The section on Science Centre Station at Don Mills and Eglinton has been updated with an illustration of the CreateTO proposal for the southwest and southeast corners.

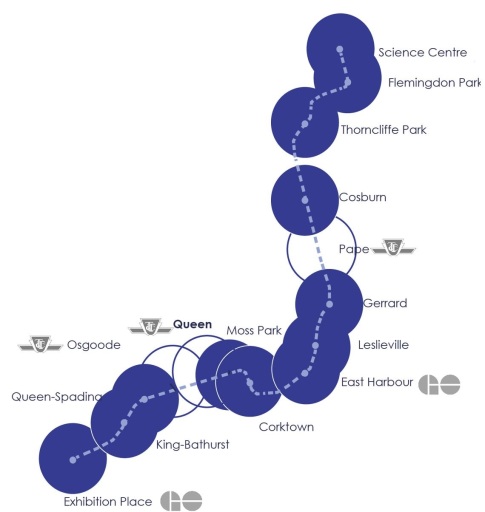

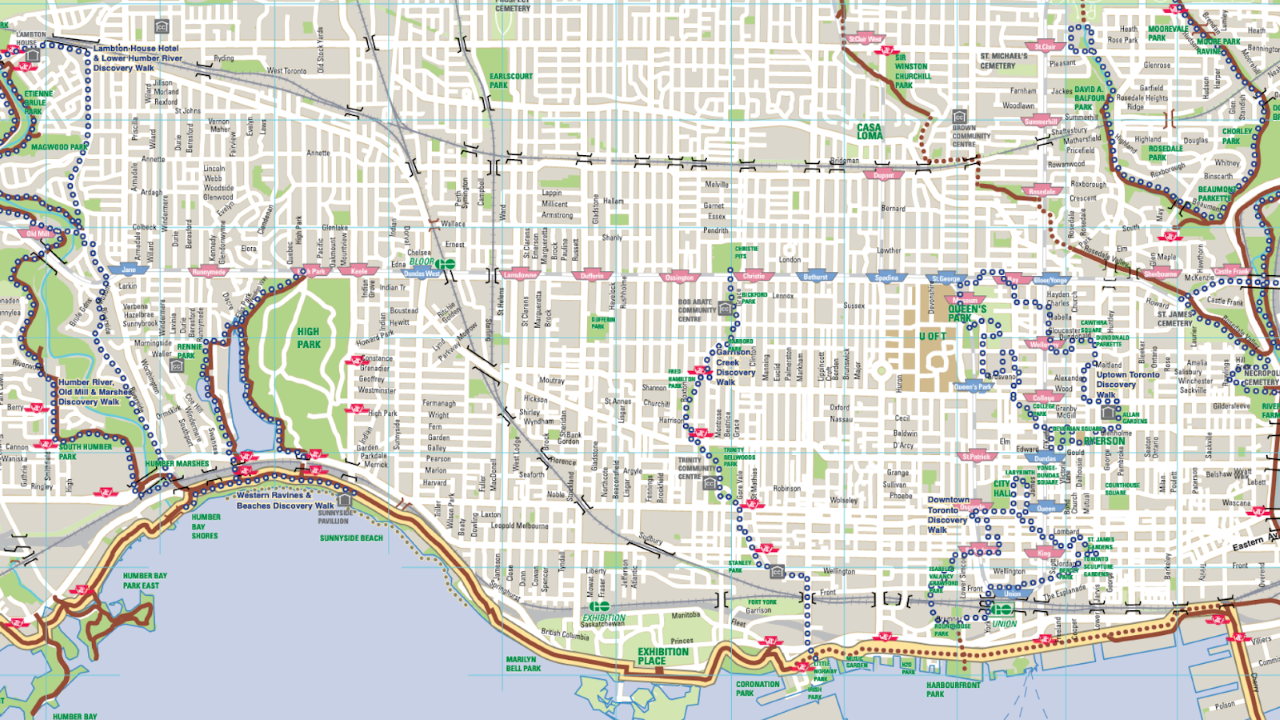

This article combines the speaking notes and presentation deck for my webinar An Ontario Line Tour that streamed on February 1, 2022 under the sponsorship of Smart Density, an Architecture and Planning firm in downtown Toronto. The image below was taken from the announcement of the webinar. It shows the stations on the Ontario Line with their zones of influence drawn as 500m circles around each of them.

Intro:

Thanks for coming today!

To set the stage for what will follow, here is a brief outline.

- Origins of the Ontario Line

- A station-by-station tour from Exhibition to Science Centre

- Planning issues for rapid transit

Illustrations in this presentation come from many sources, but are preliminary in many cases, because the final EA is not yet published with what might be “definitive” (for now) designs.

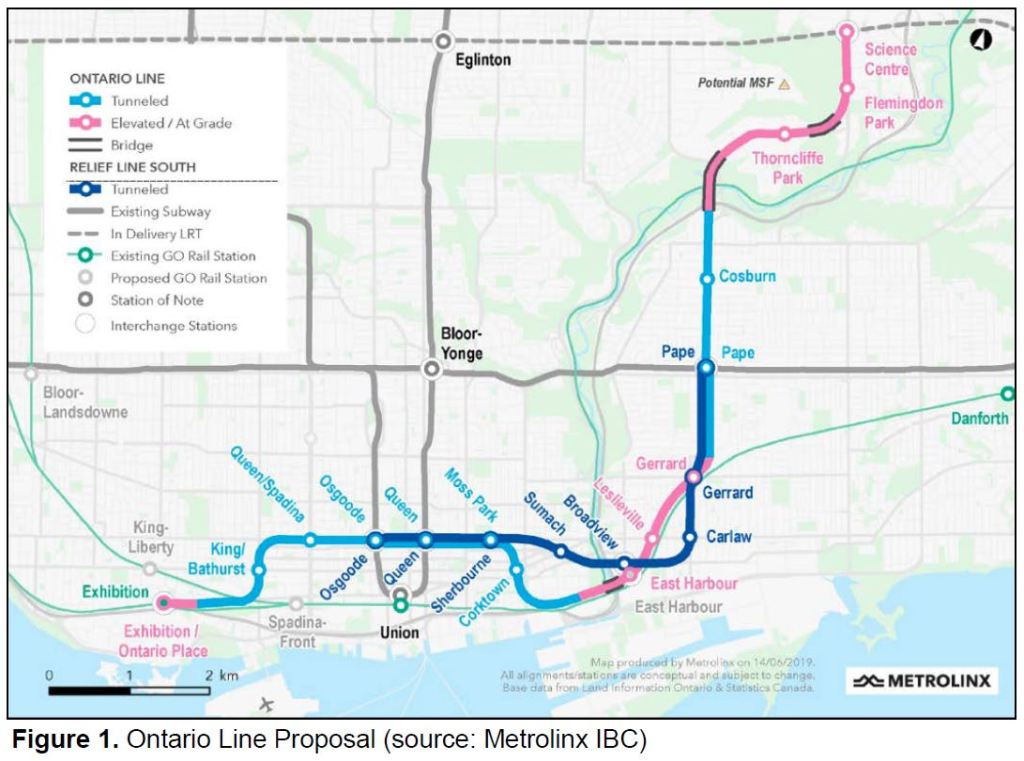

Slide 1: DRL/OL map

The Ontario line replaced the Downtown Relief Line after Doug Ford came to power at Queen’s Park. It follows in a long tradition of new governments tearing up old plans and starting over. On this map we see the Relief Line South in dark blue, and the Ontario Line in turquoise.

For many years, the Downtown Relief Line (DRL) was saddled with the name “downtown”, a poison pill to suburban politicians whose own rapid transit schemes took precedence. It didn’t help that even the TTC downplayed the need for another line into the core until pressure from the proposed Richmond Hill extension eliminated all doubt that more downtown capacity was needed.

The subway has filled up before: in the late 1980s there were severe congestion problems at Bloor-Yonge, but the recession of 1990-95 solved that as the TTC lost 20% of its ridership. More recently we faced another crunch through the 2000s combined with a renewed interest in a Richmond Hill subway. City Council is on record that without a Relief Line (whatever it’s called), the Richmond Hill extension is a non-starter.

This is the map Metrolinx typically displays when they want to talk about how much more rapid transit their proposal yields compared to the Relief Line. It perpetuates a Metrolinx Myth that the northern extension is their brain child, when in fact a line to Don Mills and Eglinton or beyond has been part of transit plans for over half a century.

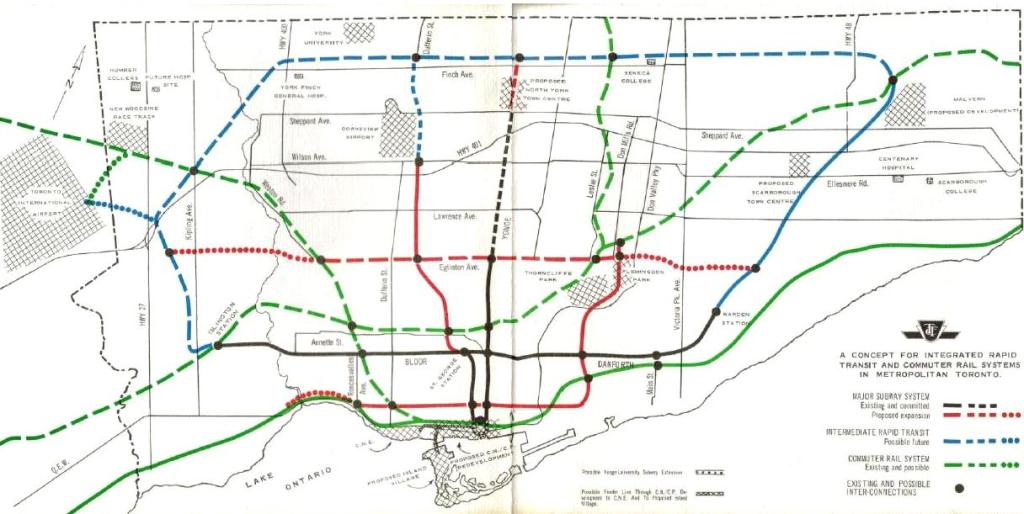

Slide 2: TTC 1969 plan

This is a plan the TTC published in the late 1960s. Notice how the suburban centres were “proposed” and did not actually exist yet. The idea was to build a network of LRT lines (using streetcars repurposed from the downtown system, and later by new cars).

