Ontario Economic Overview

With 2019 approaching its end, Ontario’s economic growth for 2019, at just over 1%, is forecasted

to underperform the national average of 1.4%, with 2020 only expected to see about 0.75% growth

compared to Canada’s 1.1%. The Greater Toronto Area (GTA) and Ottawa-Gatineau regions are

expected to see stronger growth than the province as a whole, at 1.2% and 1.0%, respectively in

2020. To encourage growth across the nation the BoC is expected to cut the benchmark interest rate

before the end of 2019, followed by a another potential rate cut in early 2020 to provide the necessary

economic stimulus to overcome a slowing global economy. However, headwinds are building, with

slower U.S. expansion and elevated trade policy uncertainty likely to weigh on growth in 2020. The

housing market in Ontario is the silver lining, as this sector weighed on economic growth in 2018

and early 2019, specifically in the GTA, however, it sprung to life in the spring and continues to show

increased in both sales activity and pricing.

Ontario’s labour market remains strong as a healthy influx of immigrants continues to help

companies secure workers amid tight labour market conditions. With the unemployment rate at 5.8%

at the beginning of 2019, employment growth in the province ramped up and by the end of October,

the unemployment rate had decreased to 5.1%. Along with a thriving tech sector in the GTA, Ottawa

and the Kitchener-Waterloo regions, much of the employment growth has occurred in the FIRE

sector, which is once again benefiting from the recovery of the residential real estate market. On the

industrial space-using side, the Transportation and Logistics sector continues to experience steady

growth with the rise of e-commerce services like fulfillment centres and distribution facilities. Ontario

is expected to see employment grow by 2.7% in 2019 and 1.0% in 2020. However, there is a disconnect

between strong job markets and consumer spending. With inflation in Ontario for 2019 expected

to come in at 1.9%, highly indebted households are keeping a tighter grip on their wallets with very

little savings to fall back on. Furthermore, business activity indicators are showing some cracks with

an abatement of U.S. and U.K.-bound exports. The downgraded profile for U.S. GDP and weakness

in the U.K., the two largest Canadian export markets along with elevated political uncertainty could

continue to hamper business investment in Canada and Ontario.

As the Liberals begin their second term on Parliament Hill, the public administration sector is

expected to slow as a result of Federal government spending plans, which will impact Ottawa

specifically, however, the high-tech sector is expected to continue growing, driving demand for space.

Expect much of the federal government’s attention to be on the West coast of Canada, specifically

Alberta, as the Liberals attempt to quell the Wexit movement and appease the Conservatives, while

also attempting to create alliances with the NDP and Bloc.

The continued concerns about high consumer debt and newer concerns about inflationary pressures

being brought on by trade wars could weigh down the performance of commercial real estate.

However, with heavy investment in infrastructure, continued growth in both residential and nonresidential construction and growing labour markets, Ontario is poised for a steady conclusion to 2019

with strong fundamentals throughout 2020.

