A decade ago, an office landlord might have gone into crisis mode upon learning a tenant as big as Canadian Imperial Bank of Commerce was preparing to flee to a new development down the street. But these days, perhaps nothing says more about demand for office space in downtown Toronto than QuadReal Property Group’s response to precisely that scenario.

While the first tower of Ivanhoé Cambridge’s 2.9-million-square-foot CIBC Square rises next to Union Station, QuadReal, rather than fretting over a huge impending vacancy at its venerable Commerce Court complex next year, is working with city planners to add 1.8 million square feet of space to the complex with a new 64-storey tower.

And, as an exclamation point, no one seems to be questioning the sanity of QuadReal or its parent, B.C. Investment Management Corp. (BCI), to create the new tower that would stand as tall as BMO Tower at First Canadian Place, which has long held the place of Toronto’s tallest office building.

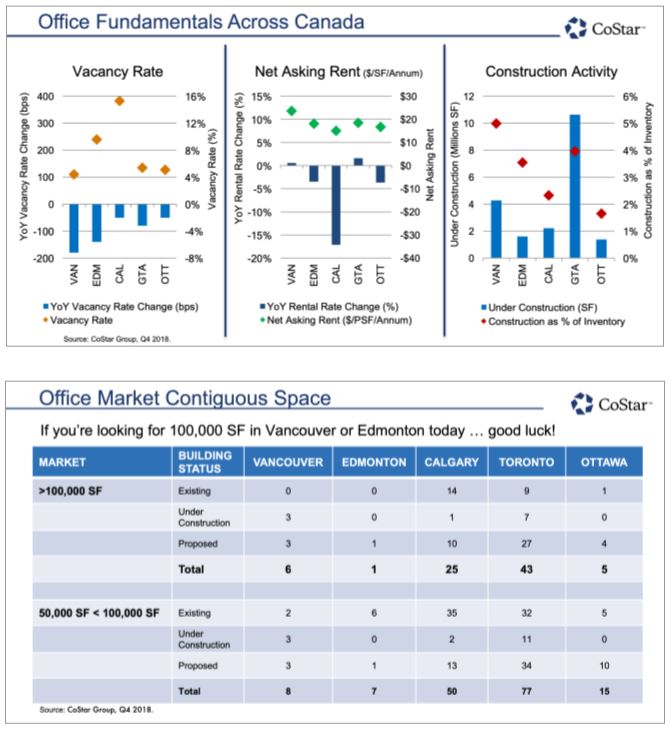

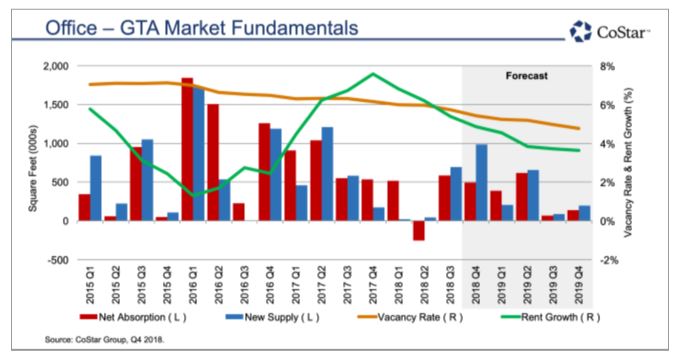

There’s 10.1 million square feet of new office space in the pipeline for Toronto’s core, but with none of it slated to open for more than a year, there’s apparent consensus that demand will further outstrip supply in 2019 – and that’s in a market that has already been North America’s tightest for more than four years.

“Americans I’ve talked to are amazed,” says Daniel Holmes. “I can’t believe this hasn’t been making headlines.”

Thomas Forr, research director points out that while there’s lots of new space coming, just 2.3 million square feet is vacant, much of it in small blocks.

“We’re absorbing about a million square feet a year without new product coming online till 2020,” Mr. Forr says. “So you could soon have a 1-per-cent [vacancy] rate, maybe even 0 per cent with the activity we’re seeing.”

