Toronto is known for many things as Canada’s biggest and most bustling city. Some of these are positive, like its diverse culture, rich history, and fan favourite sports teams. Others, not so much, like the incredibly high cost of living that Torontonians get to enjoy.

Though the title for most expensive of all is often traded with Vancouver, there is no question that these two cities simply cost the most to live in among all in the country. However, in the case of Toronto, there are at least a few million more residents in the area, making these high prices an issue for many more people.

The cost of living in a given area is a reality that essentially everyone must think about on a daily basis. For those already in the city, the amount of money they need to get by naturally is a major consideration, while for the thousands of new residents that come to the city a year, the cost of living is a major factor that determines whether or not their move is going to work out.

And yes, even for real estate investors the cost of living is a major consideration. Now, if you’re considering investing in real estate in the city of Toronto in 2022, you probably aren’t the type of person who is struggling to make ends meet. However, you are likely hoping your investment performs well and makes you some money in the long run.

The cost of living in a given area can be a major economic driver and will influence local real estate markets in a large way. Understanding this figure can be important for real estate investors looking to conduct due diligence on their property purchases or those who rent properties they own.

In this article, we will explore just what exactly it costs to live in Toronto today, why prices may be going up or down, and ways you can help yourself to afford life in the big city.

What does it cost to live in Toronto?

The amount that a person spends to live in a given area is naturally going to vary from person to person. Each person lives according to their own lifestyle and means, and some may spend far more than others. For this reason, it can be difficult to determine exact figures for the cost of living, though various sources have created estimates based on their own data.

It is also important to know that the cost of living changes all the time, and it isn’t always going up. As prices fluctuate, it can cost more or less to live somewhere on a month-to-month basis. For this reason, data that is even a few months old may not be completely accurate, though it likely doesn’t move so fast as to make it unreasonable to use old data for a ballpark estimate.

With that out of the way let’s look at a few sources of what it costs to live in Toronto.

Renting

In the city of Toronto, it is estimated that about half of the population rents the home they live in, meaning rent prices are a major consideration when looking at cost of living. In general, home expenses for renters are some of the largest regular costs they must contend with.

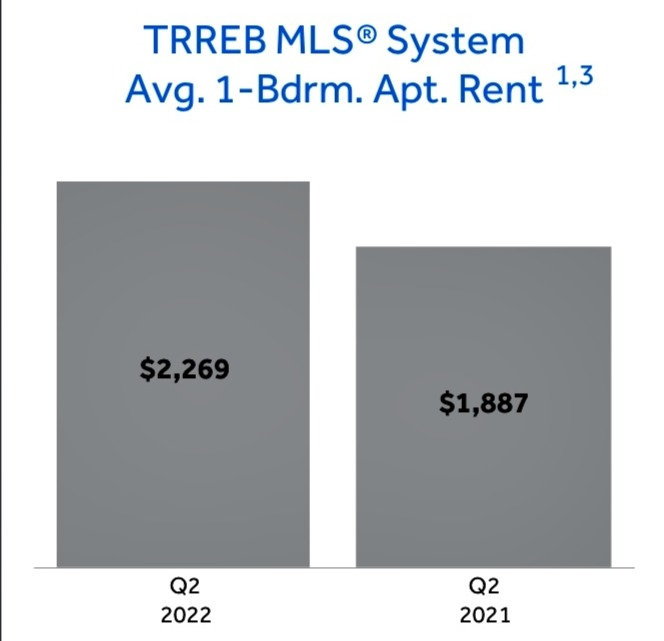

The Toronto Regional Real Estate board tracks rent prices in the GTA on a quarterly basis, with the most recent data release available dating from Q2 of 2022. At that time, the average monthly cost for a one-bedroom apartment was $2269, up from $1887 in Q2 2021.

