Would you move further out of the city to secure the type of home you’re looking for within budget?

Given how popular work from home has been in the last few years, the option to choose home type first and city second is opening up to more buyers in Southern Ontario.

In fact, a Zoocasa survey early last year found that the pandemic has led to 32% of Ontario buyers purchasing a property in a location further than what they would have previously considered – and given the consistent price increases recorded across the province throughout 2021, it’s safe to say that trend has continued.

Buyers who have their eye on a certain type of home, whether that’s a condo in the city centre or a townhome with a yard for their dog, can save big if they can be flexible on which city in the Toronto Region they’d like to make their purchase in.

To help prospective buyers narrow down which areas they should consider focusing their house search in, Zoocasa has ranked the top five most affordable cities within the bounds of the Toronto Regional Real Estate Board to buy a detached home, semi, condo townhouse, and condo apartment based on November 2021 sales data*.

In other words, if finding the right type of home at the right price point is more important to you than buying in any particular city, this report is designed to help you discover which cities to consider in your home search.

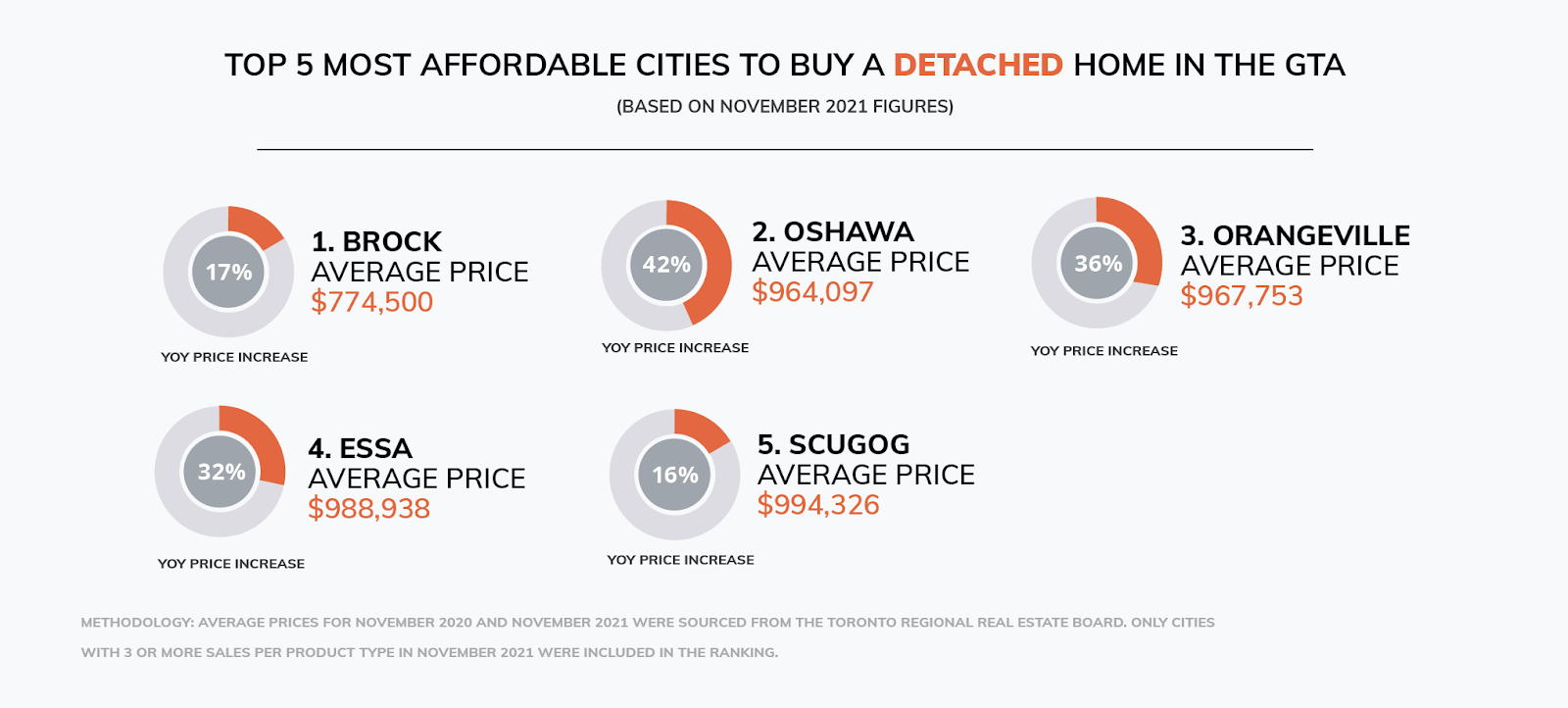

Brock is the Most Affordable Place to Purchase a Detached Home

Although the average price for a detached home in the Toronto Region hit $1,567,832 near the end of last year the top five most affordable cities to buy a detached home in the greater region all clock in with an average price under a million dollars – a significant savings of more than $500,000.

Brock, the most affordable city on the list, is a small town in the north end of Durham township. As of 2016, the population reached just over 11,000 – making it a great choice for buyers looking for more space and a small-town lifestyle.

With an average price of $774,500, detached homes here are half the price of the region’s average. However, affordability comes with a proximity tradeoff. Brock is located in the Toronto Region’s farthest north reaches, and nearly borders Lake Simcoe. In good traffic conditions, you can reach Union Station by car in a little over an hour and a quarter, but Barrie and Peterborough are both closer cities – meaning you likely won’t want to commit to a daily, downtown Toronto commute if you’re living here.

If you’re looking to live a little closer to Toronto’s core, Oshawa and Orangeville both offer better connectivity to the rest of the GTA, with detached homes still coming in at an average price of less than a million. If you’re looking for small-town living, Essa (near Barrie) and Scugog (near Port Perry) are other options on the list that round out our top 5 most affordable places to buy a detached home in the Region.