This map looks very familiar with lines that are still on the drawing boards today. The important point here is that the proposed Queen Street Subway went to Don Mills & Eglinton over 50 years ago.

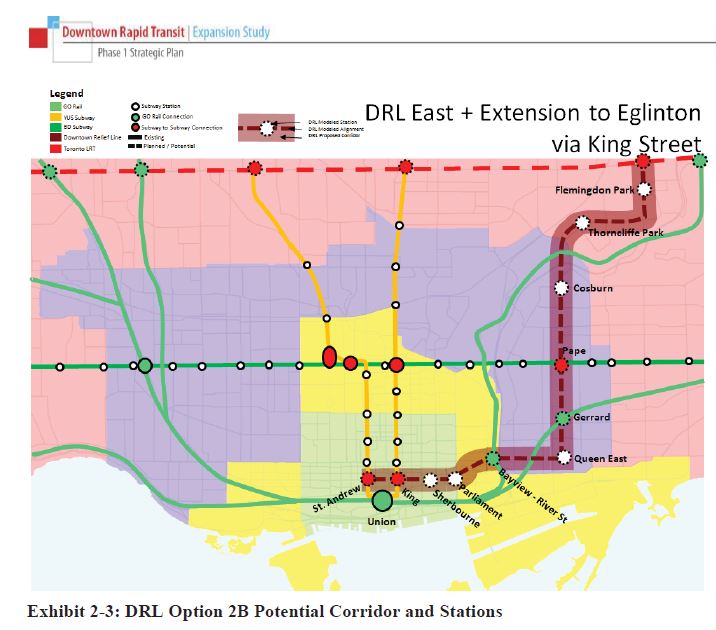

Slide 3: Downtown Rapid Transit Subway (2012)

One version of the DRL from 2012 ran along King Street and north to Eglinton. It was subsequently shifted north to Queen. We can have a debate about which route would be better, but the point again is that the line went to Eglinton.

Because of the project’s size, the development work was divided between the City and the Province through Metrolinx. The City did the south portion from Pape to Downtown, while Metrolinx took on the north segment.

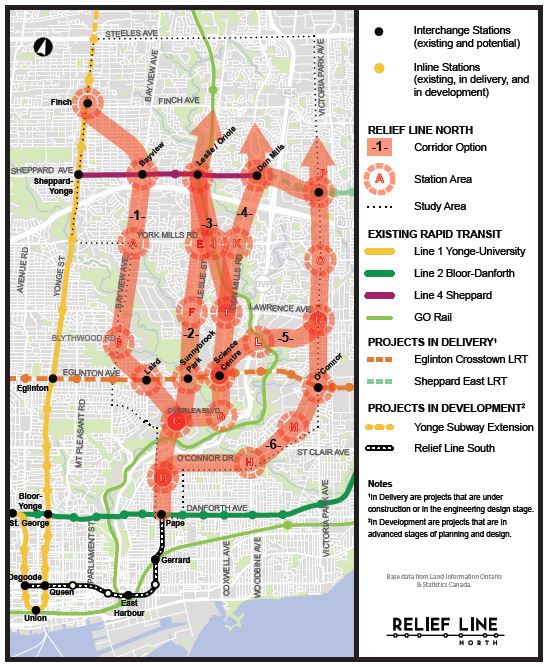

Slide 4: Corridor selection for the Relief Line North (2018)

Metrolinx was slow out of the gate and became mired in corridor selection even though it is fairly obvious that few of the options shown in this map actually make sense. One might almost think that Metrolinx was killing time.

Of particular interest here is that the line was to be studied all the way to Sheppard based on demand projections that showed this would have a profound effect on demand for Line 1 Yonge.

When the writ dropped for the 2018 election, all work stopped. It never restarted, but instead Metrolinx turned internally to crafting a new plan for a new Premier.

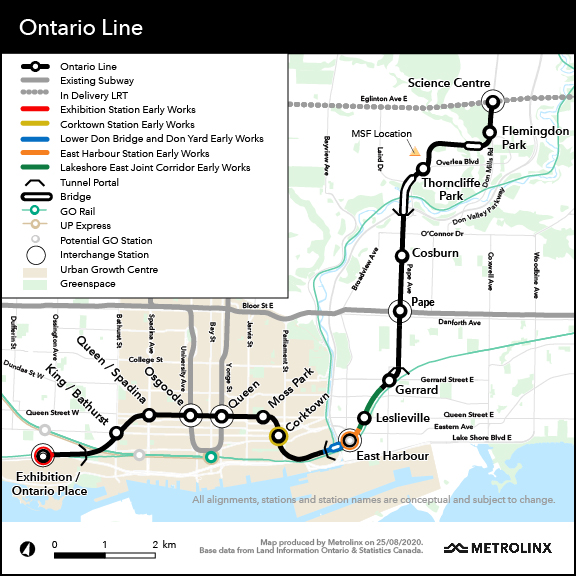

After the OL announcement and enabling legislation to clear away all possible dissent, Metrolinx launched into work on the new Ontario Line linking Ontario Place and the Ontario Science Centre. The route was extended west and south to the Exhibition from Osgoode Station, rerouted through Riverside onto the railway corridor, and changed to an elevated alignment through Thorncliffe Park. I will look at these in more detail later.

Slide 5: Major Contracts and Timing

Having learned their lesson on Eglinton that a single gigantic project brings management challenges, Metrolinx broke up the Ontario Line into four sub-projects. The first of these are the “Early Works” which are all relatively small undertakings in five locations to set the stage for tunnelling, and to resolve physical conflicts with GO Transit before OL construction begins.

There is a separate contract for the rolling stock, systems operations and ongoing maintenance (aka “RSSOM” for short).

This is a different setup from the Eglinton Crosstown line where that RSSOM functions were bundled with the construction project requiring each consortium to assemble its own team of systems providers and operators.

Ontario Line Construction Staging

- Multiple segments with separate contracts

- Early Works

- In progress or about to begin

- South Civils – Tunnels and Stations west of the Don River

- RFP issued Dec 2020, Execution Oct-Dec 2022

- “RSSOM” – Rolling Stock, Systems, Operation & Maintenance

- RFP issued Dec 2020, Execution Oct-Dec 2022

- Includes Maintenance & Servicing Facility at Thorncliffe Park

- North Civils – Tunnels and Stations east of the Don River

- RFQ to be issued July-Sept 2022, Execution July-Dec 2024

- Opening 2030-ish

- Pre-requisite for Richmond Hill Subway Extension to free capacity on Line 1

Note that the award dates for the three big projects are all after the 2022 election, and the north civils contract has not even reached the Request for Qualifications stage.

Metrolinx has recently adopted a more collegial tone about its relationship with P3 partners, and is shifting to a model where project risk is shared rather than being foisted entirely on the builders. Metrolinx hopes that this will make for smoother progress on the OL compared to Eglinton.

Slide 6: Early Works

There are five components to the Early Works, most of which involve locations shared by GO Transit and the OL:

- Exhibition Station (red): GO trackage must be realigned to suit the new station design.

- Corktown (yellow): This is not just a station site, but also the tunnel boring launch site comparable to those we saw on Eglinton east of Brentcliffe and at Black Creek.

- Don River Bridge (blue): Work here includes not just a new bridge over the Don, but also realignment of tracks in the GO yard west of the river to make room for the Ontario Line’s portal.

- East Harbour Transit Hub (orange): This will be a new major station including platforms for GO and the OL, as well as an interchange with the future Broadview Avenue extension and streetcar service connecting south into the eastern waterfront.

- Joint Corridor (green): In order to fit both an expanded GO Transit (4 tracks instead of 3) and two tracks for the OL, the corridor between East Harbour and Gerrard will undergo substantial modification. I will deal with that later in the presentation.

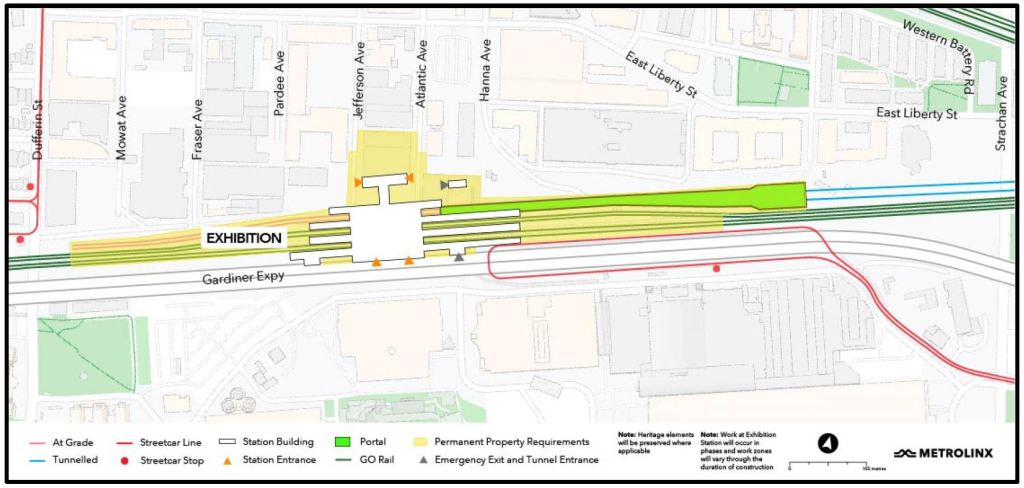

Slides 7: Exhibition Station:

Exhibition Station is the western terminus of the Ontario line, a transfer point with the Lake Shore West GO corridor, and, of course adjacent to the CNE lands and the south end of Liberty Village.

The station will be at grade just north of the GO tracks. The portal (green on the map) leads into a deep tunnel that will run in bedrock under downtown. This avoids complexities with existing buildings and utilities, but makes for very deep stations, typically 40m down to platform level.

The original plan for this station was for the OL tracks to “straddle” the GO station in order to simplify GO Transit transfers, but his proved impractical. A similar problem affected the original design at East Harbour.

The tunnel portal will also be a launch site for TBMs assuming that there will be a drive east from Exhibition.