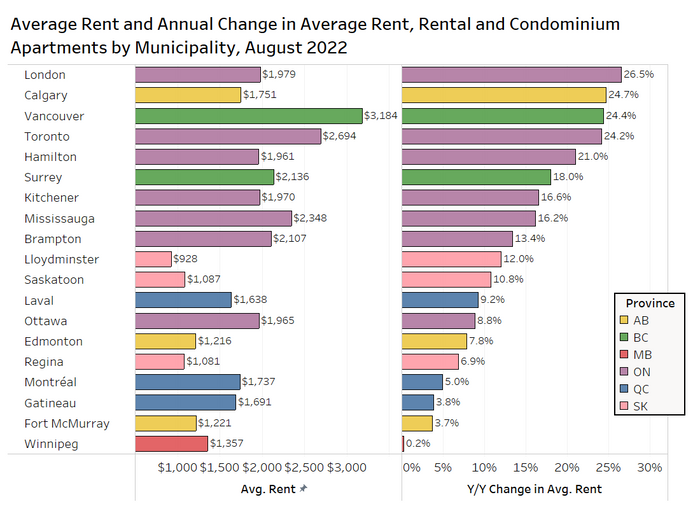

Rents in Toronto proper were very much on par with the regional average ($2279) while Innisfil reported the highest average monthly rent in the GTA at $2850 for a one-bedroom (though data indicates only 7 such apartments being rented in this period, compared to Toronto’s over 6000).

Recently, Statistics Canada released its most recent census data which reports on average incomes across Canada, though these incomes date from 2020, so they may have increased slightly since. At the time, the average after-tax median income in Toronto was $85,000.

To rent the average one-bedroom apartment for a year would cost about $27,350 or around 32% of this average salary The conventional measure for affordable housing is that it should not cost more than 30% of your income. Based on these figures it is clear that many Torontonians are well into unaffordable territory.

Owning a home

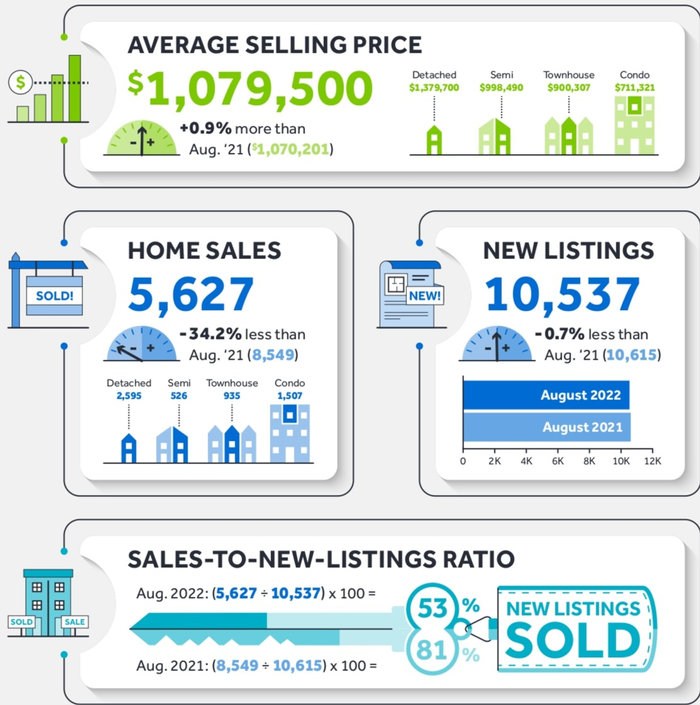

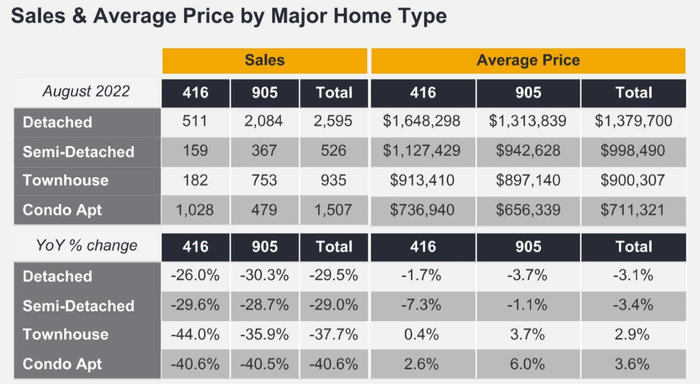

Owning a home may help you to escape the high cost of rent, though you trade that for even higher mortgage carrying costs. This is due in large part to the absolutely massive home prices in Toronto.. At their peak in 2022, home prices hit an average price of above $1.3 million in the GTA.

