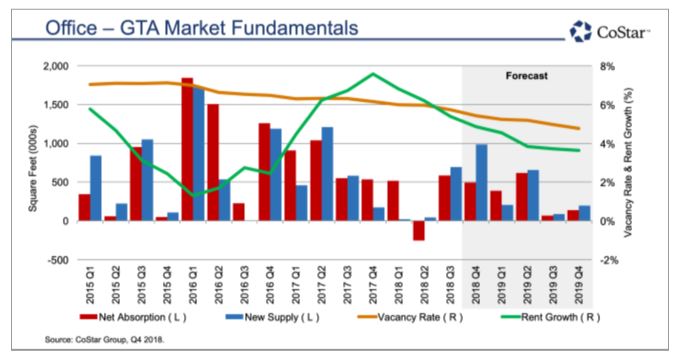

GTA Office Overview

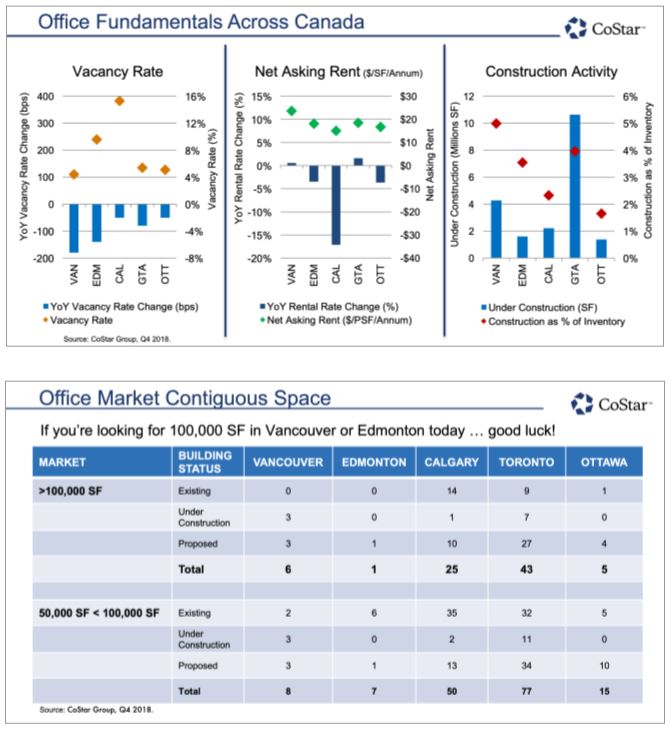

The GTA office market is experiencing exceptionally strong performance and is deeply entrenched in landlord control. The overall market vacancy rate is down 80 bps year-over-year to end 2018 at 5.4, with the average net asking rental rate up 1.6% over the same period to $18.50/SF per annum. With strong demand from finance and technology companies that continues to drive vacancy down, rental rate growth is expected to remain above 2% until approximately 2021, just after the next wave of new supply starts coming online.

There are currently only nine existing properties in the GTA that can accommodate a tenant looking for 100,000 SF or more of contiguous space. The good news on the supply front is that construction activity continues to increase, with approximately 10.5 million SF now under construction or about to kick off, representing 4.0% of existing inventory. These projects include CIBC Square at just under 1.6 million SF with CIBC as the lead tenant; the 1.2 million SF office project at 160 Front St. W., which was announced by Cadillac Fairview in June, 2018 with the Ontario Teachers’ Pension Plan as the lead tenant; and the 829,910 SF speculative project at 16 York St., also being developed by Cadillac Fairview. Furthermore, Oxford Properties continues to market its proposed 1.4 million SF (60-story) office tower, The HUB, at 30 Bay St. Although there is a mountain of new supply in the development pipeline, it should be noted that this new supply will do virtually nothing to alleviate the tight market conditions until it starts being delivered between 2020 and 2022.

Downtown vacancy remains exceptionally tight, at 3.2% at year-end 2018, and although this is down 50 bps year-over-year, it is up 20 bps from Q3 2018, whereas the suburban market vacancy rate has decreased by 100 bps year-over year, to 6.5%. Although suburban vacancy is now falling faster than downtown vacancy, with the delta between downtown and suburban vacancy narrowing from 380 bps a year ago to 330 bps at year-end 2018, there continue to be many opportunities in the suburbs for tenants who do not need to be downtown. Furthermore, tenants will likely need to pay more attention to the suburban markets if they need a large amount space before 2020. With demand remaining strong, and new supply limited in the short term, expect rental rates to continue edging up

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2