Slide 8: Exhibition Station Development

Infrastructure Ontario has produced sample plans for development around Exhibition Station. While this is fairly large, the extended Liberty Village around it is much bigger. I will return to Liberty Village and how it fits with various transit proposals later.

Proposed development:

- Atlantic Avenue: 21 + 19 storeys

- Jefferson Avenue: 2 x 19 storeys

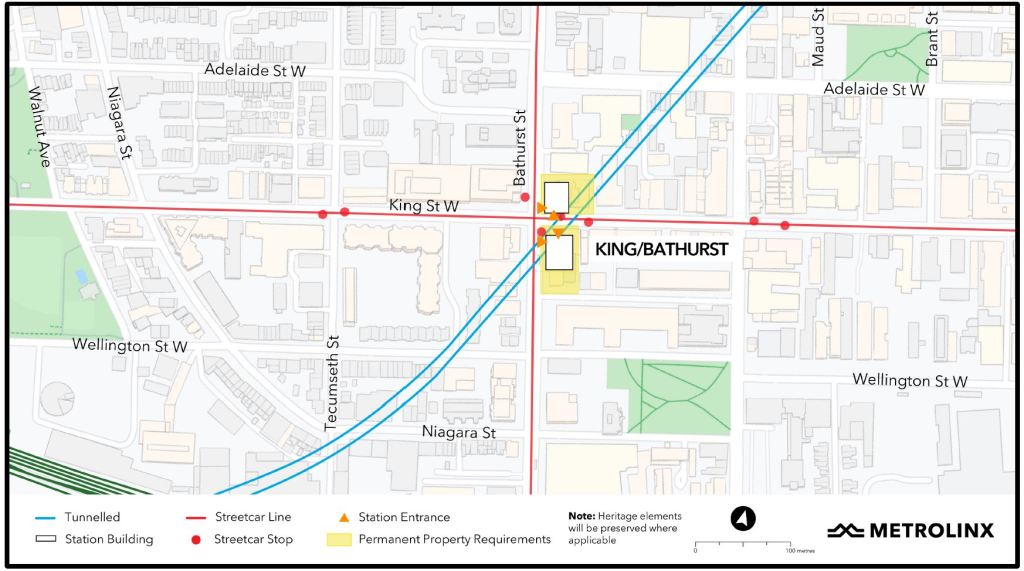

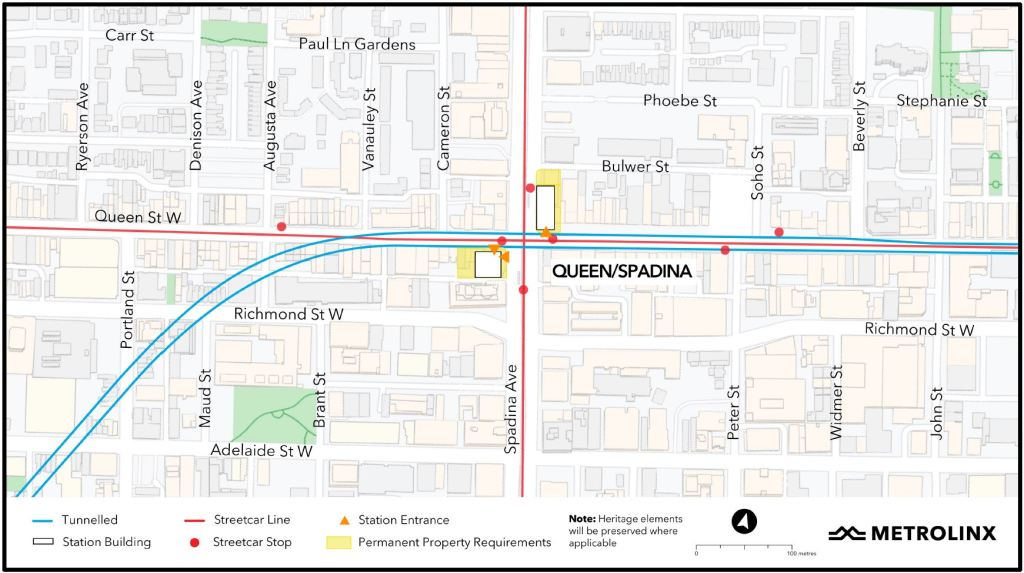

Slide 9: King/Bathurst & Queen/Spadina Stations

These stations share characteristics:

- They will be mined from shafts dug down to the tunnel from two corners of the intersection. The shafts will become entrances.

- In three of four cases, existing buildings have facades that will be preserved as part of new development.

- Surface transit will not (mostly) be disturbed during construction.

Slide 10: King/Bathurst and Queen/Spadina Development

Proposed developments:

- King/Bathurst

- 2 x 25 storey

- Queen/Spadina

- Northeast: 15 storey

- Southwest: 14 storey

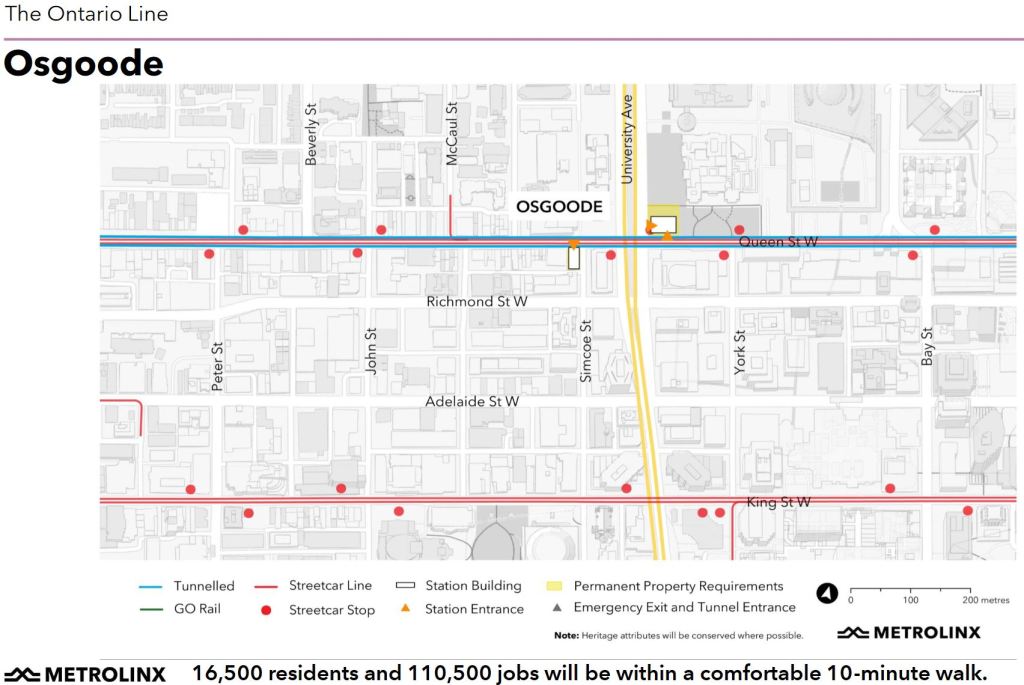

Slide 11: Osgoode Station

Osgoode is an interchange station with the University Subway, but unlike the proposed connection at Yonge (about which more in a bit), current plans call for the OL station to be built under the existing line by mining from either side, not by excavating the entire street. The two access points will be on the southwest corner of Queen and Simcoe, and the northeast corner at University.

Metrolinx has yet to produce any drawings of how the new and existing stations will work together, or how simple transfer connections will be.

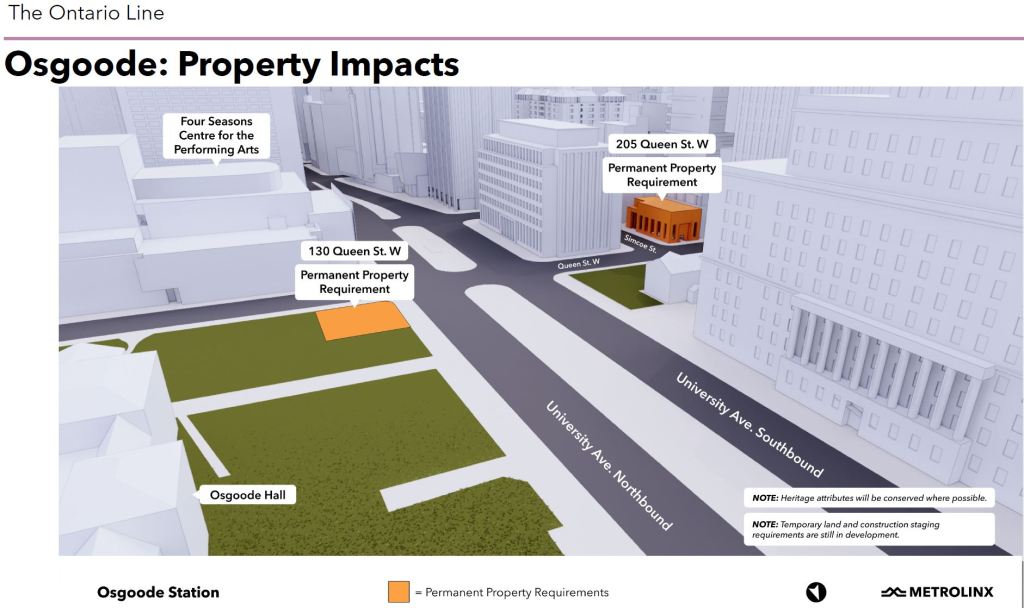

Slide 12: Osgoode Hall Park

The design puts the station entrance in conflict with the park at Osgoode Hall, and there has, strangely, been almost no public comment about this. Lands west of the Hall and north of Queen will be used as a material staging area.

The original RL station was located further east with its entrances on the northwest corner at University (the grounds in front of Campbell House), and at the Queen & York intersection. In the Metrolinx revision the station box was shifted west.

Whether a proposal to convert the east lanes of University Avenue to a park will ever occur remains to be seen. This would effectively shift the space now occupied by the median to the east curb and extending the sidewalk area.