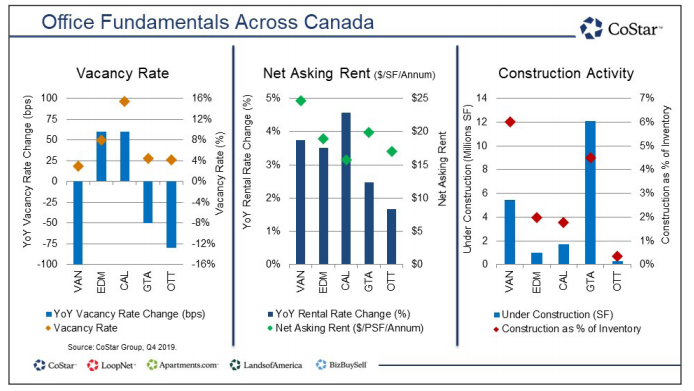

GTA Office Overview

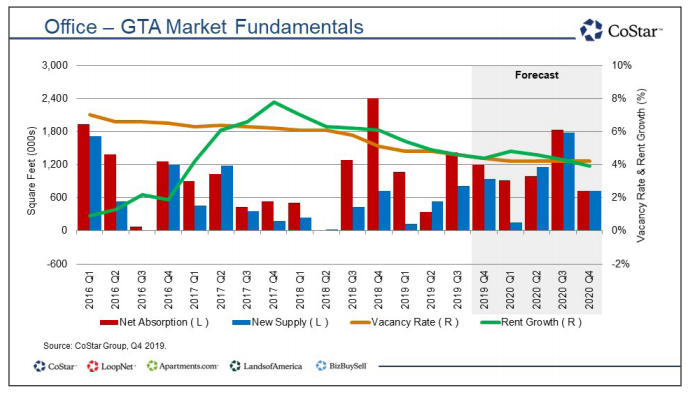

The GTA’s office market had a record year in 2019, while being recognized as one of the strongest

office markets in North America. Deeply entrenched in landlord control, the market saw its overall

market vacancy rate drop 50 bps year-over-year to end 2019 at 4.5%, with the average net asking

rental rate up 2.5% year-over-year to $19.85/SF per annum.

The good news on the supply front is that construction activity continues to increase, with 12.1 million

SF now under construction, representing 4.5% of existing inventory. This includes CIBC Square at

just under 1.6 million SF with CIBC as the lead tenant; the 1.2 million SF office project at 160 Front St.

W., by Cadillac Fairview with the Ontario Teachers’ Pension Plan as the lead tenant; as well as the

879,000 SF project at 16 York St. also developed by Cadillac Fairview with HSBC slated to be the lead

tenant. Furthermore, Oxford Properties continues to market their proposed 1.4 million SF (60-storey)

office tower, The HUB, at 30 Bay St. Along with these projects, Cadillac Fairview’s mixed-use East

Harbour development is planned to be Toronto East’s flagship destination with exceptional transit

connectivity.

With strong demand from finance and technology companies continuing to drive vacancy down,

rental rates are expected to continue increasing, and this new supply will not help alleviate the

tightening market conditions until they start being delivered between 2020 and 2022. As a result,

there are only three blocks of contiguous space 30,000 SF or larger in tech dominated submarkets

such as Downtown West and Liberty Village, and currently only 12 existing properties in the entire GTA

that can accommodate a tenant looking for 100,000 SF or more of contiguous space.

Downtown vacancy remains exceptionally tight as overall vacancy decreased to 2.1%, the lowest

downtown vacancy rate in North America. Landlords are keenly observant of this fact and are

increasingly selective in the types of tenants they are choosing for their space. In light of the strong

fundamentals supporting the Downtown market, landlords are looking for tenants with time-tested

sustainable operations and strong covenants before committing to a lease. While downtown vacancy

is moving down, suburban vacancy also experienced a drop of 190 bps year-over-year and the delta

between downtown and suburban vacancy rates has shrunken to 290 bps from a whopping 470 bps

at this time last year. As a result of the tight downtown market with limited options, tenants will likely

need to pay more attention to the suburban markets if they need a large amount of space in 2020.

The delta between downtown and suburban net asking rental rates is equally impressive. Downtown

rents ended 2019 at $31.71/SF, whereas suburban rents are around $16.31/SF, representing a difference

of $15.40/SF per annum. This is not indicative of the suburbs being in peril, as there remains strong

demand for space in the more urbanized suburban locations, such as Mississauga City Centre,

Vaughan Metropolitan Centre and Downtown Markham. With demand remaining strong, and new

supply limited in the short term, expect rental rates to continue edging up across the city.

The wild card for the GTA office market outlook will be the progression of Google’s Sidewalk Labs

project. The proposed ‘smart city’ development slated for the Port Lands on Toronto’s eastern

waterfront is generating controversy in terms of privacy of personal data, methodology behind

information gathering and how the development will be financed and managed. With 3.3 million SF

of office and retail space, the smart city is the largest attempt to integrate technology with urban

planning in North America. If the project were to get underway to the scope initially unveiled by

Sidewalk Labs, it would immediately impact the office, housing and employment markets. The GTA

receives approximately 100,000 new immigrants (international and domestic) to the area each year,

and the GTA economy is more than capable of providing the skilled talent at the quantity needed for

this project, as well as providing housing for them to live, without the increased demand upending

either the labour or housing markets.

