Although the COVID-19 pandemic did not impact the GTA housing market quite as profoundly as some thought it might, the province’s lockdown measures made cities a little less desirable than rural and suburban areas with larger homes and yards, and condo-heavy municipalities such as Toronto suffered a bit more as a result.

In Mississauga, a city comprised of both sprawling subdivisions and modern condo towers, the condo market saw significantly fewer sales than the more in-demand low-rise market.

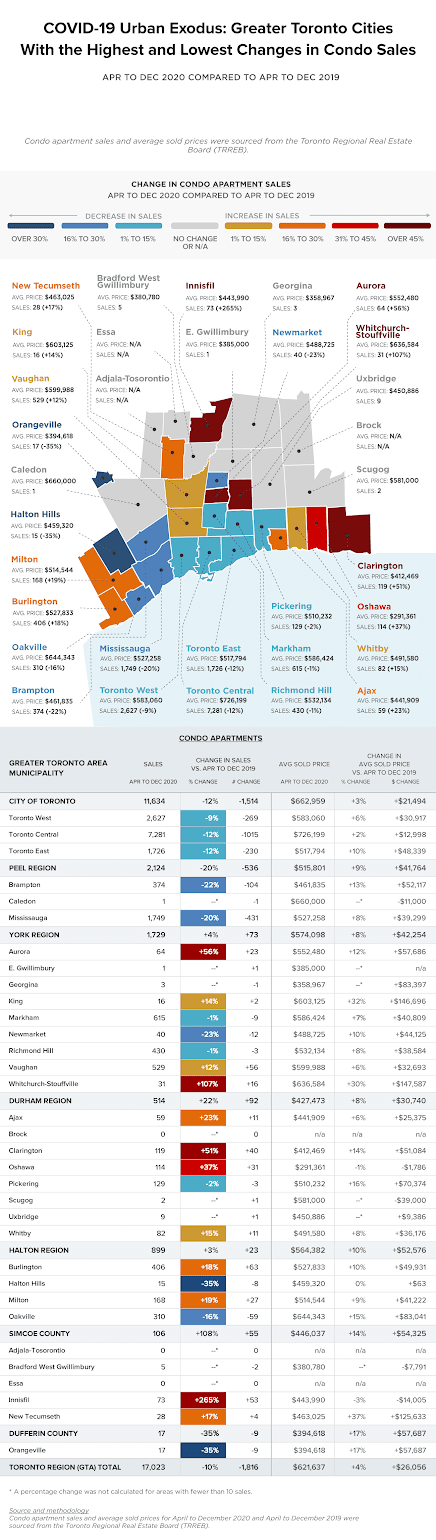

condo apartment sales declined the most sharply in Peel Region (Mississauga, Brampton and Caledon). Sales across the region fell 20 per cent year-over-year between April and December 2020.

The report says that condo sales declined 22 per cent in Brampton and 20 per cent in Mississauga.

That said, condo units are still pricy.

the average price for condo apartments grew 9 per cent to $515,801 in Peel, something the report says could be driven by buyers seeking larger units with more square footage due to pandemic-driven lifestyle shifts. Prices rose 13 per cent in Brampton and 8 per cent in Mississauga.

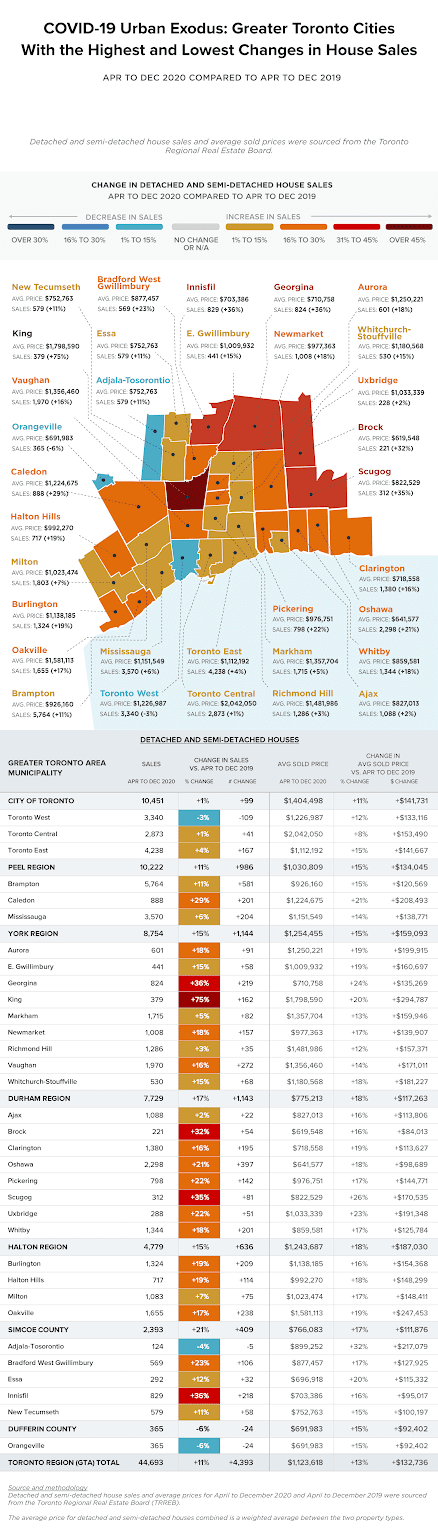

But how did home sales fare overall in Mississauga and other GTA cities? looked at home sales and the average sold price data from the Toronto Regional Real Estate Board (TRREB) for the period between April 2020 and December 2020 to examine how cities were impacted by people opting to abandon urban areas for municipalities with larger homes and more outdoor space.