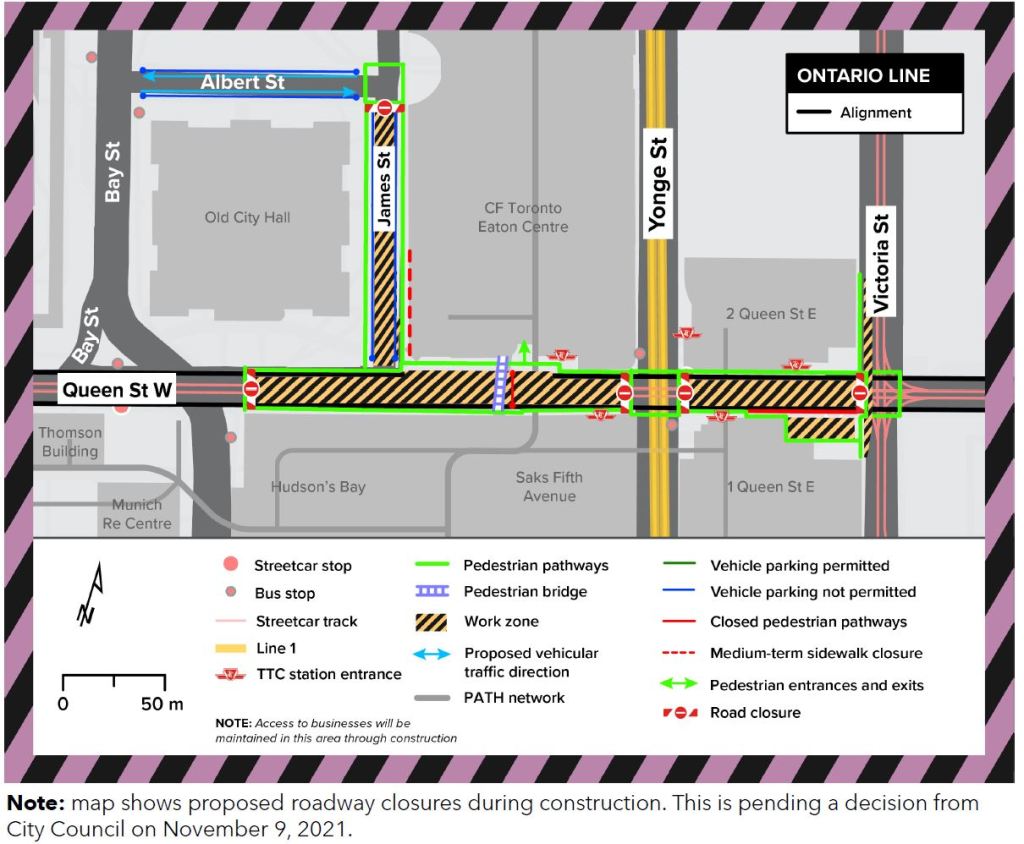

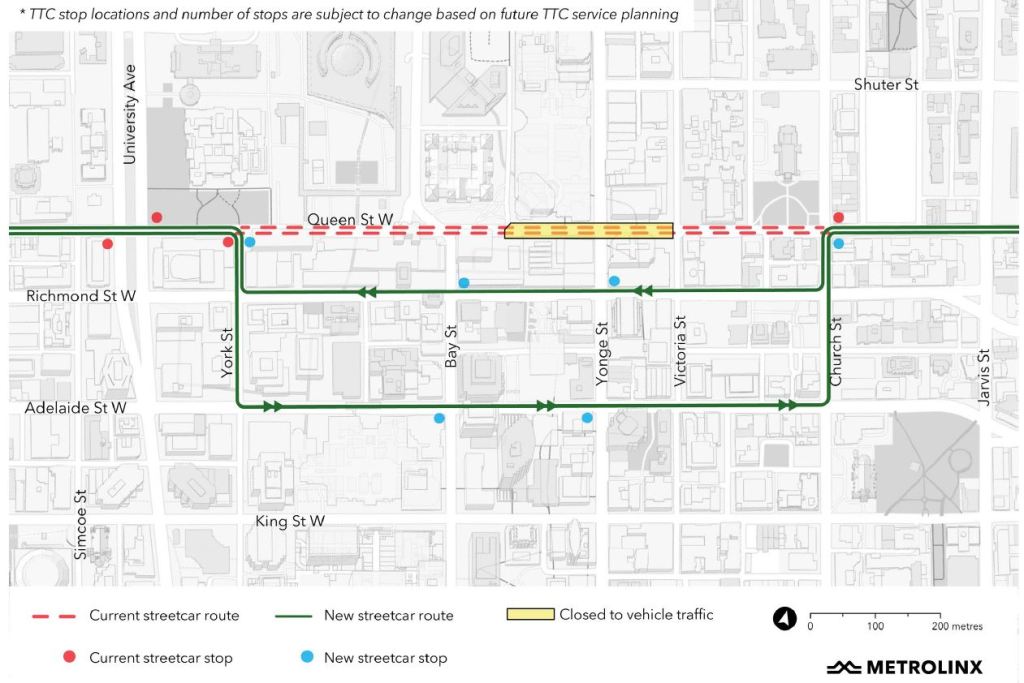

Slide 13: Yonge/Queen

Queen/Yonge Station will be one of the largest single construction sites on the Ontario Line. It will be built with a deep excavation stretching from James Street on the west to Victoria Street on the east. Queen Street will be closed to traffic for over four years, from from May 1, 2023 to November 30, 2027, and streetcars will divert between Church and York Streets.

Yonge Street will remain open crossing Queen.

York will be changed to two-way operation to make this possible. Track on Adelaide will be rebuilt this year to permit operation between Spadina and Church so that diversions are possible over a wider area, notably around TIFF at King and John.

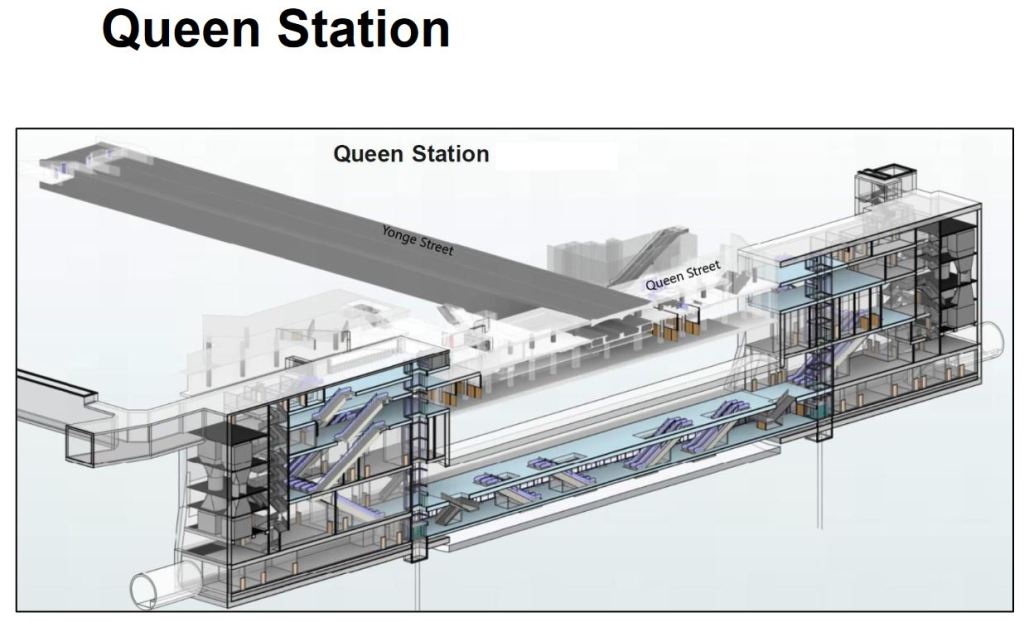

Slide 14: Yonge/Queen Cross-Section

In the cross-section view, the large open block in the centre of the drawing appears as open space, but it is an unexcavated section in bedrock. This will support the existing subway structure while the OL is tunnelled under it. Just above that block is the existing underpass between the northbound and southbound platforms at Queen Station. This was a fragment “prebuilt” for a Queen Street subway 70 years ago, and it will become part of the upper concourse level of the new station.

The station is very deep, one level deeper than the originally proposed “City Hall” station on the RL. Access to the OL station will be via two stair/escalator/elevator towers east and west of the platform.

Moving between the two stations requires walking through the concourse some distance east or west of Yonge Street, travelling vertically by a series of escalators, and then back toward Yonge onto the Ontario Line platform. This will make transfers between the OL and the Yonge line much longer than the kind of transfer we are used to at Bloor-Yonge or St. George. There is some irony in Metrolinx’ focus on simple, fast transfers at East Harbour and Exhibition.