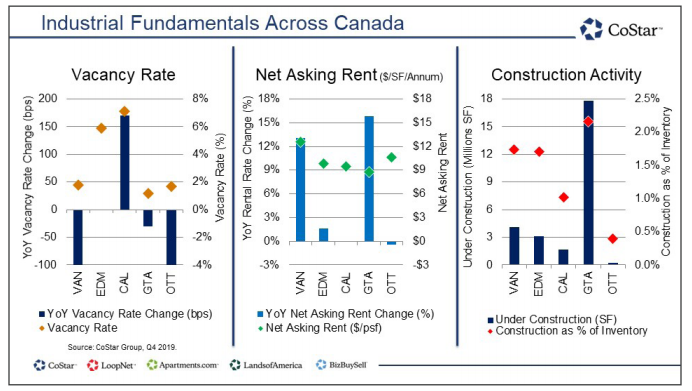

GTA Industrial Overview

Despite the strong rhetoric regarding trade wars and weak retail sales, the GTA industrial market

has experienced continued strong demand. Industrial is the new retail, and much of the industrial

demand in the GTA is primarily driven by transportation, warehousing and logistics tenants, whereas

manufacturing did see a decline in the past year. The high cost of energy is one of the reasons

being cited for the pullback in manufacturing. The PC party pledged to reduce energy costs in their

provincial election campaign last year, however the benefits from lower energy costs will likely not

result in a wholesale return to manufacturing the GTA.

Along with the insatiable demand and limited supply, the GTA is now facing land shortages, which will

impact the velocity and costs of future construction activity. Projections show that the GTA industrial

vacancy rate will continue edging down below 1.0% in 2020, before starting to climb slightly back

above the 1.5% range by 2021. Such incredibly tight conditions will continue to exert upward pressure

on the overall average asking net rental rates, with expectations for rents to reach approximately

$9.45/SF in 2020 and eclipsing $10.00/SF in 2021.

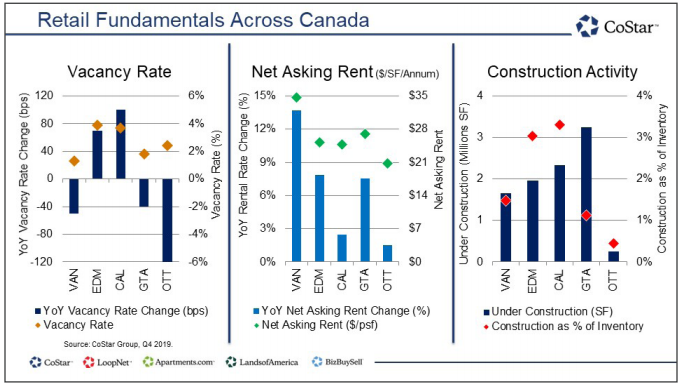

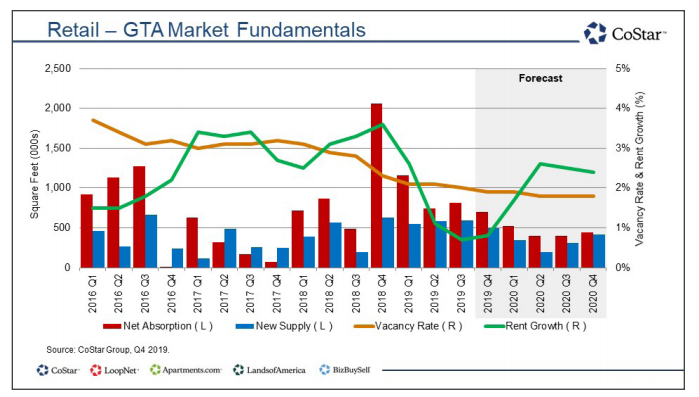

GTA Retail Overview

The GTA retail market continues to receive new international retailers who are either looking to enter the

GTA market, or are using the GTA as a launching pad to the rest of Canada. The newly opened Eataly,

which opened its doors in November at the Manulife Centre in Toronto, is a perfect example of this. The

retail markets vacancy rate edged down 40 bps year-over-year to end 2019 at an impressive 1.8%, with

the average net asking rent up 7.5% over the same period to $26.97/SF per annum. However, market

rent growth has been slightly weaker, reflecting concerns about the retail market in relation to weak

retail sales and retailer performance.

