It won’t happen overnight, but with Toronto condo sales clearly on the rebound, struggling condo prices could soon be following them upward before the end of the year.

That’s the message from RBC Senior Economist Robert Hogue who, earlier this month, wrote that the Toronto condo market’s “relative affordability” may be boosting its appeal to homebuyers. This edge in affordability over single-family homes likely contributed to condo sales across the region rising over 85 percent in January.

“[T]he growing affordability advantage over single-family homes and the start of vaccination distribution (interpreted by some investors as a sign downtown condos will soon regain popularity) have rekindled buyers’ interest in condos over the past couple of months,” he wrote.

Hogue added that the ample condo inventory currently on the market is keeping prices stagnant for now, but sales activity picked up in December and continued to climb in January, suggesting condo prices could begin to “heat up” later this year.

While the ongoing surge in condo sales bodes well for prices seeing a lift before 2021 ends, the recovery has some headwinds to contend with before it can really take off.

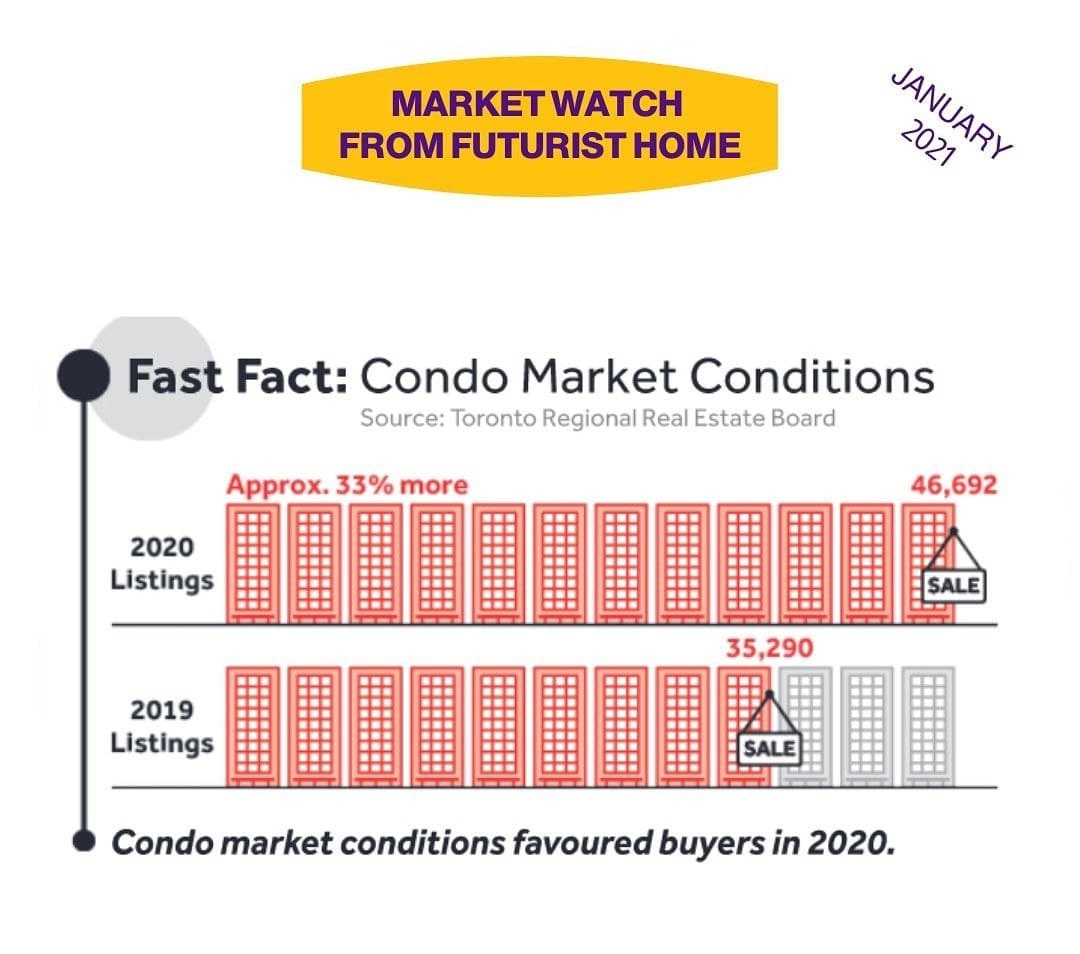

First, condo listings are still hitting the market at a rapid pace. Hogue acknowledged that active condo listings in Toronto rose by 85 percent in January, keeping “upward price pressure at bay for now.” That said, this is down from the staggering 177 percent annual increase in active condo listings recorded in November.

The Toronto Regional Real Estate Board (TRREB) forecast last month that the rate at which new condo listings are hitting the market would continue to decelerate into 2021’s second half, leaving room for strong buyer demand to push prices up.

But this begs an important question on condo demand: can it stay strong as Toronto’s rental market continues to see elevated supply and declining prices? Realosophy Realty President John Pasalis believes the outlook for the condo market hinges on how the rental market fares in the coming months.

Investors were partly responsible for the surge in condo buying seen in December and January, motivated by lower prices and a belief that rebounds in both the rental and resale condo markets were on the horizon in 2021.

This is by no means a sure bet.

“[I]f the rental market continues to soften, I suspect this may push investors back to the sidelines,” Pasalis said.

One of the big stories from fall 2020 that buoyed hopes for the Toronto condo market’s fortunes this year was the federal government initiative to boost immigration rates between 2021 and 2023. The plan is to welcome an additional 50,000 newcomers each year on top of existing immigration targets to make up for the massive disruption that played out in 2020.

New research from RBC Senior Economist Andrew Agopsowicz indicates the federal government is likely to fall short of this target, with an estimated 275,000 new permanent residents forecast to be welcomed to the country by the end of the year, far behind the 401,000 target.

With immigration being a key driver of population growth for the Toronto region, another shortfall in 2021 certainly won’t benefit the condo and rental markets.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2