Whether they take place during a pandemic-fuelled recession or during a period of sustained economic expansion, record-shattering home sales in Canada always seem to be accompanied by the same phenomenon: talk of the country’s “inevitable” housing crash.

Questioning the logic of homebuyers who engage in wild bidding wars in the midst of historic job losses is hardly unreasonable, but saying that behaviour will trigger a catastrophic fall in home prices, like the 18 percent decline projected as a potential outcome by the Canada Mortgage and Housing Corporation in May, is a train of thought Nick Kyprianou, president of RiverRock Mortgage Investment Corporation, is encouraging Canadians to abandon.

Talk of a crash in home prices has been persistent since CMHC first floated its dire 18 percent figure, even though neither CMHC nor any other housing authority, lender or brokerage has provided any evidence or metrics that tie current market activity or the economic slide caused by COVID-19 to plummeting home prices. And yet, the spectre of an 18 percent decline persists, hanging over the market like the reaper’s scythe, just waiting to harvest the souls and credit ratings of unfortunate Canadians.

Kyprianou is another market-watcher who can’t fathom the CMHC’s projection. His theory is that, in determining its absolute, institution-destroying, worst-case scenario as part of its annual report to the Office of the Superintendent of Financial Institutions, CMHC may have concluded that its own breaking point would come if home prices shrank by 18 percent.

“I think [CMHC CEO Evan Siddall] just spouted off the worst-case scenario,” Kyprianou says. “Well, the chance of the worst-case scenario is so remote, everything has to line-up perfectly – multiple times – for it to happen.”

Using five key metrics to compare the current economic situation to that which proceeded the last true housing crash in Ontario (1989-1995), Kyprianou says today’s consumers can remain confident that home values will largely maintain their strength, even as COVID-19 continues to cast its shadow over the Canadian economy.

1. Interest rates

“Interest rates are your biggest factor,” Kyprianou says “If interest rates keep going up, that’s the biggest burden on housing because your dollar just doesn’t go as far.”

Interest rates almost doubled during Ontario’s last crash, rising from from eight to fifteen percent, putting pressure not only on buyers but the province’s builders as well. That is simply not going to happen this time around. The Bank of Canada estimated that it may not raise its key interest rate target before 2022.

2. Unemployment

There is no question that Canada’s employment situation is a worry. Unemployment was 10.2 percent in August 2020, almost double the rate seen in August 2019. But Kyprianou says there’s more to the story than just the headline.

In the early 1990s, when unemployment was hovering around 11 percent, most of the jobs being lost belonged to high earners – middle management, skilled tradespeople, factory workers – who saw their employers close up shop and move their operations to countries like Mexico during the first rocky years of the North American Free Trade Agreement.

“When these jobs are evaporating and the bulk of the unemployed are the higher income earners, that is going to have an effect on housing,” Kyprianou says, adding that most of the labour disruption caused by COVID-19 has been proven to involve low-wage earners who are predominantly renters, not prospective home buyers.

“That’s a big dynamic change,” he says. “You just can’t look at what the unemployment number is. You have to drill down through it and look at who is unemployed.”

3. Equity

Much of the concern expressed by CMHC’s Siddall over Canadian debt levels and high-ratio mortgages is the risk of borrowers being dragged underwater if falling home prices leave them in a negative equity position. Fair enough. But Kyprianou, quoting statistics provided by Canadian Mortgage Professionals, says the vast majority of Canadians have far more than five percent equity in their homes.

In its most recent Annual State of the Residential Mortgage Market in Canada report, CMP found that 88 percent of Canadian homeowners have equity ratios of 25 percent or higher. Among the 6 million homeowners with mortgages, 81 percent have equity ratios of 25 percent or more.

Kyprianou says there is also the concept of emotional equity to consider. Defaulting on a mortgage is seen as an embarrassing failure most homeowners will do all they can to avoid. He saw many of them get resourceful during the last recession – taking on boarders, getting a second job, asking their families for assistance – as a means of making their monthly mortgage payments. He expects the same level of effort from today’s borrowers.

“You gotta make it work,” he says.

4. Taxes

In the early 90s, sky-high personal and corporate tax rates were deemed responsible for driving companies and individual professionals into the waiting arms of the United States. The resulting brain drain eventually led to lower tax rates in Canada, but the damage was done.