Construction activity has been relatively slow, with only 2.2 million SF of new supply delivered since

Q3 2017, and construction activity has moved down from 3.7 million SF last year to 3.2 million SF at

year-end 2019, representing only 1.1% of existing inventory, with much of this construction activity

being part of mixed-use projects, or expansions to existing malls. Despite the new vacant space that

came to the market as a result of Sears Canada closing in Q1 2018, the limited amount of new supply

has not been enough to satisfy the demand from tenants who are struggling to find space amid low

vacancy and increasing rents. However, with recently announced store closures, and street front and

even mall vacancies creeping back onto the market, expect vacancy rates to rise over the coming

year to end 2020 at 2.4%.

Despite the impressive fundamentals, the economic forecast could prove detrimental to the

retail landscape. The latest national GDP data indicates that retail activity has come off the boil.

Furthermore, retail sales have been showing weakness for some time, with much of the total increase

in retail sales has been the result of inflation and population growth. Although retail sales growth

is expected to remain positive, high consumer debt is expected to hinder retail sales going forward,

despite any expectations for the BoC to cut interest rates. However, GTA retail sales are expected to

increase by over 2.0% each year out to at least 2025, but much of that growth will be captured by

e-commerce as opposed to brick and mortar retail.

In order to combat the effects of e-commerce on the retail market, landlords of premier quality

properties continue to work on improving their properties, making them experiential destinations.

The making of an experiential destination goes beyond just having more restaurants and services

in malls, and can include ventures such as Ivanhoe Cambridge and Cirque du Soleil teaming up to

offer family entertainment centres in shopping centres, which is due to launch early 2020. Landlords

are looking at ways to further differentiate themselves from the rest of the pack in order to attract

more shoppers as well as new and better retailers. Expect to see this, along with more intensification

of retail properties and repurposing of parking lots in suburban malls, as seen at properties such as

Yorkdale Mall, and Aoyuan’s redevelopment plans for Newtonbrook Plaza.

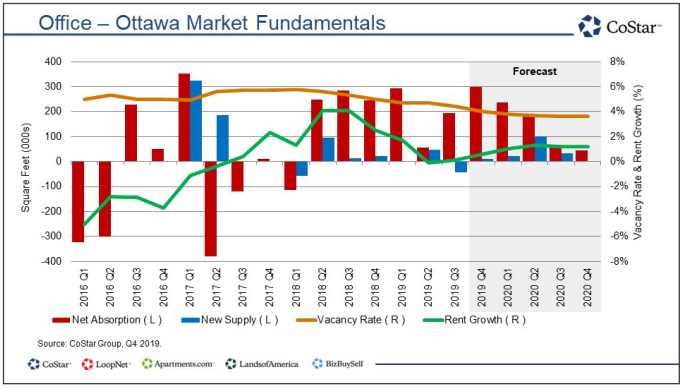

Ottawa Office Overview

Ottawa commercial real estate is experiencing a renaissance with renewed interest along the LRT

line and other well-located properties for the purpose of redevelopment or development. Occupancy

gains were attributed to leasing by technology and federal government tenants throughout 2019

with the now fully operational phase 1 of the LRT line acting as the biggest demand driver. The LRT

has made well-positioned buildings winners in the office market, particularly properties that have

stops integrated into their buildings. The LRT’s completion will secure higher rental rates in buildings in

close proximity and become a main feature in retaining old tenants and attracting new ones. Easier

accessibility outside of the Downtown Core could also continue lowering vacancy rates in both the

western and eastern submarkets. Furthermore, with federal spending likely to curb due to the election

outcome, government leasing is likely to slow down; however, this will allow private sector tenants to

either expand or move into the market with less competition.

