Ontario’s Fair Housing Plan introduces a comprehensive package of measures to help more people find affordable homes, increase supply, protect buyers and renters and bring stability to the real estate market. The plan includes:

Actions to Address Demand for Housing:

Introducing legislation that would, if passed, implement a new 15-per-cent Non-Resident Speculation Tax (NRST) on the price of homes in the Greater Golden Horseshoe (GGH) purchased by individuals who are not citizens or permanent residents of Canada or by foreign corporations. Ontario’s economy benefits enormously from newcomers who decide to make the province home. The NRST would help to address unsustainable demand in this region and make housing more available and affordable, while ensuring Ontario continues to be a place that welcomes all new residents. The proposed tax would apply to transfers of land that contain at least one and not more than six single family residences. “Single family residences” include, for example, detached and semi-detached homes, townhomes and condominiums. The NRST would not apply to transfers of other types of land including multi-residential rental apartment buildings, agricultural land or commercial/industrial land. The NRST would be effective as of April 21, 2017, upon the enactment of the amending legislation.

Refugees and nominees under the Ontario Immigrant Nominee Program would not be subject to the NRST. Subject to eligibility requirements, a rebate would be available for those who subsequently attain citizenship or permanent resident status as a well as foreign nationals working in Ontario and international students. See technical bulletin for further information.

Actions to Protect Renters

Expanding rent control to all private rental units in Ontario, including those built after 1991. This will ensure increases in rental costs can only rise at the rate posted in the annual provincial rent increase guideline. Over the past ten years, the annual rent increase guideline has averaged two per cent. The increase is capped at a maximum of 2.5 per cent. Under these changes, landlords would still be able to apply vacancy decontrol and seek above guideline increases where permitted. Legislation will be introduced that, if passed, will enact this change effective April 20.

The government will introduce legislation that would, if passed, strengthen the Residential Tenancies Act to further protect tenants and ensure predictability for landlords. This will include developing a standard lease with explanatory information available in multiple languages, tightening provisions for “landlord’s own use” evictions, and ensuring that tenants are adequately compensated if asked to vacate under this rule; prohibiting above-guideline increases where elevator work orders have not been completed; and making technical changes at the Landlord-Tenant Board to make the process fairer and easier for renters and landlords. These changes would apply to the entire province.

Actions to Increase Housing Supply

Establishing a program to leverage the value of surplus provincial land assets across the province to develop a mix of market housing and new, permanent, sustainable and affordable housing supply. Potential sites under consideration for a pilot project include the West Don Lands, 27 Grosvenor/26 Grenville Streets in Toronto, and other sites in the province. This builds on an agreement reached previously with the City of Toronto to ensure a minimum of 20 per cent of residential units within the West Don Lands are available for affordable rental, with an additional 5 per cent of units for affordable ownership.

Introducing legislation that would, if passed, empower the City of Toronto, and potentially other interested municipalities, to introduce a vacant homes property tax to encourage property owners to sell unoccupied units or rent them out, to address concerns about residential units potentially being left vacant by speculators.

Ensuring that property tax for new multi-residential apartment buildings is charged at a similar rate as other residential properties. This will encourage developers to build more new purpose-built rental housing and will apply to the entire province.

Introducing a targeted $125-million, five-year program to further encourage the construction of new rental apartment buildings by rebating a portion of development charges. Working with municipalities, the government would target projects in those communities that are most in need of new purpose-built rental housing.

Providing municipalities with the flexibility to use property tax tools to help unlock development opportunities. For example, municipalities could be permitted to impose a higher tax on vacant land that has been approved for new housing.

Creating a new Housing Supply Team with dedicated provincial employees to identify barriers to specific housing development projects and work with developers and municipalities to find solutions. As well, a multi-ministry working group will be established to work with the development industry and municipalities to identify opportunities to streamline the development approvals process.

Other Actions to Protect Homebuyers and Increase Information Sharing

The province will work to understand and tackle practices that may be contributing to tax avoidance and excessive speculation in the housing market such as “paper flipping,” a practice that includes entering into a contractual agreement to buy a residential unit and assigning it to another person prior to closing.

Working with the real estate profession and consumers, the province is committing to review the rules real estate agents are required to follow to ensure that consumers are fairly represented in real estate transactions. This includes practices such as double ending. The government will modernize its rules, strengthen professionalism and improve the home-buying experience with a goal to make Ontario a leader in real estate standards.

Establishing a housing advisory group which will meet quarterly to provide the government with ongoing advice about the state of the housing market and discuss the impact of the measures in the Fair Housing Plan and any additional steps that are needed. The group will have a diverse range of expertise, including economists, academics, developers, community groups and the real estate sector.

Educating consumers on their rights, particularly on the issue of one real estate professional representing more than one party in a real estate transaction.

Partnering with the Canada Revenue Agency to explore more comprehensive reporting requirements so that correct federal and provincial taxes, including income and sales taxes, are paid on purchases and sales of real estate in Ontario.

Making elevators in Ontario buildings more reliable by establishing timelines for elevator repair in consultation with the sector and the Technical Standards & Safety Authority (TSSA).