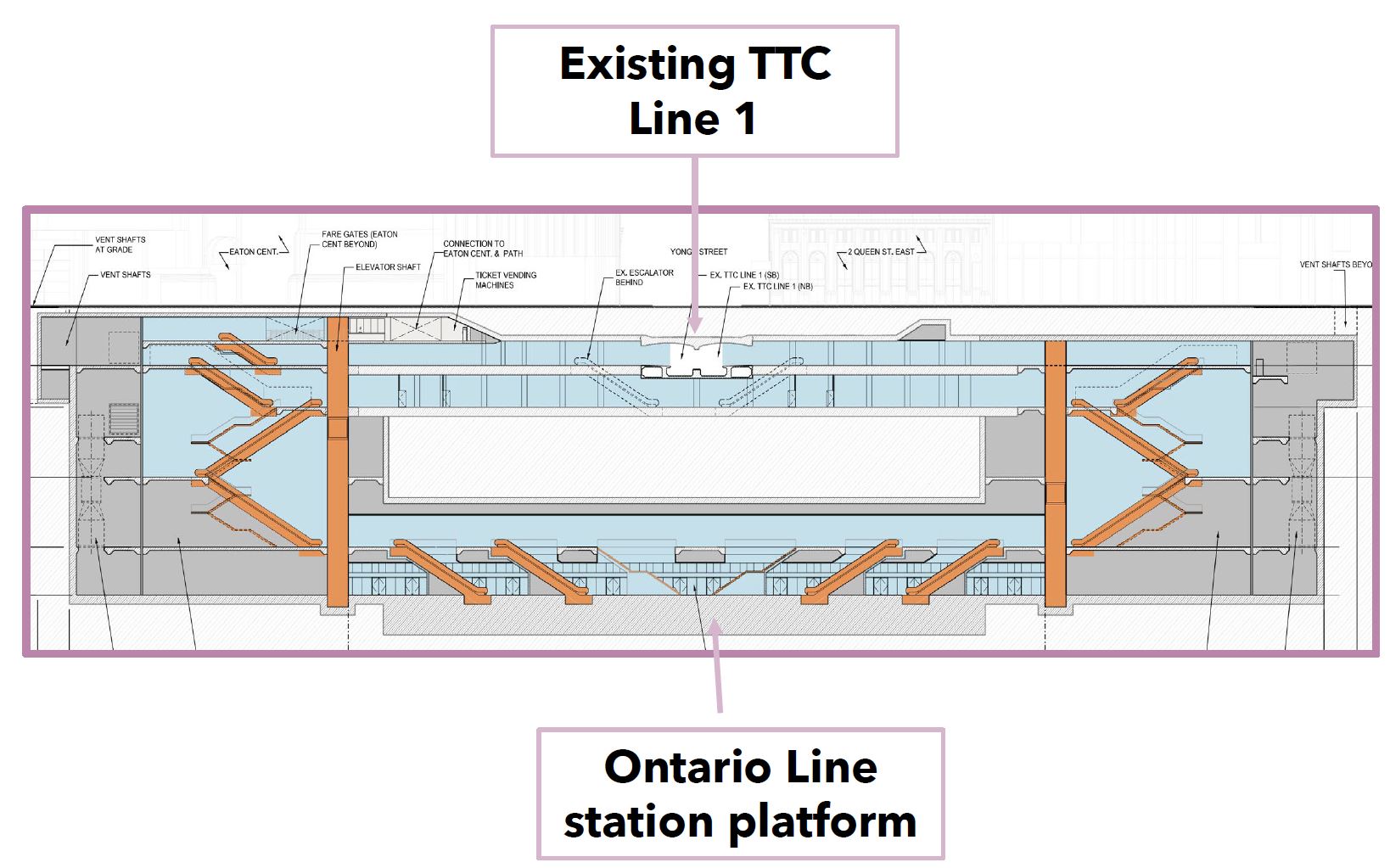

Slide 15: Moss Park/Sherbourne

Moss Park Station will be under the park on north side of Queen west of Sherbourne. No “Transit Oriented Community” development has been proposed here because the lands will remain for parkland and community use. However, redevelopment of the old industrial area has been spreading north from the St. Lawrence neighbourhood toward Queen Street. It would be reasonable to expect land near Moss Park Station to see major changes.

As at Spadina and University Avenues, construction of this station will not interrupt operation of the streetcar services on Queen.

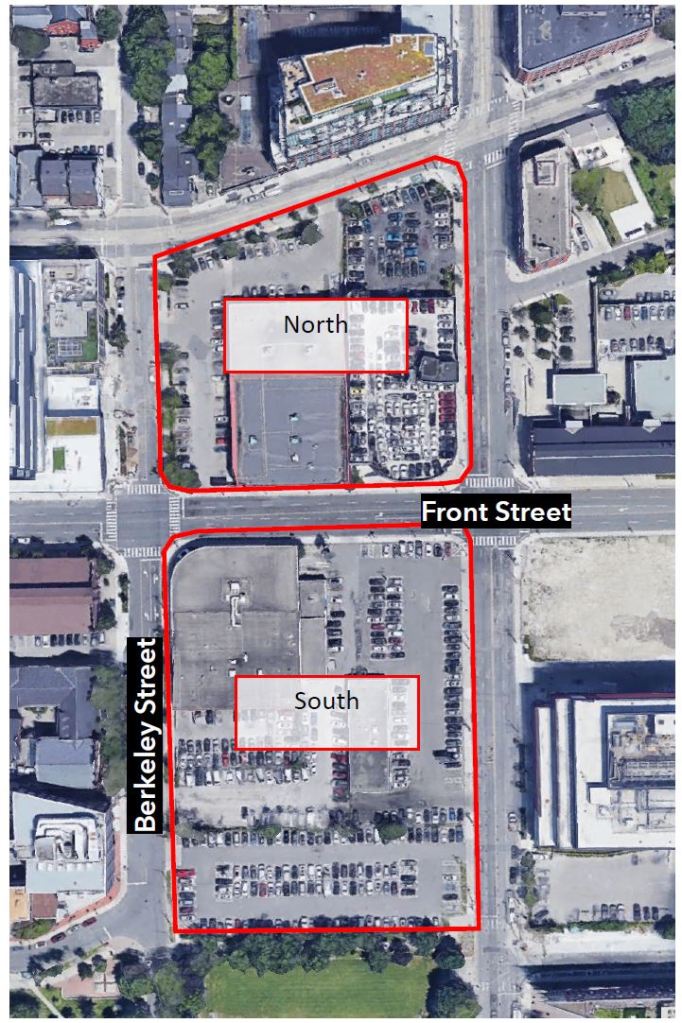

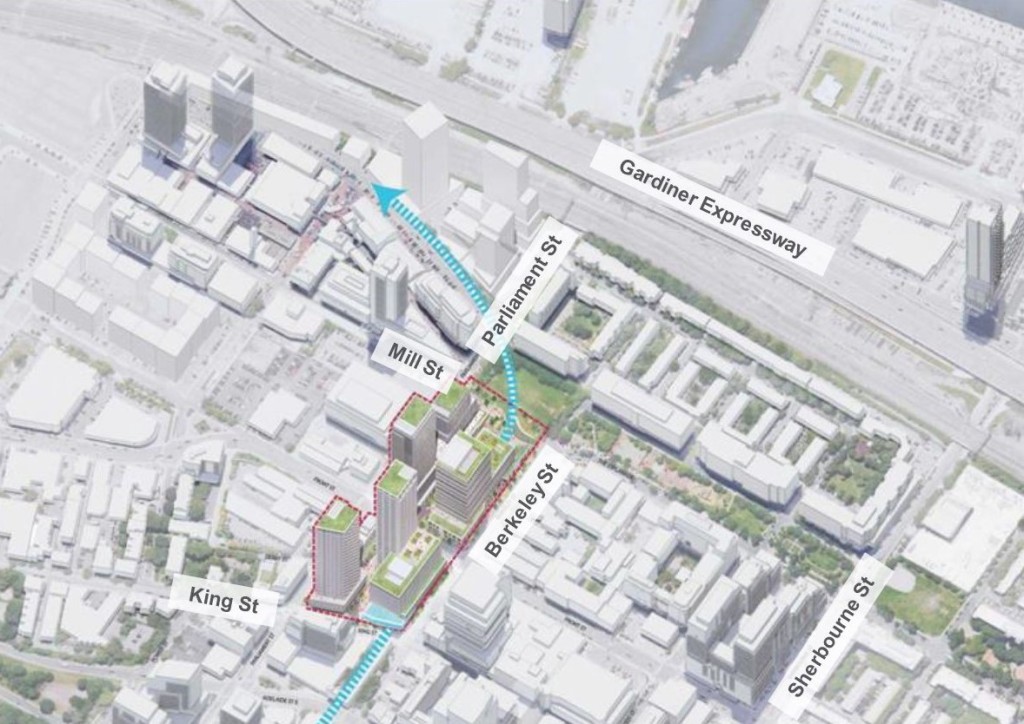

Slide 16: Corktown

From Moss Park to Corktown Station the OL turns south to run between Parliament and Berkeley Street. The north block from King to Front will have the station entrance, while the block south of Front will be the tunnel boring launch site. Tunnel boring will proceed north and west from here, as well as for a short tunnel south and east toward the Don River.

The construction will not interfere with the streetcar services running along King Street.

Infrastructure Ontario has major plans for these blocks with five primarily residential towers. This land, the site of the First Parliament of Upper Canada, was originally assembled by the City. Archeological exploration of the site has been underway for a few months.

Proposed: North site: 2x 46 stories; south site: 46+25 storey + 24 storey office

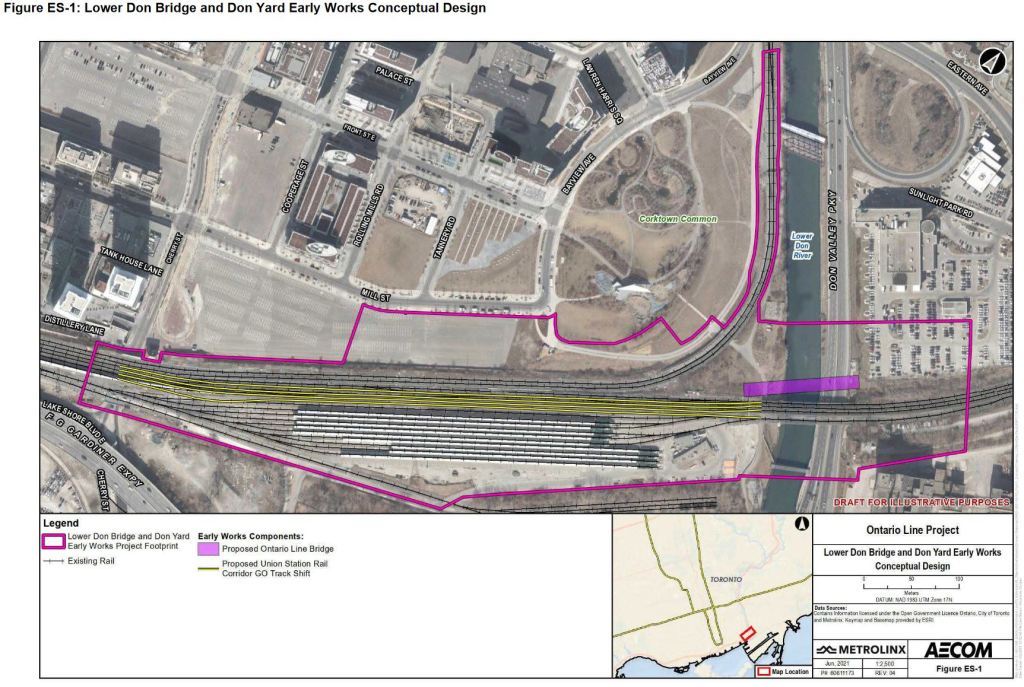

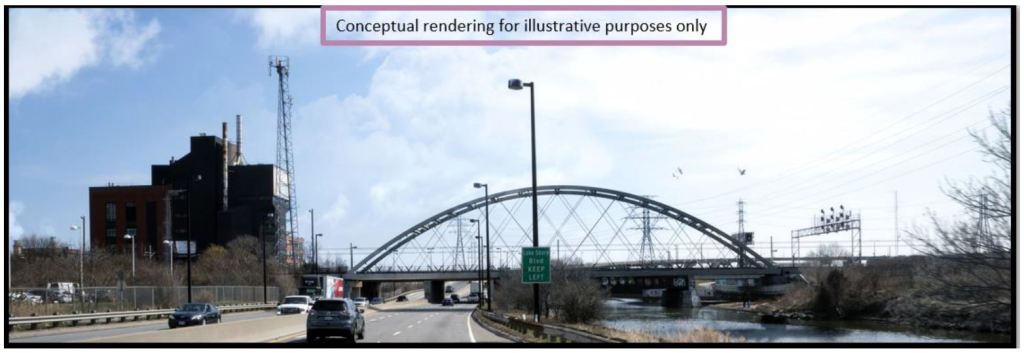

Slide 17: Don River Crossing

The Ontario Line will cross the Don River on a new bridge north of the existing railway line (purple block on the map). There will be adjustments to tracks in the GO Transit yard west of the river so that the Ontario Line can surface in between the main block of tracks in the Lake Shore East corridor and the tracks leading north to the Richmond Hill line.

