The Canadian housing market’s performance has been even worse than TD expected, but there are multiple reasons one of Canada’s biggest banks doesn’t predict “a further sustained deterioration” — or worse — this year.

“These [reasons] include another year of strong population growth, healthy labour market conditions and a more patient Bank of Canada,” writes Rishi Sondhi, a TD economist, in a report titled “The Winter of Discontent.”

TD goes on to chart four of the trends it expects to insulate the Canadian housing market from a worse year than 2018, which saw the biggest price drop since 1995.

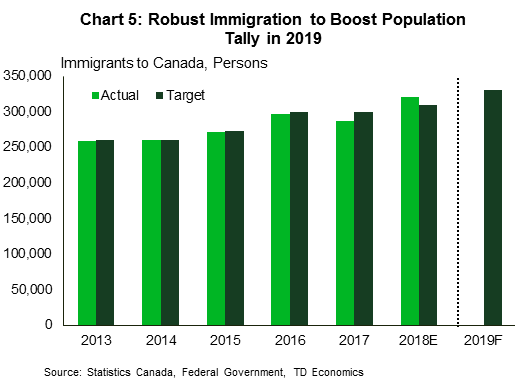

Immigration drives a housing fundamental: population growth

What’s going on here: Federal Immigration levels dating back to 2013, including a forecast for this year’s total.

The takeaway: A growing population supports demand for new homes, and TD notes that the Canadian government’s immigration target for 2019 is 331,000, up from 330,000 last year. “Moreover, a significant portion of Canadian residents are in their household formation years, providing a solid foundation for demand,” writes Sondhi.

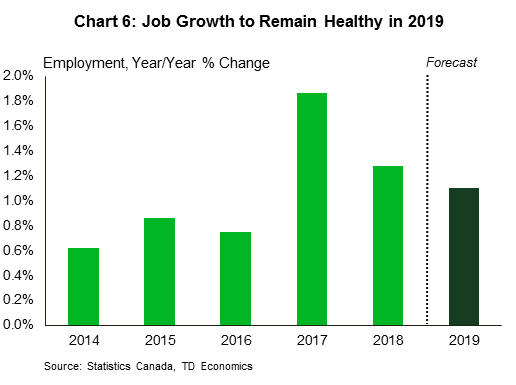

Canadian labour market to post “healthy” gains in 2019

What’s going on here: Annual employment growth presented as a percentage.

The takeaway: “Our forecast calls for over 150k jobs being added in 2019 while unemployment remains low. This should keep household incomes growing at a reasonable pace,” says Sondhi.

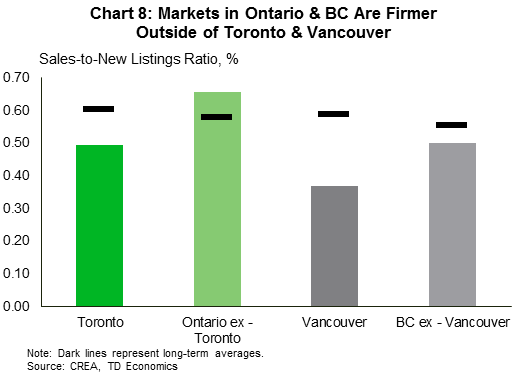

Toronto and BC are soft, but not all surrounding local markets are equal

What’s going on here: TD shows the sales-to-new listings ratio, which is an indicator of market strength, for Toronto and Vancouver, as well as the respective provinces they are in (minus those markets).

The takeaway: Ratios above 60 percent indicate conditions that favour sellers, and clearly a number of markets in Ontario are holding their own. “Outside of Toronto and Vancouver, an important (and perhaps overlooked) point is that markets in Ontario and B.C. are holding up much better,” Sondhi explains.

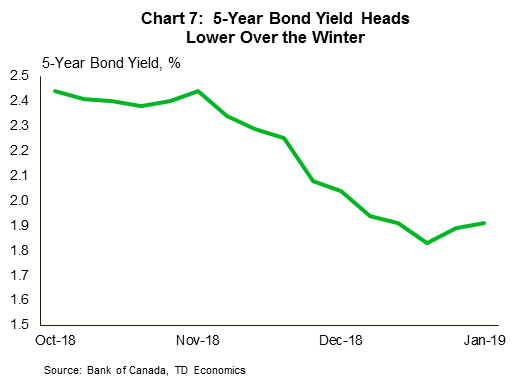

Five-year bond yields are trending lower, and that matters

What’s going on here: The yield on five-year bonds has been generally declining since late last year.

The takeaway: While the central bank’s policy rate tends to influence variable mortgages, the five-year bond yield has pull on five-year fixed-rate mortgages, the most popular option for Canadian borrowers. “Bond yields have moved significantly lower since November, which should feed through into lower mortgage rates.” Fixed-rate mortgages are more influenced by their corresponding government bond yields, as banks fund mortgages with bonds.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2