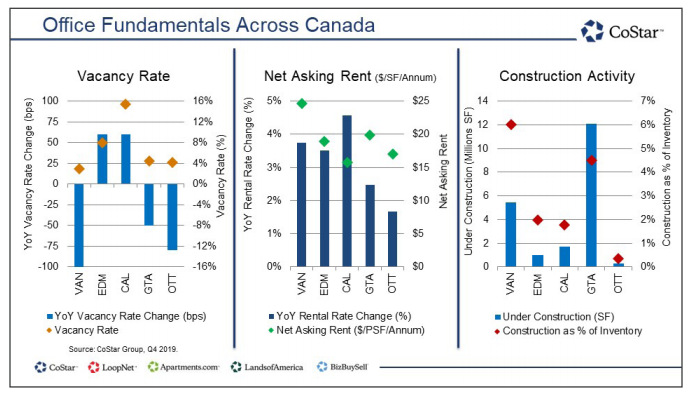

Overall vacancy in Ottawa is down 80 bps year-over-year to end 2019 at 4.2%; however, net asking

rents were up only 1.7% over the same period, to $16.98/SF/annum. Construction activity has been

underwhelming over the past years but a handful of projects should begin to change the narrative

across the city. Of the projects that are under construction, most are larger mixed-use projects,

with only a portion slated to be office space. The largest example of this being the waterfront

development Zibi, expected to bring approximately 240,000 SF of office space to the market. Close

behind is 900 Albert St., a mixed-use and transit oriented development comprised of 200,000 SF of

office space. Like many of these projects, 900 Albert St. is located along the new LRT Line. However,

other projects, such as Taggart’s 153,000 SF design build in the Kanata West business Park for Kinaxis,

a supply chain planning software company, should kick off shortly.

Although high-tech companies and the Federal government have long been part of the office market

tenant mix in Ottawa, the Federal government is beginning to embrace the concept of flexible work

space and choosing to occupy more space in the suburban markets over the last few years, which

has resulted in higher vacancy downtown. This has created opportunities for high-tech tenants who

might be looking for more urban locations with access to public transit. Expect demand to outstrip

supply in 2020 and beyond, with vacancy continuing to edge down.

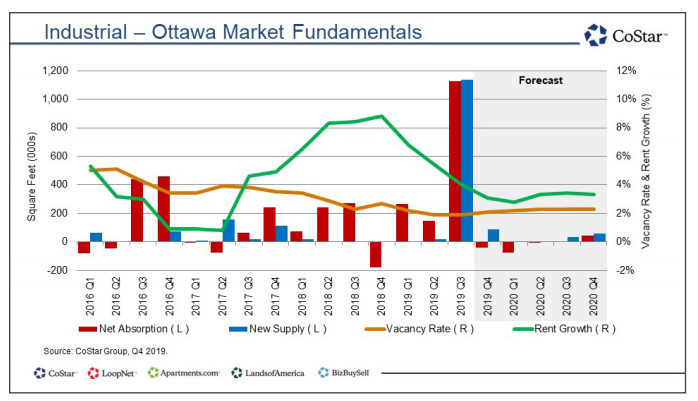

Ottawa Industrial Overview

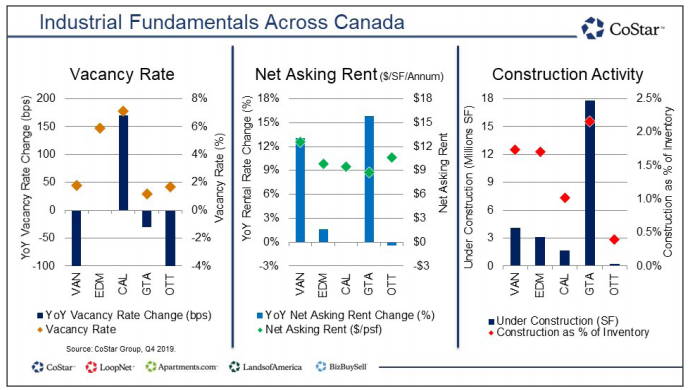

The Ottawa industrial market has experienced relatively strong demand throughout 2019, with

vacancy down 100 bps to end 2019 at 1.7%. As a result of tightening market conditions market rents

continue to increase, despite asking net rental rates appearing flat year-over-year at $10.63/SF per

annum at the end of 2019. This continues to raise the question of whether tenants are willing to wait

for new space or pay record high rental rates for existing older stock.

Although the market experienced significant new supply in 2019, 1.0 million SF of the 1.2 million SF

delivered in 2019 was the result of the new Amazon fulfilment centre, resulting in no real alleviation to

continuously tightening conditions. Both the developer and the City of Ottawa hope that this project

will breathe new life to the city’s industrial development pipeline and kick off more new speculative

construction in the region.