North of the rail corridor and east of Cherry Street, a new development has been proposed just east of Distillery Loop (lower left corner of the map). This triggered recent debate on Twitter about a possible Cherry Station on the Ontario Line to directly serve the Distillery District. Such a change in the design is quite unlikely given the advanced state of the South Civils procurement. Ideally, if there were to be a station here, the excavation should be done concurrently with the adjacent development.

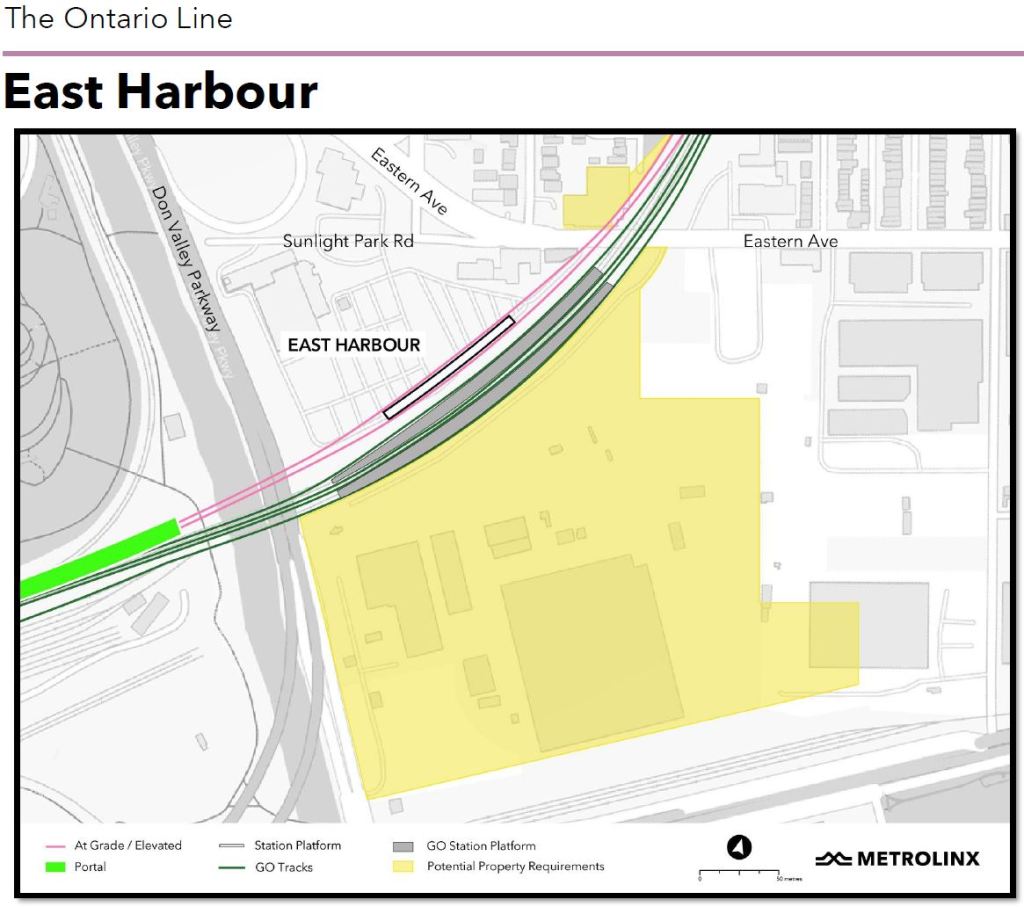

Slide 18: East Harbour Station

East Harbour (the old Lever Brothers site) will see major development in coming years. This was originally a Great Gulf project, and it has been taken over by Cadillac-Fairview. All of the proposed new buildings are south of the rail corridor, and they range from the mid-30s to over 50 stories in height. The full plan envisions about 302k sq m of residential space and 926k sq m of commercial. One obvious issue here will be the staging of residential versus commercial space, and the market for either of them in coming years.

An MZO is expected in Spring 2022 to enable this development.

Slide 19: East Harbour and Environs

There is a Transit Hub at East Harbour that will include a new GO station, the Ontario Line and the planned extension of Broadview Avenue including streetcar service.

The original design had the OL straddle the GO platforms to permit across-the-platform transfers, but as at Exhibition this turned out to be impractical. Now the OL tracks are on the north, GO to the south, and transfers via a concourse below.

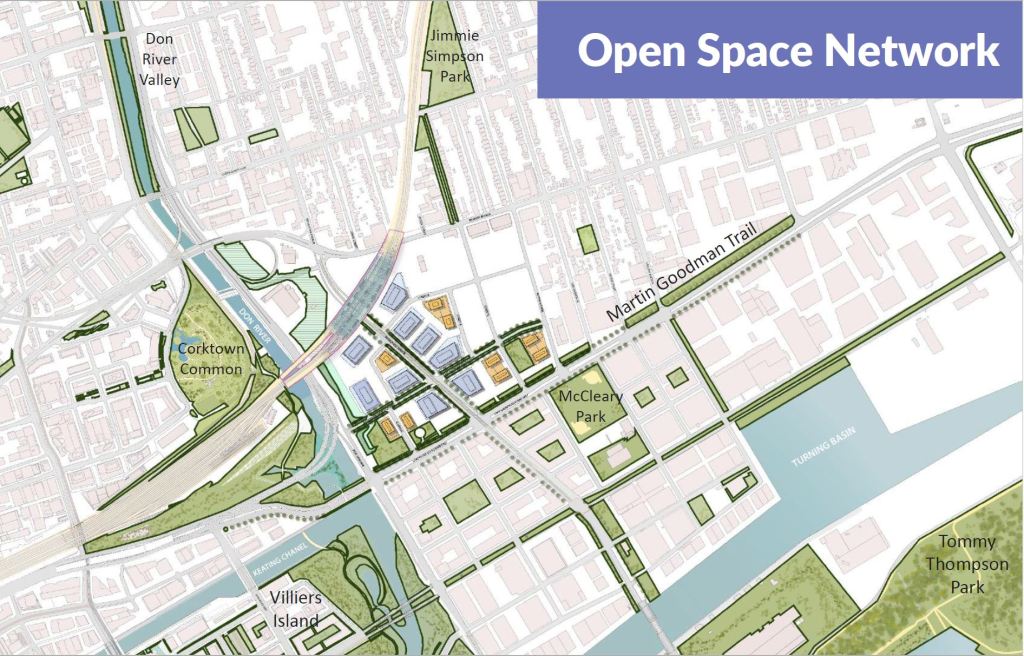

I have also included a wider view of the area in the Open Space overview from the CF proposal to show how this relates to other pending changes including the Broadview Extension, the Don Mouth reconstruction, Villiers Island and the development blocks along the north side of the Keating Channel. Road layouts include the revised Gardiner/DVP connection, and realignments of Queens Quay, Lake Shore Boulevard and Cherry Street. Any discussion of this area should be in the context of plans that have been underway for several years, not on the current layout.

Additional transit changes here include the Waterfront East LRT extension (more details of which are expected to come to Council soon), the Cherry Street connection and the Broadview Avenue connection. Although eventually there could be a link east via Commissioners from Cherry to Leslie Barns, that is in the distant future.

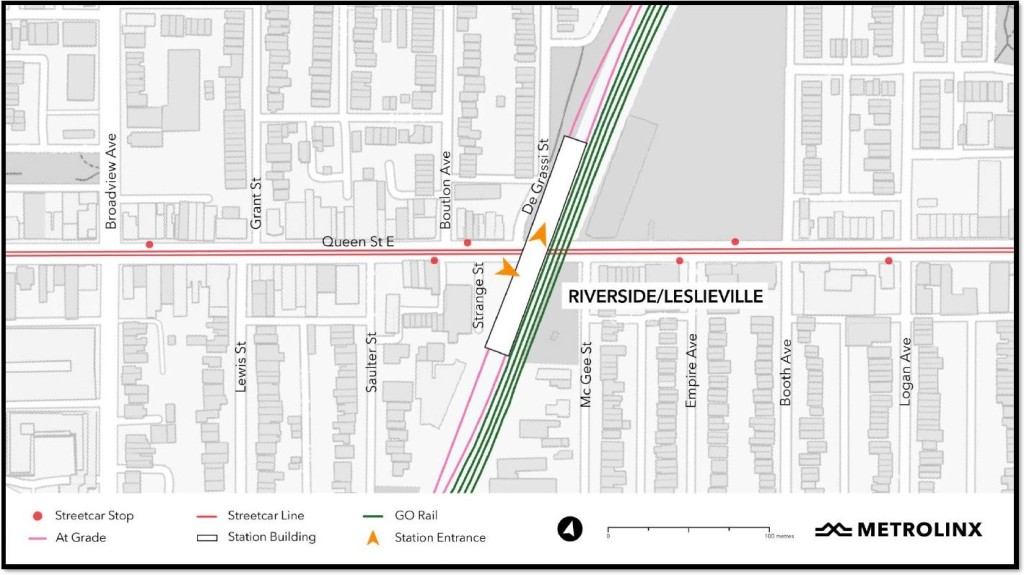

Slides 20: Riverside/Leslieville

The station at Queen was misnamed “Leslieville” by Metrolinx, even though it is actually located in Riverside, a name that is over a century old. These stations are on the Joint GO/OL corridor and some of the design issues are complicated by shoe horning six tracks of transit into the available space.

