dubbed “A Framework for Reopening our Province,” states the parameters of each “gradual stage.”

Ontario’s Chief Medical Officer of Health Dr. David Williams was asked about which businesses may open next, to which he replied that the decision ultimately lies with the government.

“It depends on what the government decides,” Williams said, adding that the process of reopening businesses is a “big job.”

Ontario health officials confirmed 421 new cases of COVID-19 and 39 more deaths.

The new patients reported Friday bring the total number of novel coronavirus cases in Ontario to 16,608, including 1,121 deaths and 10,825 recoveries.

Nearly two weeks into an aggressive physical distancing campaign aimed at curbing the spread of the novel coronavirus, cases are doubling at a slower rate in Canada than elsewhere, and hospitals are not yet overwhelmed, public health experts say.

But it’s too soon to tell how well the country will fare.

Because Canada’s COVID-19 situation is about two weeks behind the U.S. and months behind Italy and China, it’s hard to tell how the country will rank globally, said Dr. Barry Pakes, an assistant professor at the University of Toronto’s school of public health.

“What some countries looked like two weeks ago we look like now—maybe a bit better—but we’re still in early stages,” Pakes said.

It takes about three to four days for cases in Canada to double, whereas it only takes about two days in the U.S. and Italy, said Dr. Barry Pakes, an assistant professor at the University of Toronto’s school of public health.

He added that people need to continue aggressive physical distancing, which requires Canadians to stay at home as much as possible and to keep at least 6 feet apart from one other.

By limiting virus spread, public health officials say Canadians can prevent a dramatic spike in new cases overtime—or “flatten the curve”—and decrease the strain on our healthcare system.

Canada’s top medical official, Dr. Theresa Tam, has strengthened the expression, urging Canadians to “plank the curve” instead.

The coronavirus has skyrocketed in Canada, which now has more than 4,000 confirmed or probable cases and 39 deaths. Nearly half of newly diagnosed cases were caused by community transmission, meaning there are no known links to travel or no known source.

The increase in cases is partially a result of Canada’s efforts to ramp up testing. As of Friday morning, the country had administered more than 160,000 COVID-19 tests—an average of 10,000 tests per day.

On Thursday, Tam said that even though we’ve seen an increase in COVID-19 cases, Canada’s hospitals are not yet overwhelmed. About 6 percent of COVID-19 cases require hospitalization and 1 percent of cases have been fatal, she added.

“Anyone unconvinced about the seriousness of COVID-19 and the absolute need for physical distancing need only look to countries like Italy to see the severe impacts of a health system overwhelmed,” Tam said.

According to Pakes, Canada’s fairly strong leadership—both political and scientific—puts the country in a better position than the U.S.

The U.S. now has the highest number of confirmed COVID-19 cases at 70,000, surpassing case counts in China and Italy.

It will likely be the new pandemic epicentre, according to the World Health Organization.

While many states and municipalities in the U.S. are handling the pandemic well, the country lacks a coordinated, streamlined response, Pakes said.

In Canada “we have political leadership that we do in many ways trust,” Pakes said, adding “that’s not necessarily the case in the U.S.”

And even though it’s too early to gauge whether Canada is successfully flattening its curve, Pakes said the country is somewhat lucky that its COVID-19 timeline is behind other countries.

“We can learn from our neighbours to the south that aren’t necessarily doing the right thing,” Pakes said.

MONTREAL ― The COVID-19 economic crisis has shuttered our cinemas and airlines, thrown restaurants and bars into disarray and is currently busy running up a heck of a government deficit.

But apparently it can’t derail Canada’s housing markets, many of which can expect to see rapid house price growth once the outbreak passes, several recent forecasts have predicted.

Despite a steep drop in sales this year, the average home price in Canada will be 6.1 per cent higher at the end of this year than it was a year earlier, TD Bank said in a forecast issued this week.

Given that incomes are unlikely to rise much during this crisis, “affordability will deteriorate when you look at house prices,” the report’s author, economist Rishi Sondhi, conceded.

Sales may be falling, but the supply of homes on the market is falling with them, Sondhi said, which means the market balance isn’t shifting much.

Many people are hesitant to put their house on the market ― either because of concerns about the virus, or concerns about the health of the market.

“Sellers are moving to the sidelines just as rapidly as buyers are,” Sondhi told HuffPost Canada.

“We might be in a situation where (prices) start to accelerate into the uncomfortable zone.”

Peter Norman, VP and chief economist, Altus Group

Still, TD’s forecast makes a few big assumptions. One is “that provinces take tentative steps towards re-opening their economies over the next month.”

Another is that the country won’t see a sudden rush of people who need to sell their homes quickly, thanks to the banks’ new mortgage deferral programs.

Not everyone agrees. At least one recent forecast says the country will likely see some “forced selling” in the housing market.

And what about the millions of Canadians who have lost work in this crisis? Won’t their plight affect house prices?

Like some other economists, Sondhi says that won’t have as much impact on the housing market as one would think.

That’s because, they say, the jobs lost in this crisis have disproportionately affected people in service industries ― think customer service reps and Starbucks baristas ― and these people overwhelmingly tend to rent.

“While it is sad that these people skewed strongly to young and to part-time workers, for the housing industry, the impact of these presumably temporary job losses will be limited as these groups are much less likely to buy and sell real estate,” Phil Soper, president and CEO of real estate agency Royal LePage, said in a report earlier this month.

TD’s forecast sees Toronto house prices rising 7.8 per cent this year, compared to last year, while Vancouver will see 4.7 per cent growth. Things will look worse on the Prairies, TD predicted, where the oil slump will lead to a 4.7 per cent price decline in Alberta, and a 4.1 per cent drop in Saskatchewan.

“Sales are poised to plunge at an historic pace in April, while gradually recovering their lost steps in subsequent months as buyers remain cautious,” the report states.

‘Uncomfortable zone’

In a separate report Wednesday, real estate services firm Altus Group predicted a more than 50 per cent drop in home sales in the April-June period this year, before bouncing back in the second half of 2020, to end the year at around 10 per cent below the previous year’s sales.

Although there is a “broad range of outcomes” possible in these uncertain times, ”it’s very unlikely we’ll see significantly declining house prices,” Altus Group vice-president and chief economist Peter Norman told HuffPost.

“The odds are better that … we might be in a situation where they start to accelerate into the uncomfortable zone.”

He predicts price growth in the 5 to 10 per cent range for this year, because there will be many buyers who will be “ready to buy” once shutdown orders are lifted and social distancing rules start to be eased.

“We think this recession is going to be deep but quick, and the economy will recover quite quickly as soon as we substantially get through the health crisis,” he said.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

416-599-9599 ext:150 Cell : (647) 699-5900

HomeLeaderRealty.com

ListOfCondo.com

LocateCondo.com

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

416-599-9599 ext:150 Cell : (647) 699-5900

HomeLeaderRealty.com

ListOfCondo.com

LocateCondo.com

Privacy Policy

Privacy Policy