MARKET SUMMARY

With the first two months of 2019 behind us, there was no shortage of events fueling political and economic uncertainty in Canadian markets. From Jody Wilson-Raybould’s recent response to allegations that she was pressured by the Prime Minister’s Office to intervene in criminal proceeding against SNC-Lavalin to the ongoing extradition case of Huawei’s CFO, all could pose major ramifications for the Canadian economy in terms of trade, employment and growth. Even with these potential challenges facing the federal government, there were some signs of progress. Firstly, Canadian financial markets surged as the S&P/TSX Composite Index rebounded by 11.7% over the past two months after plummeting by 5.8% in December alone. Moreover, the implementation of oil production cuts in Alberta has had a positive impact on oil prices, as the price differential between West Texas Intermediate (WTI) and Western Canadian Select (WCS) has narrowed to approximately $12.50/barrel. The surge in value of WCS since December to $44.25/barrel has also supported the appreciation of the Canadian dollar to $0.76 USD. Even with the recent increase in oil prices, the Bank of Canada will likely hold off on raising interest rates until the fall of 2019 due to slowing economic growth (both within Canada and globally), easing inflation, weak recent data on retail sales and the tumble that the housing market has taken due to the new mortgage rules and higher interest rates.

The latest GDP data for Canada, which was released on March 1st, shows that the Canadian economy only grew by 0.4% annualized in Q4 2018, reflecting the toll that weak oil pricing, the slow housing market and weak business investment is taking on the economy. Economic growth in Canada is predicted to decline from a lower than expected 1.8% in 2018 to a forecasted 1.5% in 2019. Ontario is expected to only slightly outperform Canada as a whole, with 2019 GDP growth forecasted to come in at 1.6%.

The Greater Toronto Area (GTA) on the other hand is one of only a few markets across Canada that are expected to see GDP growth increase in 2019, up 10 basis points from 2018 to 2.4%, however, this is based on the assumption that consumer spending and housing sales will pick up. On the residential housing front, GTA home sales in 2018 were down 16.1% from 2017, and the average selling price for all property types was down by 4.3%. Although sales and prices picked up slightly in January, they remain weak, with many now calling on Ottawa to review the mortgage stress testing rules, as it is having a deeper impact on the housing market than anticipated and still making housing unaffordable for new home buyers. A weak housing market always impacts consumer confidence, and with five interest rate hikes over the past 18 months, mortgage and lending rates are finally catching up to households. This combined with a 2.3% increase in the CPI Index for Ontario during 2018 will directly affect consumer spending in 2019. As consumption and residential housing were key contributors to economic growth in Canada, Ontario and the GTA over the past several years, slowing demand in both sectors will shift the focus towards business investment and exports.

Given this economic backdrop, the office, industrial and retail commercial real estate markets in the GTA continue to perform well and remain well within “landlord” market status. The office market vacancy rate has decreased by 90 basis points (bps) year-over-year to end February of 2019 at 5.0%, with the average net asking rental rate up 5.6% over the same period, to $19.51/sq. ft. per annum. With exceptionally strong demand from both finance and tech tenants driving down vacancy and pushing net asking rents up, it is no surprise that landlords and developers are confident about the future performance of the GTA office market. Furthermore, although rental rate growth has begun to slow, growth will remain positive for the foreseeable future. As such, construction activity continues to increase. There is currently almost 10.6 million SF of office space either under construction or expected to break ground imminently in the GTA, representing over 3.9% of existing inventory. These projects amount to approximately 8.4 million SF downtown, and represent 8.9% of the existing downtown inventory. Downtown vacancy remains tight, at 3.4% at the end of February 2019, however, it is up 10 bps year-over-year as limited options. It should be noted that meaningful new supply is now 12 to 18 months away, and those tenants who can hold off until the new supply starts coming online, will do so rather than taking space that may not necessarily meet their needs, resulting in a temporary slowdown absorption activity. Due to limited options downtown, suburban demand continues to pick up, with suburban vacancy down 160 bps year-over-year to 5.9%. With demand remaining strong, and new supply limited in the short term, expect rental rates to continue edging up. Downtown net rents are up approximately 20% year-over-year at $33.42/sq. ft. per annum, however, they are off slightly from $33.44/sq. ft. per annum at year-end 2018. Suburban rents have increased by only 4.3% year-over-year to $18.03/sq. ft. per annum in February 2019 and were up 1.1% since year-end 2018.

