Canada is in election mode, and all politicians have a plan to cool real estate markets. The thing is, most markets have begun to cool on their own. Canadian Real Estate Association (CREA) data shows a third of markets made a monthly pullback in July. The trend is likely to get stronger as well, as over 4 in 5 real estate markets have seen annual growth drop. There’s still a long way to go before it would be a “correction,” but it may be a sign cooling measures aren’t as urgently needed.

Momentum And Price Growth

Every new trend starts with a change in direction. The momentum of price growth is one of the most important measures of this. It drops a few hints on the direction of where the market is heading, and how people may react.

When price growth accelerates, the rate of growth is rising. If it abruptly begins after a downturn, it may be marking the bottom of the market. Early in this stage is when buyers make the most money, and feel the luckiest. As the trend accelerates, sellers have more incentive to hold onto their property. It doesn’t matter if it’s negative cap, as long as it rises in value, right? The faster prices accelerate, the less likely an investor is to sell. Ironically, this means lower inventory, potentially accelerating prices further.

Price growth deceleration is when the rate of growth is getting lower, or even negative. If this happens after a period of acceleration, it can mark the top of the market. This is when sellers make the most money, and feel the luckiest. As the trend decelerates, more buyers tend to stand back and delay their purchases. Often they’re waiting to see if prices fall. The FOMO to jump into the market immediately may also disappear. If you’re not as worried about being “locked out” of the market, you’re not in as much of a rush to purchase.

The best time to sell is often the worst time to buy. Conversely, the best time to buy is often the worst time to sell. It’s tricky identifying when those turns happen. The momentum of price growth is a pretty good starting point though. Remember, that’s starting point. Not your comprehensive, single-point market guide.