No TOC development is proposed for Riverside Station, although it is self-evident that there will be development pressure nearby.

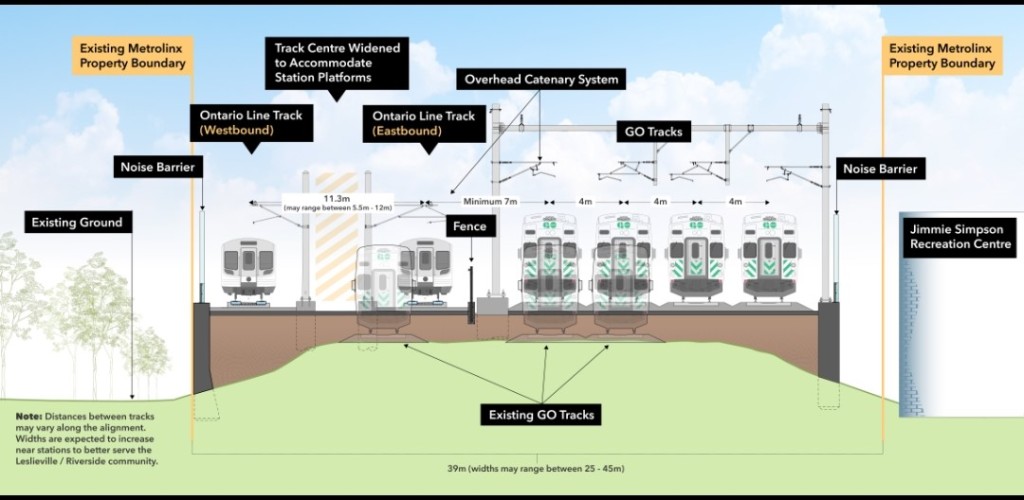

Slide 21: Joint Corridor

From East Harbour to Gerrard, the OL shares the existing GO corridor. There are now 3 tracks, but this will be expanded to 6 completely filling existing Metrolinx right-of-way.

- The corridor will be raised by up to 1.5m with 4 new bridges that will provide 5m clearance for large vehicles.

- Berm construction will be replaced by retaining walls.

- All vegetation will be removed within the corridor and some adjacent lands due to clearance needed for electrification.

Metrolinx trumpets the expansion of parkland along the corridor. What they do not mention is that the percentage change in space is relatively small, and there is no guarantee that areas along the rail corridor berm that are now treed will be replaced in kind in the same location.

Full disclosure: I have worked with community groups in this area on a proposal for an alternative “hybrid” route using Metrolinx’ OL design west of East Harbour Station and the original RL design to the east and north. Metrolinx examined, but did not accept this design.

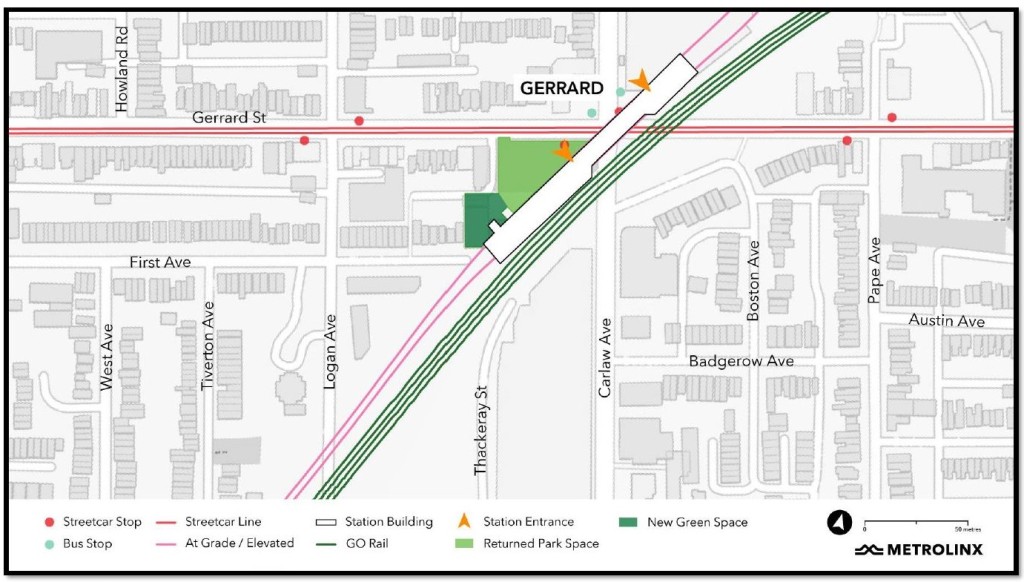

Slide 22: Gerrard

At Gerrard, there is a large commercial property at Gerrard Square east of the station. Again, it is not flagged as a TOC because this is not provincially owned, but it is an obvious location for intensification.

Northeast of Gerrard Station, the OL dives back underground for its trip north on Pape.

At one point, there was a proposal for a new GO/SmartTrack station here, but it would fit with the Ontario Line and has been dropped.

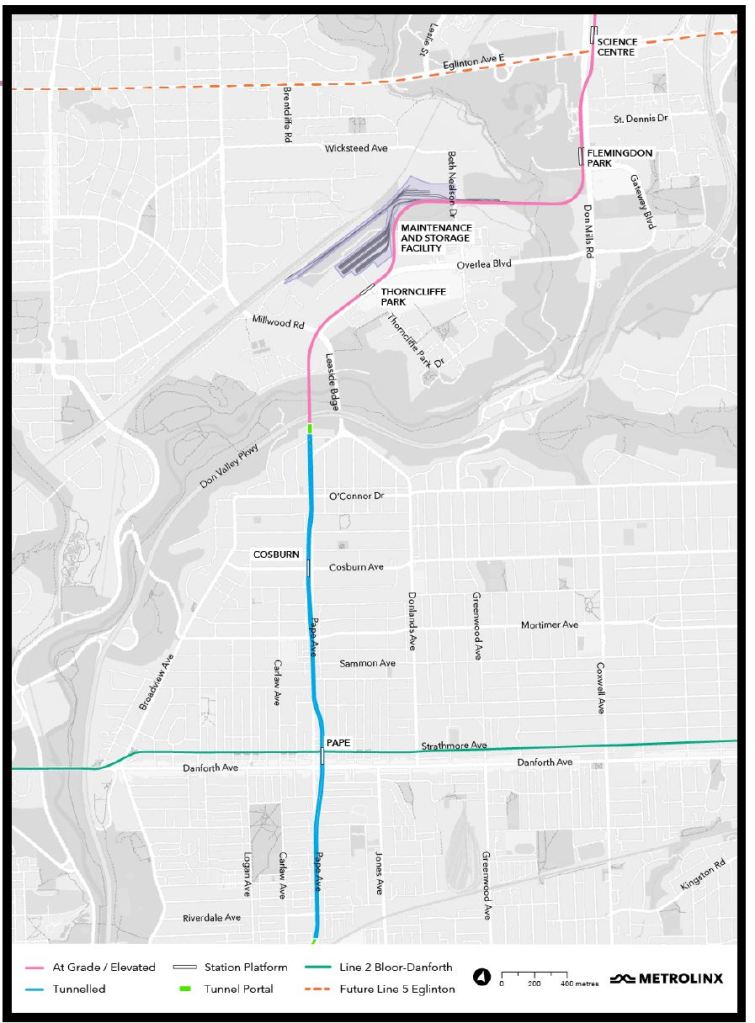

Slide 23: Northern Alignment & Danforth Pape

Much less detailed info available so far on this segment of the line. It comes north up Pape, dodges slightly to the east for the station at Danforth (a change from the original plan), and slightly to the west for the station at Cosburn (again a change from the original). There are no illustrations yet published by Metrolinx of how these stations will work, and especially how or if the interchange with the Danforth subway will make for easy transfers between the two lines.

There is no TOC proposed for Pape/Danforth, but this has been flagged by City Planning for intensification as an MTSA.

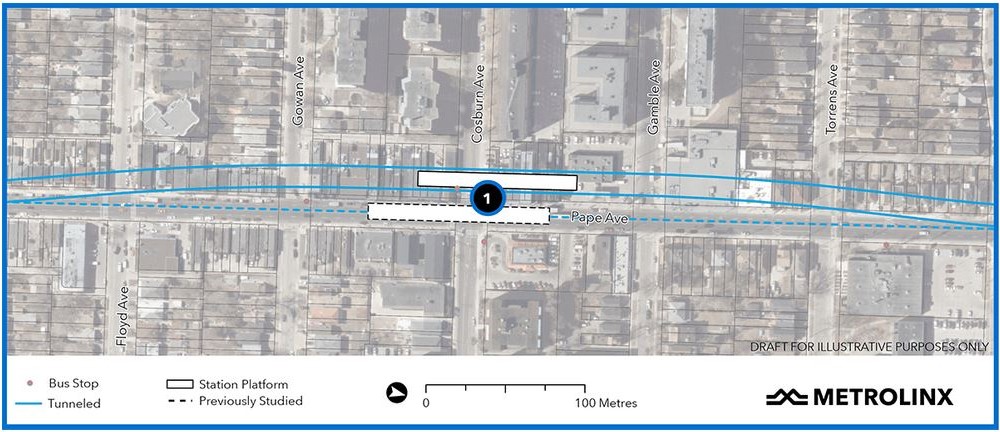

Slide 24: Cosburn Station

The station at Cosburn will be on the west side of Pape where there is now a collection of smaller commercial/residential buildings. The originally proposed location was under Pape Avenue.

West of the station to Broadview is a high rise apartment district. To the east is single family housing.