Looking forward, there is currently only one major project to speak of that could satiate demand

from new or expanding tenants in the Ottawa market. Broccolini’s proposed 700,000 SF speculative

development is interesting not only because of its size, but also because they have applied to the

City to raise the height of the building from just under 50 feet to almost 100 ft. The question is, what

would you do with a 100-foot tall single storey industrial building? Despite this potential project,

the lack of new supply and availability of quality space, in particular large blocks, will contribute to

continued tight market conditions and higher asking rental rates.

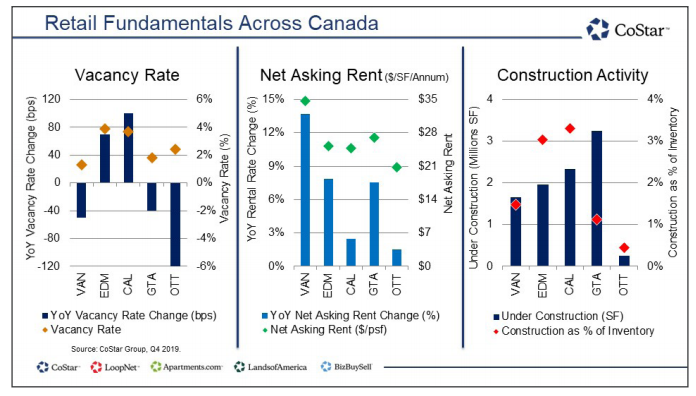

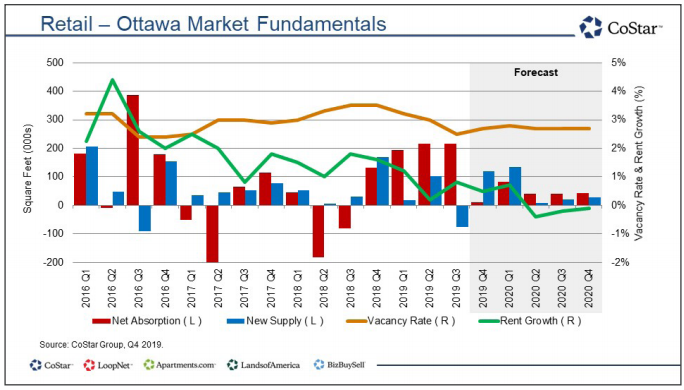

Ottawa Retail Overview

The Ottawa retail market has experienced a 120 bps year-over-year drop in vacancy to 2.7% at the

end of 2019. This drop is partially the result of retailers opening new locations at the Cadillac Fairview

Rideau Centre earlier this year and the slow rollout of legal cannabis brick-and-mortar stores. As a

result, average net asking rental rates have steadily increased, however, they are only up 1.5% yearover-year to end 2019 at $20.96/SF per annum.

Construction activity has been relatively slow as well with only 534,000 SF of new supply delivered

since Q2 2017 and only another 252,000 SF currently under construction, mainly as part of the

podiums of mixed-use residential projects along the new LRT lines. Given the forecast of demand for

space along the LRT lines, this construction activity will likely not meet demand over the coming years,

and redevelopment of the areas adjacent to the new transit line seems likely.

Ottawa’s retail sales growth is expected to remain strong in 2020, at 2.1% growth, however, as the

potential for pullbacks in the public administration sector weigh on the outlook, retail sales growth

is expected to fall below 2.0% for the foreseeable future thereafter. Furthermore, high debt service

costs and competition from the rise of e-commerce, especially now that Amazon is in town, will take

a bite out of retail sales activity. Developers will look to give buildings in close proximity to the LRT a

facelift while retailers in older buildings, in less than ideal locations, may have to close their doors due

to increased costs and lackluster sales growth. The upside of this shift would be new and fresh retail

space available upon completion, leading to continued interest from diversified international retailers.

Landlords continue to look for ways to differentiate their properties and make them more experiential

destinations in order to combat the effects of e-commerce on the retail market, and the Ottawa

market has not been immune to this. Expect to see more intensification of retail properties and

repurposing of parking lots, specifically along the LRT lines in the coming years.

Source: CoStar

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2