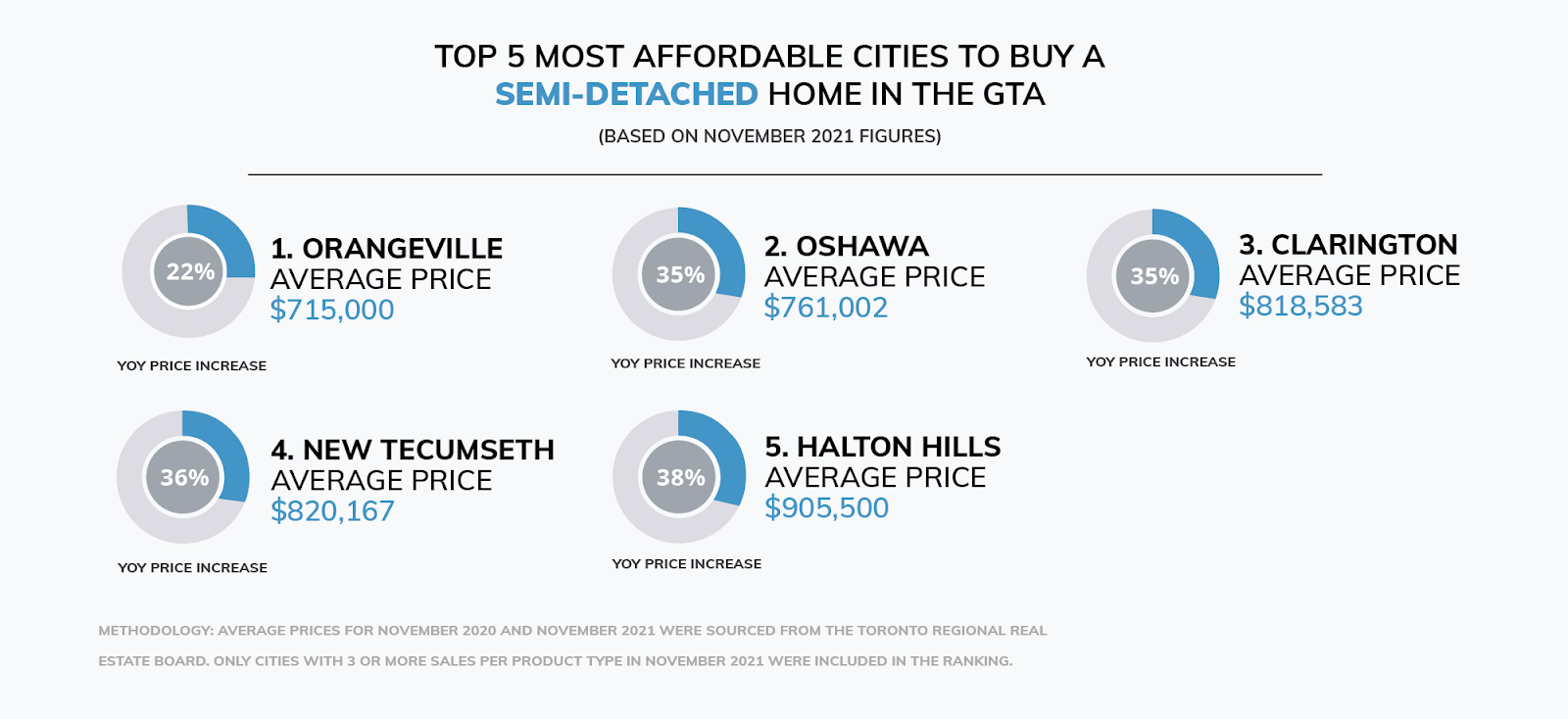

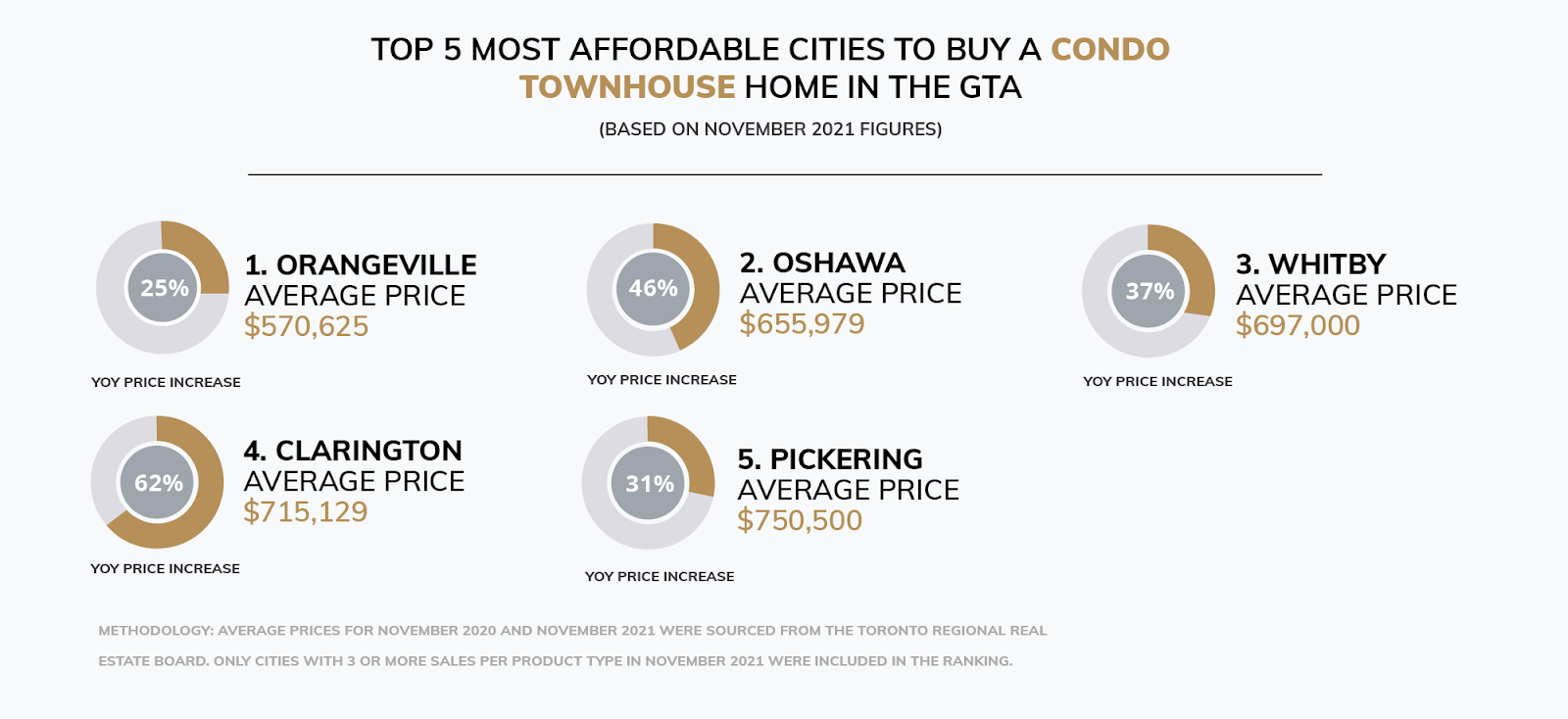

Orangeville is Also the Most Affordable Place to Buy a Condo Townhouse

If things like multiple floors of living space and access to private outdoor space are high on your wishlist, a condo townhouse might be an affordable option for you to consider. Combining the higher-density building form and ownership structure of a condo, these homes are a great blend of space and affordability, especially for young families.

Regardless of your desired city, the average price in the Toronto Region is $826,475 for a condo townhome, which is well below the average price of all home types. When looking for the most affordable cities to choose from, Orangeville comes out on top again with an average price of $570,625 for this type of home.

The rest of our more affordable options come from Durham Region, with the cities of Oshawa, Whitby, Clarington, and Pickering rounding out the remaining spots on the list.

