Is the Canadian real estate industry too big to fail? Maybe. It just depends on how you define failure.

While RBC has said that homes sales in Canada could drop as much as 30% this year, they’ve also said they believe there is a “low risk” of a full market collapse. Similarly, RE/MAX has also suggested the odds of the country’s real estate bubble being burst are low.

And now it’s Royal LePage’s turn.

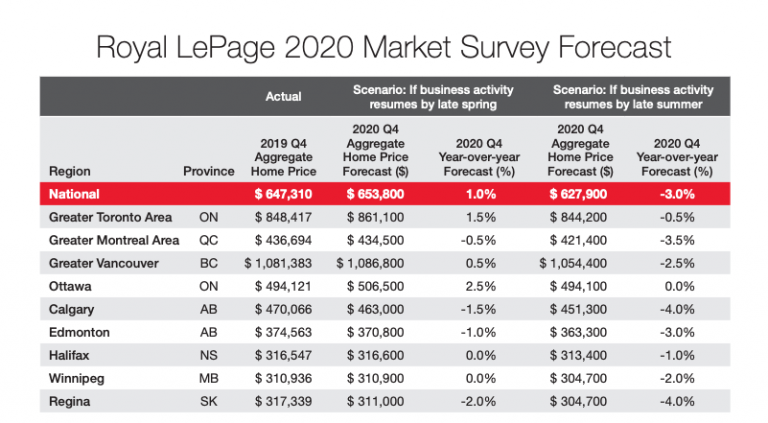

The real estate giant has released both its quarterly Canadian House Price Survey and Market Survey Forecast today, predicting different scenarios depending on the length of the COVID-19 lockdown.

That said, the overall belief from Royal LePage is that “the aggregate price of a home in Canada is expected to remain remarkably stable through the COVID-19 pandemic.”

Just how stable prices remain depends on how long the current states of emergency last throughout the country, and how long the resulting social distancing and stay-at-home restrictions are in place. Not to mention the economic consequences currently being felt by millions of Canadians.

If the measures currently in place across the country are lifted before the end of the second quarter, Royal LePage is forecasting that overall prices for Canadian homes will end 2020 relatively flat, with the aggregate value up 1% year-over-year to $653,800. If, however, COVID-19 restrictions remain in effect throughout the summer, this could drive home prices down by 3% year-over-year to $627,900. Essentially, the average difference between a quick reprieve from current measures and a longer lockdown is about $26,000.

“The impact of COVID-19 on the Canadian economy has been swift and violent, with layoffs driving high levels of unemployment across the country. While is it sad that these people skewed strongly to young and to part-time workers, for the housing industry, the impact of these presumably temporary job losses will be limited as these groups are much less likely to buy and sell real estate,” said Phil Soper, president and CEO, Royal LePage. “From our experience with past recessions and real estate downturns, we are not expecting significant year-over-year price changes in 2020. Home price declines occur when the market experiences sustained low sales volume while inventory builds. Currently, the inventory of homes for sale in this country is very low, matching low sales volumes as people respect government mandates to stay at home.”

In December 2019, Royal LePage had forecast the national aggregate price to increase 3.2% by the end of 2020.

Toronto and GTA

In the GTA, where demand has remained high, the aggregate home price rose 7.5% year-over-year in the first quarter of 2020, arriving at $866,211. Royal LePage broke this down between two-storey homes and bungalows, which saw 7.7% and 3.7% rises to $1,010,004 and $826,186, respectively.

Likewise, the average condo price in the GTA rose 8.8% year-over-year to $580,508 in the first quarter of 2020.

“Toronto real estate appreciated rapidly in the first quarter as the demand that began in the second half of 2019 kept its momentum while inventory remained low. However, by mid-March both buyers and sellers had pulled back to adhere to social distancing measures and gauge the impact of the pandemic on the market,” said Kevin Somers, chief operating officer, Royal LePage Real Estate Services Limited.

Much like the rest of the country, the forecast for Toronto and the GTA depends on how long the current COVID-19 restrictions remain in place. If lifted soon, the GTA could see a 1.5% y-o-y increase in home prices by the end of the year ($861,100). If quarantine remains in place throughout the summer, the GTA could see a decrease of 0.5% y-o-y in aggregate home prices ($844,200). The difference between those two scenarios is $16,900.

Either way, Royal LePage’s market survey suggests the GTA housing market will come out of this pandemic in much better shape than most Canadians.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2