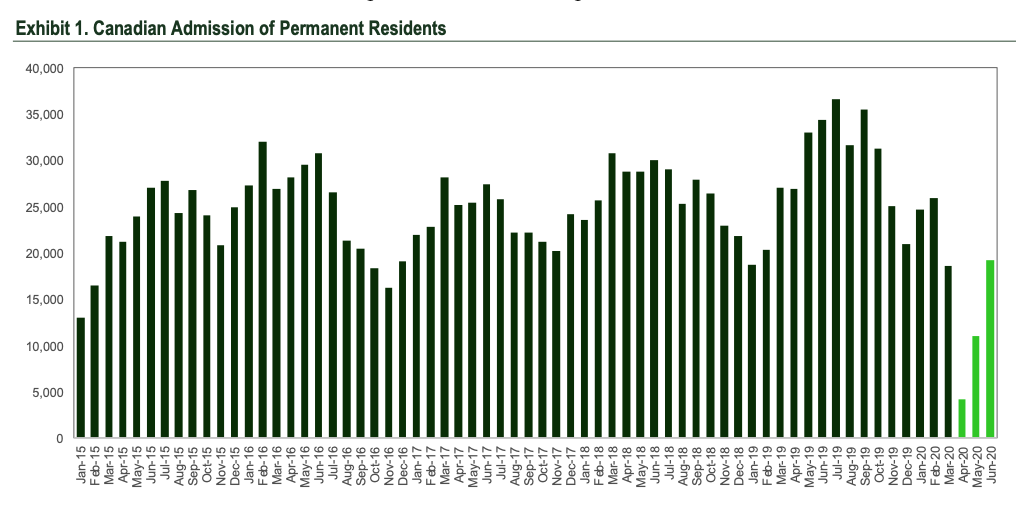

Population growth — so, immigration — is a crucial demand driver for the real estate industry, and for the growth of the overall Canadian economy. Last year, Canadian immigration averaged about 28,400 people per month, according to a recent equity research report (on the apartment sector) by TD Bank. The total number for 2019 was 341,175 people.

Not surprisingly, this number fell off in March of this year with the closing of our borders. In March, immigration declined to 18,560 per month and bottomed out in April with only 4,135 immigrants being admitted to the country. This has no doubt been a factor in some of the rent softening that we have seen in the multi-family space.

While it’s unlikely that Canada will meet its 2020 target of 320,000 to 370,000 new immigrants, it’s important to note that we have seen a fairly swift recovery (see above). In June of this year, the number rebounded to 19,175 new immigrants. And I’m certain that most of this cohort still went straight toward our biggest cities.

It’s also important to keep in mind that Canada’s three-year goal (2020-2022) remains 1 million new immigrants. TD is of the opinion that this target is still attainable, as this “short-term immigration headwind” is likely to flip into a tailwind once our borders become more porous and we get to the other side of this pandemic.

I think it’s pretty safe to say that you could bucket this immigration blip into (1) short-term dislocation. It is not a (3) long-term structural change. Canada remains one of the greatest countries in the world. We will continue to attract smart and ambitious people from all around the world, and most will want to settle in our urban centers.

All of this, of course, will be good for the real estate industry and will be vital to the strength of the Canadian economy as a whole.

Chart: TD Securities

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2