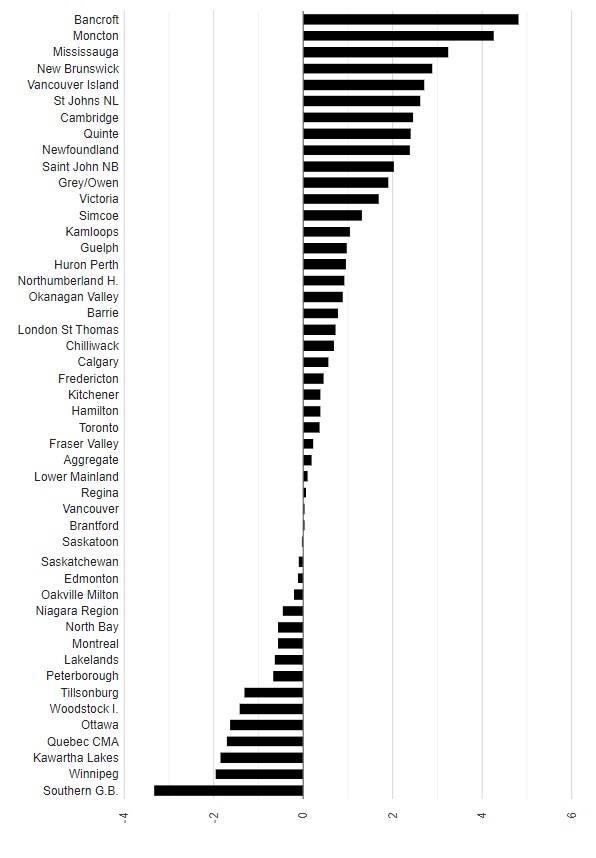

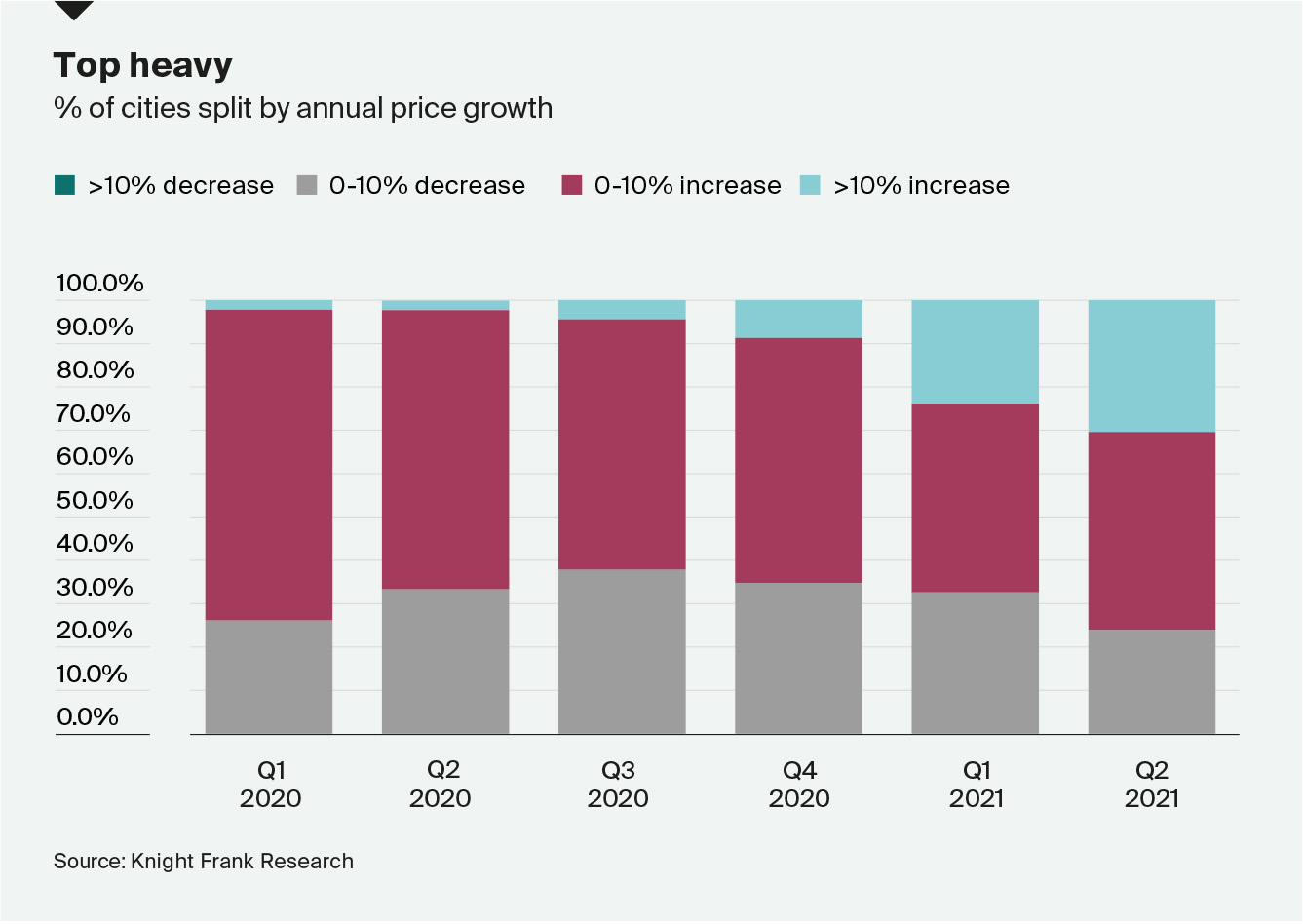

A Third Of Canadian Real Estate Boards Reported Lower Prices In July

First, let’s start with which markets are actually pulling back in dollar terms. A third of boards, 16, reported monthly drops for the July composite benchmark. Data also shows 38 markets printed smaller monthly gains than the previous month. Prices don’t move in a straight line, so some variance should be expected. Once it turns into the annual trend changing direction though, it’s harder to see a turnaround.

Canadian Real Estate Price Monthly Change

The monthly change in the composite benchmark price of a home for July 2021.

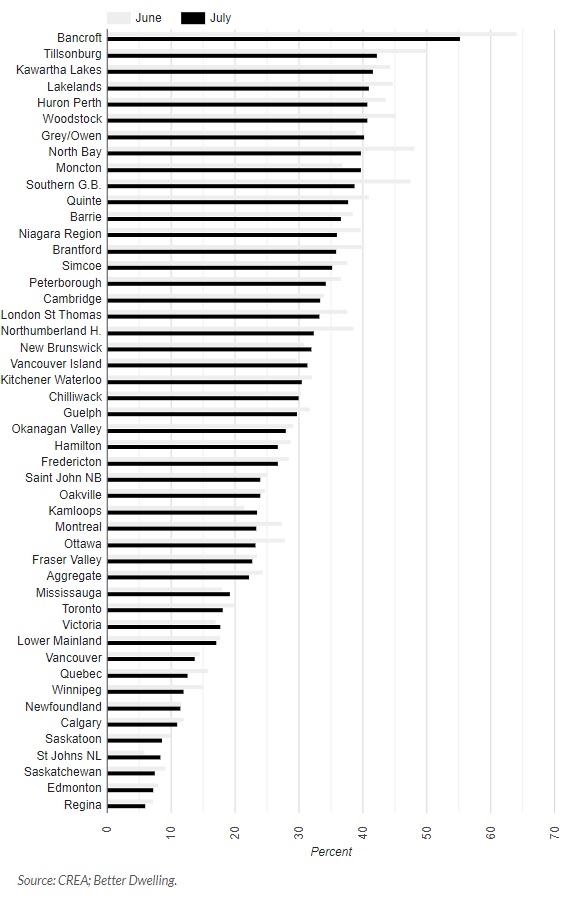

Over 4 In 5 Real Estate Markets Saw Annual Growth Decelerate

Annual growth of composite benchmark price has dropped in the majority of markets. Over 4 in 5 markets reported the annual rate of price growth as fallen. Just 8 markets have seen flat or accelerated price growth. Some of these rates are astronomically high, so it’ll take a while to get back to reality. But once these trends start to fall, a catalyst is often needed to reverse them. It’s an election though, so a capital injection in the name of affordability might be seen. Never underestimate how poorly bureaucrats can misread the market.

Canadian Real Estate Price Annual Change

The annual change in the composite benchmark price of a home for July 2021.

Most markets are now seeing a deceleration in price growth. It’s also happening during falling home sales, which is interesting. Most industry observers have attributed falling sale volumes to a lack of inventory. However, if the shortage of inventory was the problem, prices would be rising. They aren’t. This is one of those narrative-reality mismatches.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2