In recent months, however, prices have begun to fall in many areas, and the current average being reported by TREB is $1,074,754, almost $300,000 less than just months ago. While it may seem that this means the cost of a home has decreased in Toronto, this isn’t exactly true.

The actual price of a home is not the factor that will affect a homeowner most on their monthly bottom line. While home prices have fallen, this has been largely in response to increased interest rates, which actually eroded affordability further for Torontonians. Your home may be cheaper now, but the cost of paying your mortgage will actually have increased.

Down payment costs

Before you can buy a home you need to first surpass the barrier of a large down payment. Remember: On a home greater than 1 million dollars (as many in Toronto are), the minimum allowable down payment is 20%, or about $200,000.

Looking at the median income from before, and assuming a resident could save 10% of their yearly income (on top of the already high rent prices, and ignoring the effects of inflation) it would take them over 20 years to even have enough for a down payment.

Unfortunately, the median income earner in Toronto would likely have a hard time even being approved for a mortgage Toronto given their high prices. According to a recent report from Ratehub.com, a buyer of an average home in the city would need to make over $200,000 a year in order to service a mortgage.

Mortgage costs

Once you buy the home, you need to consider the carrying cost of a mortgage. Assuming a home of $1 million with 20% down and a fixed mortgage at about 5.5%, your monthly payments would cost over $4800 a month. This is before you consider all other costs of owning a home such as utilities, repairs, furniture, and more. With interest rates still rising, mortgage costs may continue increasing even further in the near future.

Property tax

One piece of good news about the city of Toronto is it does have some of the lowest property taxes in the province. Even given the high cost of homes, residents in Toronto pay less property tax than much cheaper homes in other municipalities. The cost is still not negligible, however, at about 0.6% of the value of your home, or around $6000 a year for the average home.

Other expenses

We’ve spent some time looking at the cost of housing in the city of Toronto. Though this is the largest part of most people’s spending, it is only one component of a household’s average monthly costs. Here are some more costs to consider.

Utilities

For most people their home is much more than just a shelter. We must pay for the various utilities that keep our homes comfortable and keep us connected, such as water, gas, electricity, internet, and mobile phones. These costs will vary a lot between homes and lifestyles, but the estimated monthly costs for utilities can add up in the range of $200 – $500 monthly.

While things like internet costs can vary based on individual plans, the rates for utilities like water, gas, and electricity will be the same across most houses in a given area, so your main option for reducing costs will be simply to conserve your usage.

Essential purchases

Then there are also the essentials of everyday life, such as clothing and food costs. Numbeo.com estimates that an average household in Toronto may spend up to another 30% of their monthly income on food and clothing costs.

Unfortunately, things like grocery costs have been on the rise in recent months, however, residents can save money by reducing food waste, opting for low-cost options, and taking advantage of sales and points programs.

Transportation

Finally, another major component of life in the city is transportation. Luckily, those who live within big cities have much better public transit options than in many other areas. Say what you like about the TTC, but you must admit that it is far better than the alternative of no transit at all, such is the case with many rural and remote areas.

With public transit, residens can get around the whole city quite easily via subways stretching from Union Station in Downtown Toronto to the far edges of the city, as well as an extensive system of bus routes. Though the routes in the TTC system cover the city quite comprehensively, everyday riders will inevitably be forced at some point to contend with delays and other headaches that come with public systems.

With a yearly plan, riders can get a discount on their monthly pass and access the TTC network for $143 a month. Without a yearly plan, a monthly transit pass regularly costs $156, and discounts are available for seniors, youth, and post-secondary students. While this can likely be much cheaper than a car based on how much you travel, it may also be much more inconvenient based on your lifestyle.

If you choose to own a car in the city you open yourself up to a whole new range of expenses. The cost of each household’s personal vehicle will vary on a number of different factors including the car you buy, financing costs, your insurance rates, your maintenance needs, and how much you drive. All transportation costs factored in this can easily cost a driver more than $500 a month.

How much do I need to make to live in Toronto?

