A recent Ipsos survey painted a grim picture for many Canadians: apparently, nearly half are $200 or less from being too broke to pay the bills.

The annual survey of more than 2,000 adults in Canada garnered dire headlines across the country, with nearly a third of respondents reporting they haven’t any money left over at the end of each month.

However, National Bank’s deputy chief economist, Matthieu Arseneau, suggests the headlines are “more bark than bite” despite access cheap credit in recent years leading to ballooning debt as homebuyers took advantage of historically low mortgage rates.

Arseneau calls attention to last year’s version of the same survey. In it, 33 percent of respondents said they had no wiggle room with their finances.

“What happened next is interesting,” writes Arseneau in a Hot Charts note.

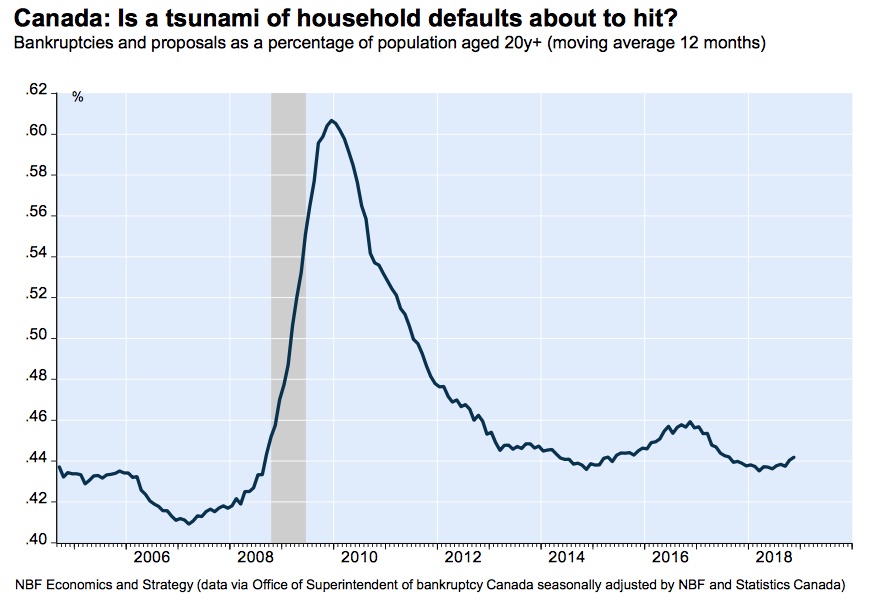

Namely, loan defaults, which occur when borrowers stop making monthly loan payments, didn’t surge. In fact, according to the most recently available data, although insolvencies increased 5.2 percent in November compared to 12 months ago, actual bankruptcies remained around record lows.

Insolvency data muddies the issue because it lumps proposals in with bankruptcies. Proposals are plans borrowers put forward to restructure debt, sometimes extending the timeline of a loan, for instance.

The 5.2 percent increase in November, then, reflects an increasing number of proposals rather than rising bankruptcies.

According to National Bank, the insolvency ratio (that’s bankruptcies and proposals as a percentage of the Canadian population, aged 20 and up) is only slightly up, hovering at 0.44 percent.

“That’s in sharp contrast to the 33 percent tsunami suggested by last year’s survey,” Arseneau points out.

The tsunami may not have come, but high household debt in Canada has been flagged as a risk for the economy.

As interest rates have begun rising in the wake of five Bank of Canada policy rate hikes since July 2017, there have been concerns about Canadian households’ abilities to service debt, such as keeping up with mortgage payments.

National Bank provides a few reasons insolvencies haven’t increased sharply with the arrival of higher rates. Disposable incomes are trending higher and Canadians are tightening their belts, putting off optional purchases.

While the general consensus is not one of a major financial crisis, CIBC says in another report out this week that it’s “reasonable” to expect the Bank of Canada’s previous rate hikes will moderately push the insolvency rate higher.

“The negative impact of increased debt financing costs will offset any positives on the unemployment front,” writes CIBC Deputy Chief Economist Benjamin Tal.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2