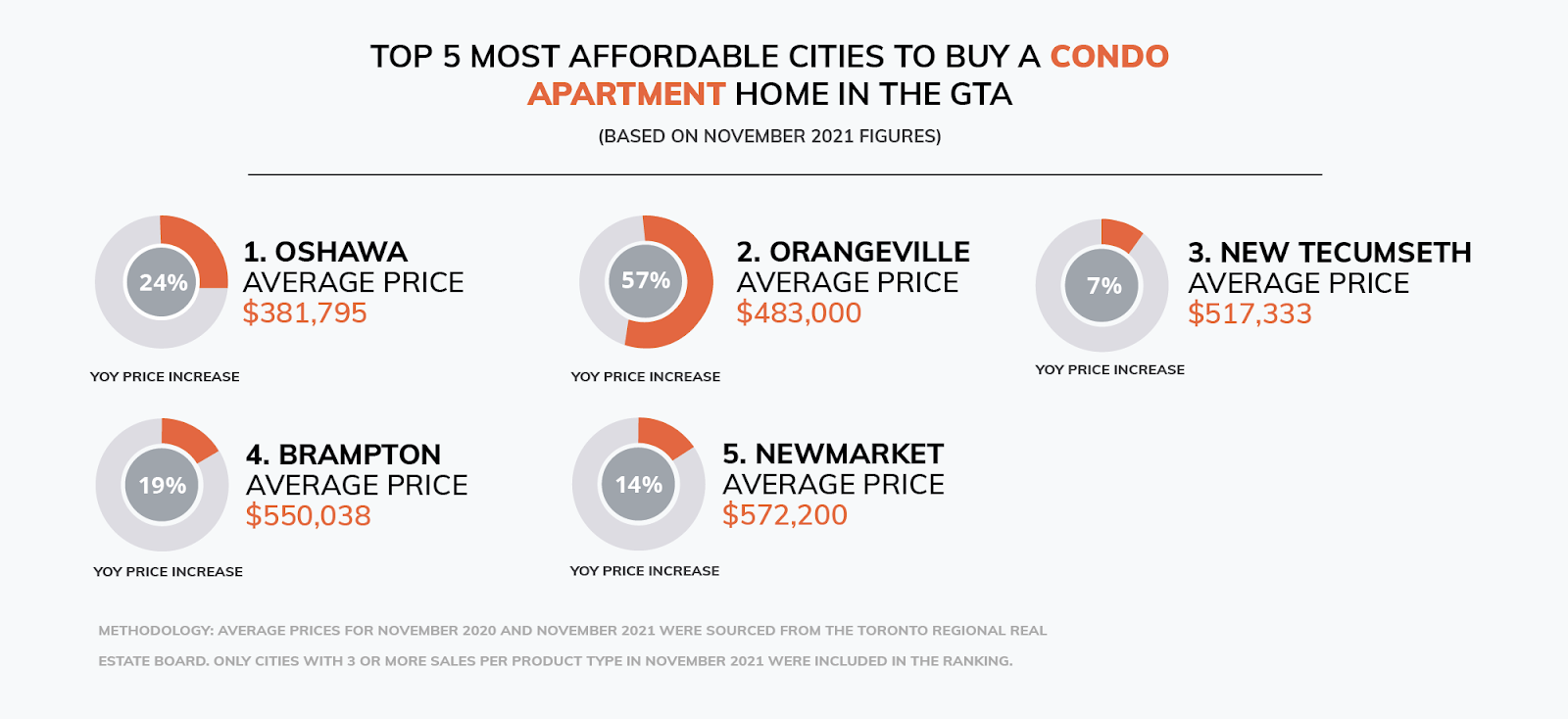

Oshawa is the Most Affordable Place to Buy a Condo Apartment

Condo apartments are one of the most affordable home types on the market in the Toronto Region today, with the average price as of November hitting $711,933 – a rate that comes in at over half the cost of the average detached home.

Within this category, you can find options with average prices under $400,000 if you consider moving to Oshawa, where the average price for a condo apartment was just $381,795 near the end of 2021.

Compared to some of the other cities that topped our list of affordability, Oshawa is considerably larger and more connected. With a population of 170,071 you’ll find more big-city amenities than what’s offered in Orangeville and Brock.

When it comes to your commute, you can make it downtown in 45 minutes by car in good traffic conditions, and taking public transit to work is a viable option with frequent GO Train service.

Other cities that top the list for the most affordable places to buy a condo apartment in the Toronto Region include Orangeville, New Tecumseth, Brampton, and Newmarket

What Do Buyers Need To Know About Moving Further Away From The City Centre?

According to Zoocasa Sales Representative, Allyson Neves, many of today’s buyers understand that being flexible on the location of their home purchase can help them check more boxes off of their wishlist

“Lately when I’m working with buyers, they’re coming to me with their top budget and wishlist for their home then asking me where they’ll need to move to marry the two. It becomes my job to help introduce them to new neighbourhoods or smaller towns that they may not have considered previously” she explains.

When working with buyers with this mindset, Neves starts the process off by understanding the non-negotiables. “It really comes down to knowing your price point first, along with anything else that binds you to a certain general location.”

“Usually buyers will come to me with a general bound for their location. This used to commonly be ‘no more than an hour from the office’. However, with work from home or hybrid options becoming the norm in many industries, I’m more often hearing ‘no more than an hour from my family’, or ‘I’d like to stay north of Toronto’. I compare this request with their budget and talk about which areas would be a fit for what they’re looking for in a property. From there, we start our house hunt. If you’re a buyer with this mindset, it’s helpful to work with an agent who really knows the general area you’d like to purchase in, they’ll be able to introduce you to some of the best places to consider during your search.”

While this report focused on the most affordable locations to purchase in the GTA outside of the city centre, this same mindset can still be applied for buyers looking outside of Toronto too. Neves, who is based out of Barrie explains, “as an agent that specializes outside of the GTA, it’s been a real pleasure introducing buyers who are new to the area to all that outside-of-Toronto living has to offer. Many are excited to trade city living for more space.”

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2