The Bank of Canada finally hit pause on rate hikes in its latest announcement – and its language in the statement suggests its preference is to keep its benchmark rate unchanged for the remainder of the year, according to a prominent economist.

Benjamin Tal (pictured), deputy chief economist at CIBC World Markets, told Canadian Mortgage Professional that the central bank had indicated a willingness to diverge from monetary policy south of the border despite US Federal Reserve chair Jerome Powell’s recent bellicose comments on the likelihood of further hikes.

Tal said a relatively unremarkable statement from the Bank, which contrasted strikingly with its aggressive language in previous rate announcements, showed that it was comfortable taking a different path to the Fed – even if it said it remained open to more rate increases later in the year.

“I think if you give them the choice, they will actually prefer not to continue to raise because they don’t want to overshoot,” he said.

“They are keeping their options open, but at the same time one thing that is interesting [is that] although the Fed is sounding very hawkish, and Powell is talking about another 75 basis points potentially, it seems that the Bank of Canada is not paying attention to the gap between the Fed and [itself].”

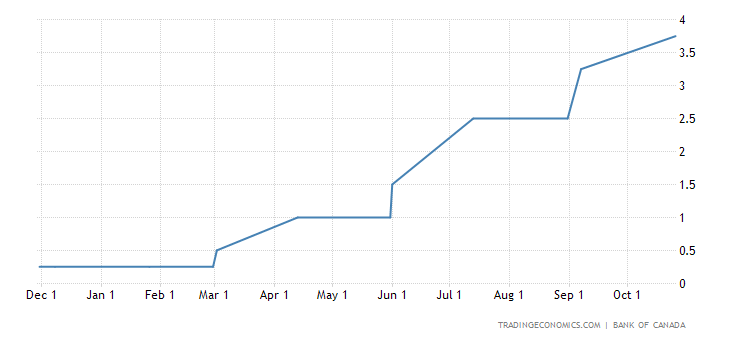

We have maintained our policy interest rate at 4.50%.

What could push the Bank of Canada into further rate hikes in 2023?

One fear could be that the Fed will move so rapidly that it will force the Bank of Canada into action because of the impact that divergence will have on the Canadian dollar, Tal said – although he added that the Canadian central bank had given itself breathing space to assess the landscape before deciding on further action.

Wednesday’s announcement marked the first time in more than 12 months that the Bank has opted to hold fire on rate hikes, with its statement noting that global economic trends had continued to play out as anticipated in January. Global inflation ticked downwards and growth slowed, while in Canada inflation fell to 5.9% in January and the economy remained flat despite resilient employment figures.

Still, while those factors may have helped copper-fasten the decision to keep the trendsetting rate unchanged, plenty could still transpire between now and the end of the year to nudge the Bank in the direction of further increases, according to Tal.

“Although [they] opened the door to another move if necessary, they’re basically telling you that ‘We don’t have data to justify a rate hike at this point,’” he said. “The labour market is still relatively tight, although [they’re] starting to look at some aspects of the inability of companies to pass the cost to the consumer because of the reduction in come.

“So this suggests that they are willing and hoping that they will not need to raise again – but the options are still open.”

What’s next for interest rates in Canada?

The five-year Government of Canada rate could be set for a small decline in the coming months, Tal said, reflecting a possible calming in the market over the Bank of Canada’s future approach, and to some extent the Fed’s.

“Over the next six months, my guess is that we will see a modest decline in the five-year rate while the variable-rate mortgage that is linked to the overnight rate will be stable,” he said. “Let’s hope that they will not go by another 25 basis points – but [that’s] still a risk.”

The Bank’s decision not to raise its policy rate further may “inject a wave of optimism” into the housing market as buyers and developers move off the sidelines, Tal said, although he cautioned that the impact would remain mild for now.

Stability in rates, he said, was “something that will empower people to get into the market and even [allow] developers to start rethinking their plans, and actually go ahead with some plans.

“It’s not going to be a market changer and a gamechanger, but it’s going to be overall, at the margin, a positive development.”

While the Bank by no means shut the door on the prospect of resuming its rate-hiking trajectory further down the road in 2023, Tal said its apparent willingness not to follow closely at the tail of the Fed was a positive development.

“I think that the focus should be to what extent they are paying attention to the Fed. I think that’s very important,” he said. “And at this point, it seems that they’re willing to ignore the Fed – and that’s good news.”

What’s your reaction to the Bank of Canada’s latest interest rate announcement? Let us know in the comments section below.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2