Working with municipalities to better reflect the needs of a growing Greater Golden Horseshoe through an updated Growth Plan. New provisions will include requiring that municipalities consider the appropriate range of unit sizes in higher density residential buildings to accommodate a diverse range of household sizes and incomes. This will help support the goals of creating complete communities that are vibrant, transit-supportive and economically competitive, while doing more to address climate change, protect the region’s natural heritage and prevent the loss of irreplaceable farmland. As part of the implementation of the Growth Plan for the Greater Golden Horseshoe, 2006, enough land was set aside in municipal official plans to accommodate forecasted growth to at least 2031. Based on discussions with municipalities across the region, the government is confident that there is enough serviced land to meet the Provincial Policy Statement requirement for a three year supply of residential units. The Greenbelt provides important protection of natural heritage and farmland, and neither the area of the Greenbelt or the rules about what can occur inside of it will be weakened. The upcoming Growth Plan will promote intensification around existing and planned transit stations and will promote higher densities in the suburbs to support transit.

See map “Greater Golden Horseshoe”.

Actions to Date

The government has taken a number of actions over recent months and years in order to support homebuyers, increase supply of affordable and rental housing and promote fairness. These include:

Helping more people purchase their first home by doubling the maximum Land Transfer Tax refund for eligible first-time homebuyers to $4,000. This means eligible homebuyers in Ontario pay no Land Transfer Tax on the first $368,000 of the cost of their first home.

Modernizing the Land Transfer Tax to reflect the current real estate market, including increasing rates on one or two single-family residence over $2 million. Revenue generated from the increased rates is being used to fund the enhancements to the First-Time Homebuyers Refund.

Making it easier for not-for-profit affordable housing providers to buy surplus government lands.

Introducing an inclusionary zoning framework for municipalities that will enable affordable housing units as part of residential developments.

Amending the Planning Act and the Development Charges Act to support second units, allowing homeowners to create rental units in their primary residence and creating additional supply.

Freezing the municipal property tax burden for multi-residential apartment buildings in communities where these taxes are high.

Collecting information about Ontario’s real estate market to support evidence-based policy development

Appendix: Data and Trends on the Real Estate Market

Ontario’s housing market has seen very dynamic growth in recent years, with prices in the Greater Toronto Area and the Greater Golden Horseshoe rising significantly. This has been supported by economic fundamentals, including a growing population, rising employment, higher incomes and very low borrowing costs.

House prices have been rising at a robust pace in the Greater Toronto Area since the end of the 2008-09 recession.

After two consecutive years of double-digit gains, average house prices in the Toronto region reached $916,567 in March 2017, up 33.2 per cent from a year earlier.

See image “Toronto Home Resale Prices”

The Greater Toronto Area showed the sharpest rise in home prices in Ontario over the past two years.

While the growth rate of prices of homes in the Greater Vancouver Area have been slowing since August 2016 after the introduction of B.C.’s foreign-buyers tax, home prices have been climbing steadily in the Greater Toronto Area.

See image “MLS Home Price Index”, “Greater Toronto Area Price Increases Outstrip Other Cities” and “Housing supply in Ontario seems to be aligning with demographics”.

According to Urbanation, the average rent per square foot for new leases in the Greater Toronto Area condo market rose 11 per cent in the last quarter of 2016 compared to a year earlier, the fastest pace of growth since at least 2011.

See image “% change, year-over-year, GTA”.

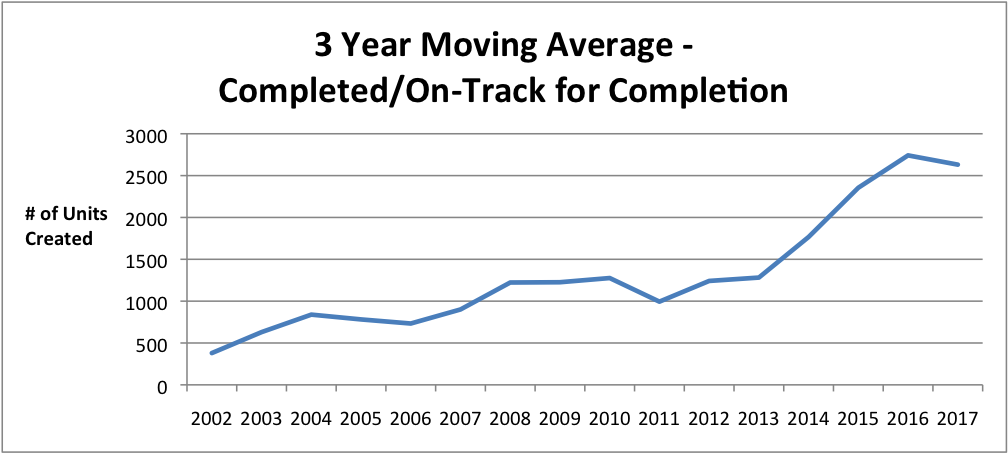

The number of owners with more than one residential property has been rising steadily since 2000.

See image “Number of Owners With More Than One Residential Property in the GTHA: 2000-16”.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2