In Mississauga, low-rise sales climbed 6 per cent and the average sold price hit $1,151,549.

Not unexpectedly, the report found that there was a higher rate of sales and price growth for low-rise homes versus condo apartments in nearly every region. For the GTA as a whole, this translated to an 11 per cent increase in detached and semi-detached house sales and a 10 per cent decrease in condo apartment sales compared to 2019.

The average house price in the GTA rose 13 per cent (or $132,736 to $1,123,618 year-over-year) during this period, and the average condo apartment price rose just 4 per cent (or $26,056, to $621,637).

The report says that “urban flight” did indeed become a factor last year, with municipalities furthest from Toronto seeing the largest jumps in the growth rate of house sales.

According to the report, Simcoe County had the highest increase in house sales among GTA regions, as detached and semi-detached house sales grew 21 per cent year-over-year and 2,393 houses changed hands. The average sold price grew 17 per cent annually to $766,083.

Following Simcoe County was Durham Region, where there were 1,143 more detached and semi-detached house sales between April and December 2020—a 17 per cent increase. The

Other municipalities that saw a big uptick in sales include King (75 per cent increase in house sales and a 20 per cent annual increase in the average home price to $1,798,590), Georgina (36 per cent spike in sales and 24 per cent increase in the average house price to $710,758), and Caledon (29 per cent uptick in sales and 21 per cent climb in price to $1,224,675).

Interestingly enough, condo apartment sales grew in some parts of the GTA. Simcoe County saw a 108 per cent increase in condo apartment sales and a 14 per cent increase in the average sold price for condo apartments. That said, the report found that the total volume of condo apartment sales in the region was relatively low, with just 106 condos being sold.

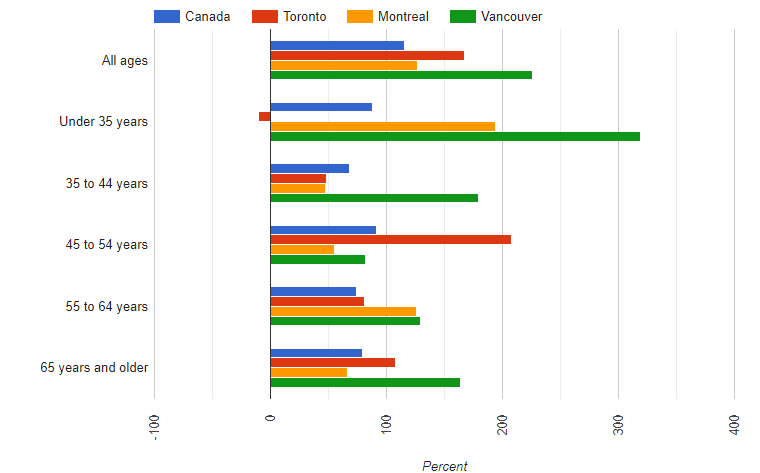

Municipalities with the highest per cent increase in detached and semi-detached house sales, April to Dec 2020, compared to April to Dec 2019

1. King (York Region)

April to Dec 2020 sales: 379 (+75%)

April to Dec 2020 average price: $1,798,590 (+75%)

2. Innisfil (Simcoe County)

April to Dec 2020 sales: 829 (+36%)

April to Dec 2020 average price: $703,386 (+16%)

3. Georgina (York Region)

April to Dec 2020 sales: 824 (+36%)

April to Dec 2020 average price: $710,758 (+24%)

Municipalities with the smallest increase in detached and semi-detached house sales, April to Dec 2020 compared to April to Dec 2019

1. Orangeville (Dufferin County)

April to Dec 2020 sales: 365 (-6%)

April to Dec 2020 average price: $691,983 (+15%)

2. Adjala-Tosorontio (Simcoe County)

April to Dec 2020 sales: 124 (-4%)

April to Dec 2020 average price: $899,252 (+32%)

3. Toronto (West)

April to Dec 2020 sales: 3,340 (-3%)

April to Dec 2020 average price: $1,226,987 (+12%)

Municipalities with the biggest decrease in condo apartment sales, April to Dec 2020, compared to April to Dec 2019

1. Orangeville (Dufferin County)

April to Dec 2020 sales: 17 (-35%)

April to Dec 2020 average price: $394,618 (+17%)

2. Halton Hills (Halton Region)

April to Dec 2020 sales: 15 (-35%)

April to Dec 2020 average price: $459,320 (0%)

3. Newmarket (York Region)

April to Dec 2020 sales: 40 (-23%)

April to Dec 2020 average price: $488,725 (+10%)

Municipalities with the biggest increase in condo apartment sales, April to Dec 2020, compared to April to Dec 2019

1. Innisfil (Simcoe County)

April to Dec 2020 sales: 73 (+265%)

April to Dec 2020 average price: $443,990 (+17%)

2. Whitchurch-Stoufville (York Region)

April to Dec 2020 sales: 31 (+107%)

April to Dec 2020 average price: $636,584 (+30%)

3. Aurora (York Region)

April to Dec 2020 sales: 64 (+56%)

April to Dec 2020 average price: $552,480 (+12%)

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2