The First-Time Home Buyer Incentive (the Incentive) helps qualified first-time homebuyers reduce their monthly mortgage carrying costs without adding to their financial burdens.

You need to have the minimum down payment to be eligible. You can then apply for a 5% or 10% shared equity mortgage with the Government of Canada. Your maximum qualifying income is no more than $120,000 and your total borrowing is limited to 4 times the qualifying income.

The Incentive has an equity-like payout, where the government would share in the upside and downside of the property value.

The First-Time Home Buyer Incentive launches September 2, 2019*.

* Barring any unforeseen circumstances the program will launch on September 2, 2019. The first closing will take effect on November 1, 2019.

Program Details

How does it work?

The Incentive enables first-time homebuyers to reduce their monthly mortgage payment without increasing their down payment. The Incentive is not interest bearing and does not require ongoing repayments.

Through the First-Time Home Buyer Incentive, the Government of Canada will offer:

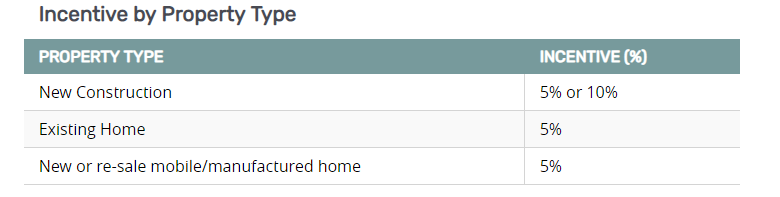

-5% of a first-time buyer’s down payment for the purchase of a re-sale home

-5% or 10% of a first-time buyer’s down payment for the purchase of a new construction

How do I know how much I have to pay back?

You can repay the Incentive at any time without a pre-payment penalty. You have to repay the Incentive after 25 years or if the property is sold. The repayment of the Incentive is based on the property’s fair market value:

- You receive a 5% incentive of the home’s purchase price of $200,000, or $10,000. If your home value increases to $300,000 your payback would be 5% of the current value or $15,000.

- You receive a 10% incentive of the home’s purchase price of $200,000, or $20,000 and your home value decreases to $150,000, your repayment value will be 10% of the current value or $15,000.

NOTE: If your property value goes down, you are still responsible for repaying the shared equity mortgage based on the current home value at time of repayment.

Funding Available

The First-Time Home Buyer Incentive works on a first-come-first-serve basis. The total amount of funding will be $1.25 billion over 3 years.

Eligibility & Requirements

Who can apply?

- Canadian citizens, permanent residents, and non-permanent residents who are legally authorized to work in Canada

- Borrowers must have a maximum qualifying income of $120,000

-Total qualifying income cannot exceed $120,000 per year

-This is subject to qualifying income requirements set out by lenders and mortgage loan insurers - At least one borrower must be a first-time homebuyer, as per the definition below.

Are you a first-time homebuyer?

You are considered a first-time homebuyer if you meet one of following qualifications:

- you have never purchased a home before

- you have gone through a breakdown of a marriage or common-law partnership (even if you don’t meet the other first-time home buyer requirements).

- in the last 4 years, you did not occupy a home that you or you current spouse or common-law partner owned

- IMPORTANT: With the 4-year clause, it is possible that you or your spouse or common-law partner qualifies for the first-time homebuyer incentive (if you are in a married or common-law relationship). Even if you or your spouse or common-law partner has previously owned a home in the last 4 years.

How does the 4-year period work?

- The 4-year period begins on January 1 of the fourth year before the year you purchased your home. It ends 31 days before the date you purchase your new home. Here are a few examples:

-if you purchase a home on March 31, 2015, the 4-year period begins on January 1, 2015 and ends on February 28, 2019

-if you sold your home you lived in in 2013, you may be able to participate in 2018 or if you sold the home in 2014, you may be able to participate in 2019

Are there other mortgage details?

- Total borrowing is limited to 4 times the qualifying income. The combined mortgage and Incentive amount cannot exceed four times the total qualifying income.

- The amount for the mortgage loan insurance premium is excluded from this calculation.

- The Incentive will be a second mortgage on the title of the property. There will be no regular principal payments, it’s not interest bearing and has a maximum term of 25 years.

- The Incentive will have an equity-like payout, where the Government of Canada will share in the upside and downside of the property value upon repayment.

Is Mortgage Loan Insurance required?

- Mortgages must be eligible for mortgage loan insurance. The first mortgage must be greater than 80% of the value of the property. This is subject to a mortgage loan insurance premium based upon the amount of the first mortgage.

- Mortgage loan insurance premiums may be subject to provincial taxes.

What are the down payment requirements?

- Minimum down payment is 5% of the first $500,000 of the lending value. It is 10% of the lending value above $500,000 from traditional down payment sources.

- Traditional down payment comes from the borrower’s own resources and may include:

-savings

-withdrawal/collapse of a registered retirement savings plan (RRSP)

-non-repayable financial gift from a relative

–Note: Unsecured personal loans or unsecured lines of credit used to satisfy minimum down payment requirements are not eligible for the program.

What properties are eligible?

- The Incentive is to help first-time homebuyers purchase their first home. Eligible properties include:

- 1 to 4 unit residential properties which includes

-new construction

-re-sale home

-new and re-sale mobile/manufactured homes

- The property must be located in Canada and must be suitable and available for full-time, year-round occupancy.

What are the terms of repayment?

- The first-time homebuyer will be required to repay the Incentive amount after 25 years or when the property is sold, whichever comes first. The homebuyer can also choose to repay the Incentive in full at any time, without a pre-payment penalty.

How is repayment calculated?

- If a homebuyer receives a 5% (or 10%) Incentive, he would repay 5% (or 10%) of the home’s value at repayment.

- Repayment is based on the property’s fair market value.

Let’s look at a specific situation

Anita wants to buy a new home for $400,000.

Under the First-Time Home Buyer Incentive, Anita can apply to receive $40,000 in a shared equity mortgage (10% of the cost of a new home) through the program. This is on top of the minimum required down payment of $20,000 (5% of the purchase price) from her savings.

This lowers the amount she needs to borrow and reduces her monthly expenses.

As a result, Anita’s mortgage is $228 less a month or $2,736 a year.

* This example is for illustrative purposes only. Anita will need to repay the incentive at 10% of the fair market value when she sells the property or after 25 years, whichever is earliest.

Here’s another situation

John has an annual qualifying income of $83,125.

To be eligible for Canada’s First-Time Home Buyer Incentive, he can purchase a home up to $350,000. John still has the required minimum down payment of 5% of the purchase price, $17,500 from his savings. He can receive $35,000 in a shared equity mortage — 10% of a newly constructed home.

This would reduce John’s mortgage payments by $200 a month or $2,401 a year.

* This example is for illustrative purposes only. John will need to repay the incentive at 10% of the fair market value when he sells the property or after 25 years, whichever is earliest.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2