With unemployment high and business confidence muted, it is highly unlikely that taxes will see any kind of significant spike over the near-term. Canadians are likely to be up in arms when their CERB payments are taken into account come tax time next year, and the billions in government aid used to prop up the economy for six months will eventually need to be recouped, but it’s safe to say the feds won’t threaten the nation’s economic recovery – or their polling numbers – by implementing any significant new taxes.

5. Immigration

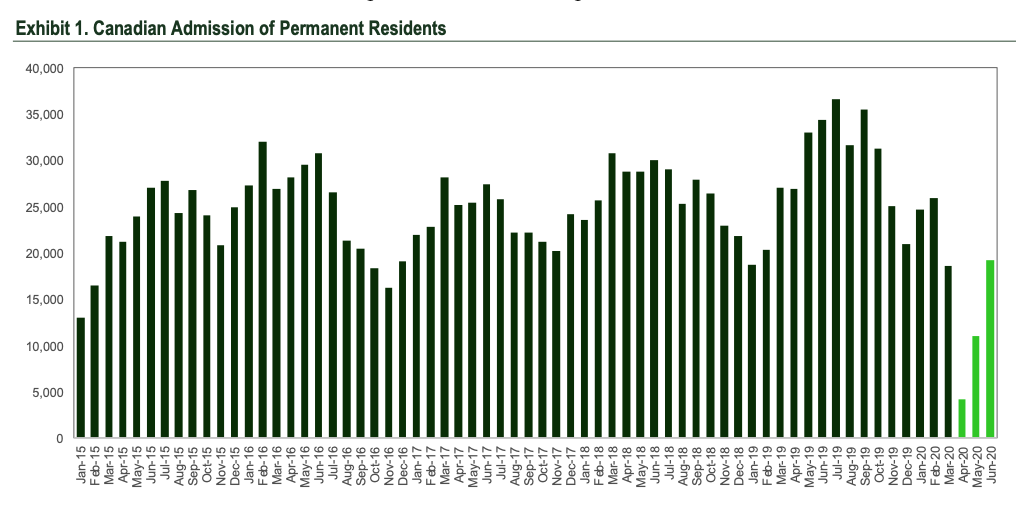

In the 1989-1995 downturn, the problem wasn’t a lack of new Canadians, it was an inability to keep them. The brain drain days are over, but by limiting international immigration, COVID-19 has thrown a wrench into the works. With just over 100,000 permanent residents being welcomed into the country in the first six-months of 2020, Canada has little chance of hitting its immigration target of 341,000 for the year.

Immigration has been a significant driver of all things good in Canada over the past several years – population growth, innovation, economic expansion, home sales – but Kyprianou doesn’t see a fall in immigration numbers having too negative an impact on home prices, largely because immigrants don’t tend to buy properties for the first two years after arriving in Canada.

“If the pandemic affects immigration for three years, it’s not going to be a problem,” he says. “If it’s just a year, year-and-a-half, it’s not going to be a problem.”

Canada’s reputation for being a stable presence in a chaotic world has also been strengthened by the country’s handling of the pandemic (and the humiliating failure of our neighbours to the south to do the same). Once recovered from COVID-19, the country should still offer the same opportunity for new arrivals to find not only a safe environment to raise their families, but high-paying jobs in growing industries like tech and financial services.

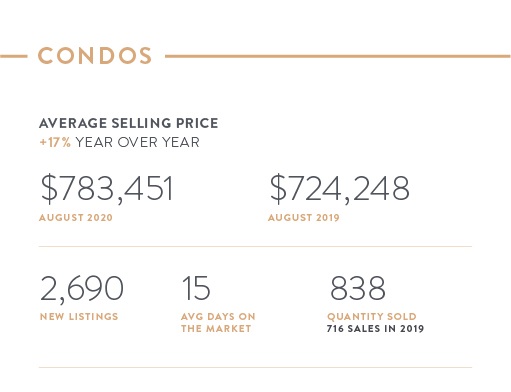

The only sub-market where Kyprianou sees prices softening is high-rise condos. But with so many investors having purchased rapidly appreciating pre-construction properties over the past five years, even those who may be forced to sell, like unlucky Airbnb operators, are unlikely to face a loss. If the average price per square foot in Toronto, for example, falls from its current level of approximately $1,100 to $900, anyone who purchased at $500 per square foot in 2015 will still be making a hefty profit.

“It’s not like there’s going to be a bloodbath,” Kyprianou says. “They just don’t make as much money if they have to sell.”

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2