If you are hoping to live in the City of Toronto or the GTA, figuring out if you have enough money will be a major deciding factor. As mentioned before, the most recent census reports an average median income of $85,000, meaning at least half of the city is at or below this line.

Now, naturally the more you can make the better, and those who are only earning minimum wage will find it much harder to get by than higher earners. Though it may seem intimidating, there are a number of benefits that can make a life in the city comfortable despite the costs.

One such factor would be a large number of housing options, allowing you to split your bills with various roommates (though you will still need to contend with low vacancies). Another benefit is a large number of jobs in the city, many of which are relatively well paying. And finally, options like public transit can help you to reduce expenses that may be harder to reduce in smaller cities and towns.

For those hoping to buy a home, you have a much harder task ahead of you. Saving a large enough down payment will likely be your largest difficulty in buying a home in Toronto, but in order to maintain your mortgage estimates indicate you would need to make a combined household income of over $200,000 or more. Again, similar benefits apply when buying in the city – lots of job options, and many different housing types and areas. If you plan on buying a family home and you work in the city, it may be worth considering becoming a commuter to enjoy less crowded, and less expensive, areas in the region.

Are prices going up in Toronto?

Across the board, the cost of living has generally been increasing in Toronto, like in most of Canada. The way we know this is due to the inflation rate.

Many people think that the rate of inflation is an abstract measure, but in reality, it is based on a well understood formula known as the Consumer Price Index (CPI). The CPI tracks a set basket of everyday costs that reflect the average cost of living. These include things we have mentioned here: food prices, clothing, housing, utilities, transportation, and more.

The CPI is a retroactive measure – it looks back at how prices have risen over a given period, meaning an increase in CPI indicates an actual rise in prices, not a hypothetical future increase.

Even as the Bank of Canada attempts to slow inflation, a lower inflation rate still represents an overall growth in prices. Inflation when kept under control, is not a huge issue – when growth is slower, however, people are able to adjust more easily and wages can keep up with inflation. When inflation is too high, it can quickly become too much to handle, thus recent efforts to slow its pace.

Why is rent increasing?

As mentioned before, the price of rent has been increasing for the last year or so as well. This is due in part to the increased costs of things like utilities and maintenance equipment that increase the costs of running a rental property.

On the other hand, the rise in rent can also be seen as a symptom of supply and demand. The supply of rental inventory in the city is very low, with less than 1% vacancy across much of the GTA. At the same time, the demand for homes is only increasing with the return of many post-secondary students, immigrants, and those wishing to live close to their jobs. There has also been an increase in the rental market from the many people being pushed out of homebuying by increased costs of buying.

Why are home prices falling?

The prices of homes in Toronto have actually been trending down in recent months. The largest cause of this downtrend is the rise of interest rates, which affects how much buyers are able to afford to borrow, putting downward pressure on the sky-high prices seen previously.

However, Toronto real estate has long held value very well. While the city has gone through down periods in the past, it has always turned around eventually, and the upward growth of prices in the city over the long term is a near certainty. Prices may be down temporarily, but they are unlikely to fall so low to be considered anywhere near cheap or even affordable.

Affordability tips for living in Toronto

For those concerned with the rising costs of living in the city, there are luckily some ways that you can help to make your lifestyle more affordable. Short of increasing your income, which is often out of one’s control, the best options are ways to reduce your overall expenses. here are some things to consider:

- Use public transportation whenever possible if you aren’t already. The cost of gas, parking and car payments can take a serious dent out of your finances.

- Reconsider your living arrangements. This could include living with roommates to help split bills, moving to a different neighbourhood if you are a remote worker or don’t mind the commute, or even leaving the city altogether if the high housing costs simply aren’t worth it anymore. Living as a single person will usually cost more than living with others.

- If buying a home, consider looking into first-time home buyer incentives and rebates, such as the land transfer tax rebate that can save you thousands on your home purchase.

- You may also want to consider alternate housing outside of the popular single-family home. Townhouses and condos are both abundant and much cheaper for example. Another option may be to co-buy with friends and family or live in a multigenerational living arrangement.

- If you own a home, think about renting out a portion of your property to help offset the costs of your mortgage. This not only helps you to save money but also adds much-needed rental inventory to the marketplace.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2