The industrial market experienced a 100 bps drop in vacancy year-over year to end February 2019 at an exceptionally low 1.4%, with availability down 100 bps over the same period to 2.3%. As a result of strong demand and limited availability and new supply (only 3.5 million SF in 2018), the average net asking rental rate continues to increase, up almost 13.7% year-over-year, to $7.8219/sq. ft. per annum in February 2019. Low vacancy rates and continued demand from transportation and warehousing users as well as non-traditional users such as film and television production, self storage operators and cannabis grow operations is driving both demand and increased construction activity. Construction activity is now at 10.6 million SF, compared to only 5.6 million SF a year ago, and this activity equates to 1.3% of the current market inventory. As a result of the above, and the fact that there is limited land available for new projects, expect vacancy to remain low and rental rates to continue rising. Rental rate expectations from landlords for new construction projects are increasing even further due to rising construction and land costs, and as a result, both landlords and tenants are going to have to start looking even further out around the periphery of the GTA for suitable options. On the retail front, despite the exit of several retails over the last year, both big and small, and weakening retail sales as a result of rising debt servicing costs for households, Canada, and the GTA specifically, continue to attract retailer expansions and new retailers. As a result, the retail vacancy rate has decreased by 100 bps year-over-year to 2.1% at the end of February 2019, with the average net asking rental rate up by 9.0% year-over-year to $26.12/sq. ft. per annum. The delta between the have’s and have not’s when it comes to retail properties, continues to grow. The landlords that are able to update and renovate their properties in order to attract the best tenants are also attracting the most traffic, whereas the landlords who are not, are being impacted the most.

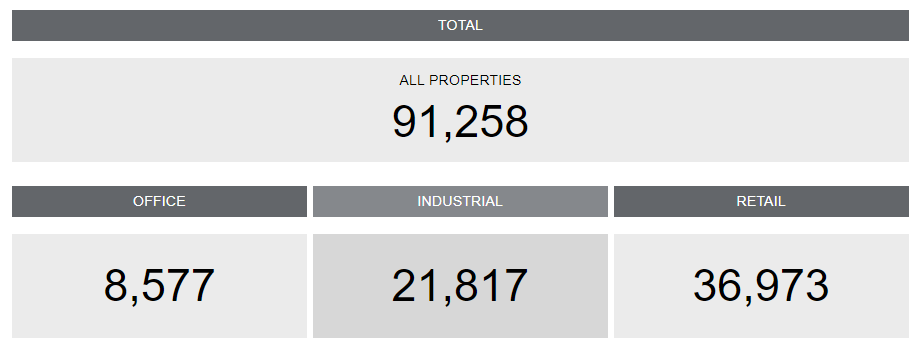

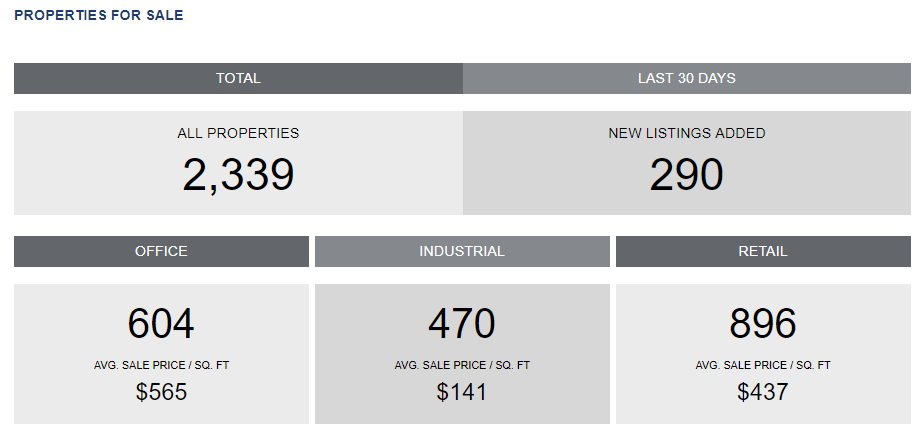

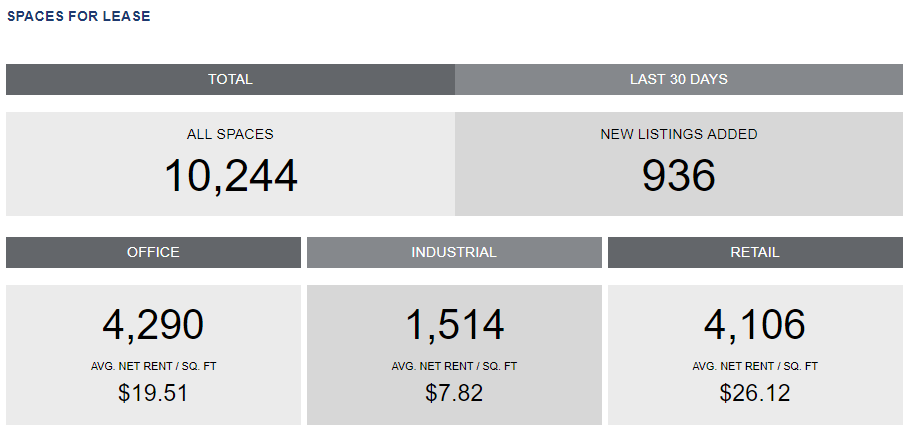

These insights are made possible through CoStar, the largest commercial real estate source for property listings for sale or lease in Canada. CoStar enables users to gain insight into the approximate 91,258 properties currently tracked in the Greater Toronto Area, which include 2,339 properties for sale and 10,244 spaces for lease.

Source: Costar

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2