The broader Toronto market has about a 3-per-cent vacancy rate, but it’s already between 1 and 1.4 per cent in the core, depending on whose data you use.

Average asking net rents are up 38 per cent since 2013, and Mr. Forr and Mr. Holmes both say tenants with leases due to expire have learned they now have to search aggressively two or more years in advance to ensure they have much choice if they want new digs.

It’s a sharp contrast to a decade ago, when big new office buildings started to rise again for the first time since the early 1990s recession. That wave of development (2008-2011) brought about three million square feet to market and had some expressing fears about a potential space glut. Now, after another five million square feet was added between 2012 and 2017, there’s the coming 10.1 million, which should all be open by 2024.

“Nobody’s getting reckless,” Mr. Forr at JLL says. “If you look at downtown or even across Canada, there’s still a conservative ownership and development community. You have a lot of pension funds and they’re looking long term. One interesting thing we’re seeing in this cycle is lots of net new tenants coming downtown.”

Five big names on that list include:

– Microsoft, which is moving in 2020 from the airport area, taking 132,000 square feet at Ivanhoé’s CIBC Square.

– Shopify will set up in a new 38-storey tower at The Well, which Allied Properties REIT and RioCan REIT are developing at Front Street and Spadina Avenue (Shopify has taken 253,000 square feet with an option on another 181,000).

– Ontario Teachers’ Pension Plan is moving its head office from North York to a new 46-storey tower that its real estate unit, Cadillac Fairview, is building at Front and Simcoe streets.

– Amazon has taken 113,000 square feet in Scotia Plaza (a building that will eventually lose many of its Bank of Nova Scotia employees to Brookfield’s Bay Adelaide North tower, where construction is set to start this spring).

– Tim Hortons is moving its head office from Oakville to 65,000 square feet in the Exchange Building on King Street.

When asked what factors are driving change most, Mr. Holmes of Colliers replies, “technology and millennials.”

While people recently feared Toronto’s core was overly reliant on financial services, Mr. Holmes says it has diversified, becoming a global player – particularly in tech, which relies on young talent.

“Millennials are choosing first where they want to live and then where they want to work,” he says, adding that Toronto’s core is diverse, welcoming, safe and fun. “Companies don’t want to be further out, even for cheaper rent in a better building. They need to attract and retain top talent and talent is choosing the core.”

Colliers projects that when the coming wave of buildings has opened, Toronto’s vacancy rate will climb to a healthy 6 to 7.7 per cent, which would still be North America’s third tightest, behind Manhattan and San Francisco.

City planners say another 31.9 million square feet are needed by 2041, but industry observers say that’s too far in the future to merit comment. What the golden goose definitely needs, they say, is more rapid transit through downtown, even before the core gets the 200,000 to 300,000 new jobs expected in the next 25 years.

“Transit’s key,” says Mr. Forr, adding Union Station proximity is a big part of Ivanhoé’s success in leasing nearby CIBC Square.

With CIBC, Microsoft, Boston Consulting, AGF and others as its tenants, Ivanhoé’s first tower, scheduled for completion in 2020, was fully leased about 2½ years ahead of Ivanhoé’s usual timeframe. The second tower won’t break ground till 2020, but it is 50-per-cent leased already.

“If we had room for a Phase 3, I think we’d be looking at that very seriously,” says Jonathan Pearce, Ivanhoé’s North American executive vice-president for leasing. He sees transit as so important that it has, in effect, shifted the centre of Toronto’s core south toward Union Station, where all modes of transit converge and where the only certain downtown service expansion is in the works.

As for the prospects of Commerce Court, which began as one tower in 1931, once CIBC starts seriously packing to move down Bay Street, count Mr. Pearce among the optimists. “Toronto is such a strong market that the older-generation product in those iconic towers is still going to lease,” he says.

QuadReal, meanwhile, declined an interview request, but industry people say the planned new tower at Commerce Court, which will replace two shorter buildings to be torn down, will be impressive, is probably six or seven years out, and that there will likely be announcements in 2019.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2