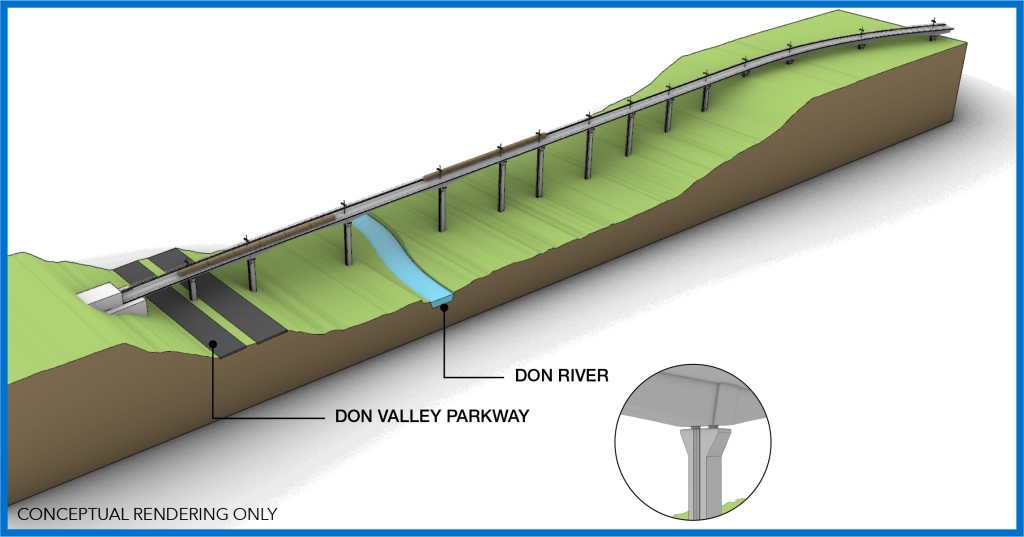

Slide 25: Minton Place / Don Valley Crossing

The OL runs straight north on the line of Pape via Minton Place. Four houses will be taken for the portal construction site (green above).

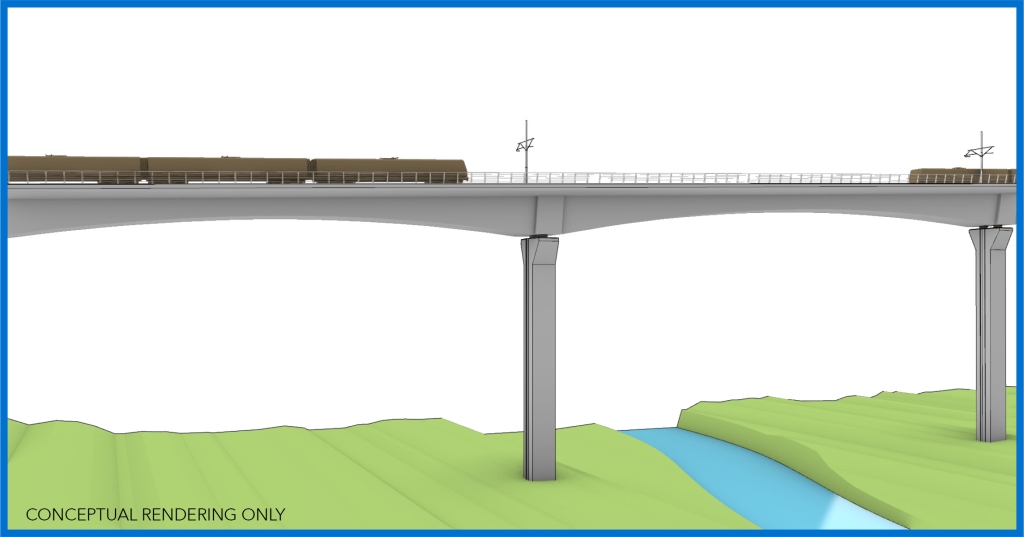

It will cross the Don Valley on a new bridge west of the existing Leaside bridge.

Note that a route following the road and using the existing bridge is not practical. There are structural issues with the bridge (it was not designed for a lower deck like the PEV, and added strength included originally for a streetcar line in the 1920s was used up when the bridge was widened to six lanes) and the curves approaching the bridge at both ends would be too tight.

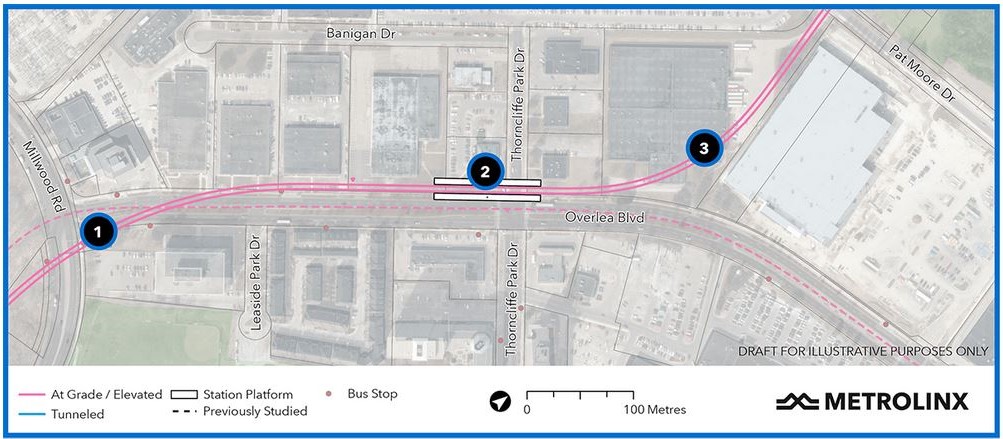

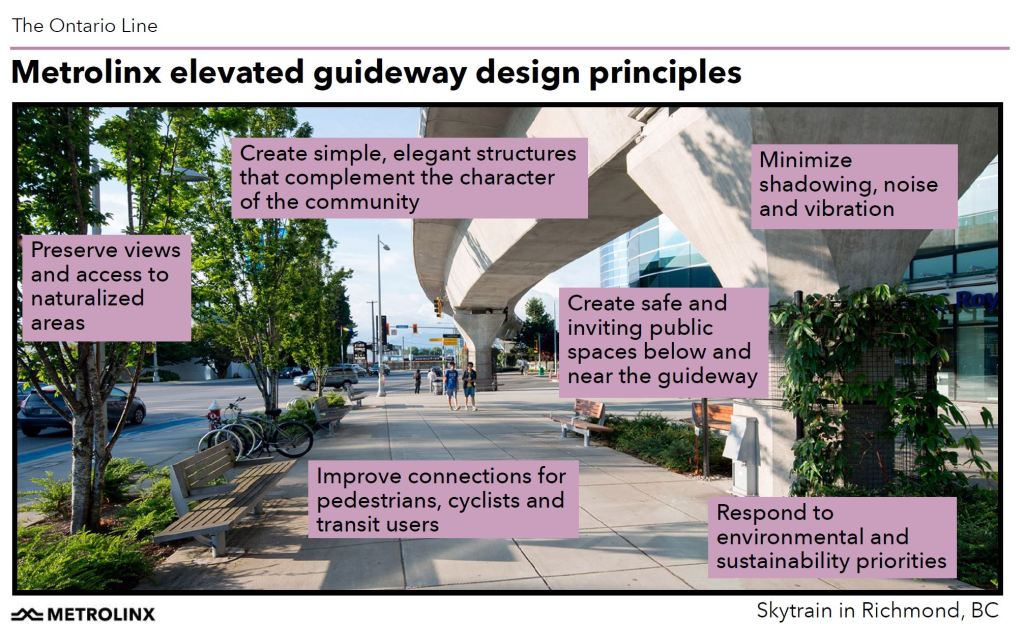

Slide 26: Thorncliffe Park / Overlea:

After crossing the valley, the OL turns east on an elevated structure on the north side of Overlea to Thorncliffe Park Drive West with a station on the northwest corner. The line then turns north to access a new maintenance yard south of the CPR tracks that divide Thorncliffe Park from Leaside. (The large building and parking lot on the right side of this image is Costco.)

The originally proposed alignment followed the middle of Overlea Boulevard and turned north at Don Mills Road.

Metrolinx uses an illustration of the Vancouver Skytrain to show what the elevated structure will look like. This is not an entirely fair presentation because it does not include the space required for station platforms and vertical access from the street. It also does not show the specific relationship of the proposed structure with buildings that it will pass along its route and how open, or not, the space under the structure will feel.

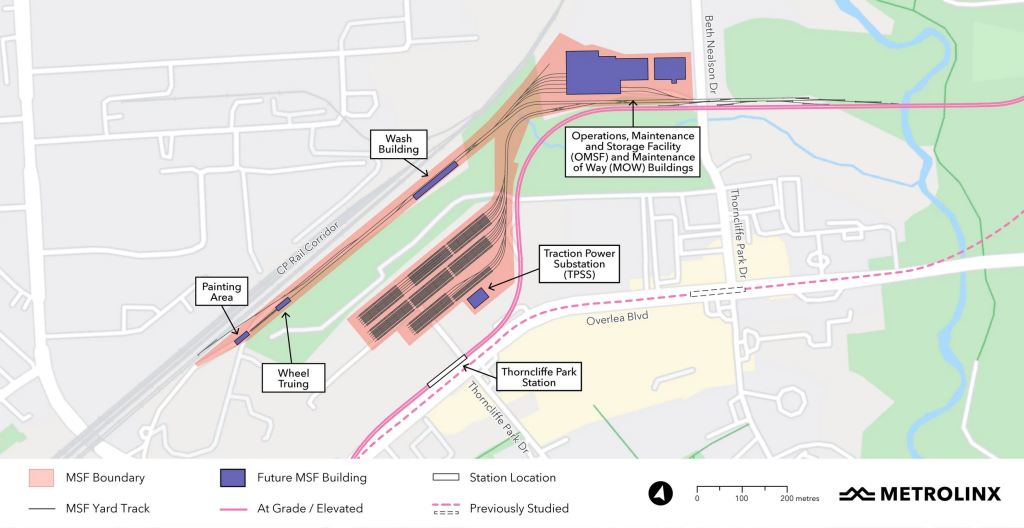

Slide 27: Maintenance and Storage Facility (MSF)

The proposed Maintenance and Storage Facility will be located at the north side of Thorncliffe Park on lands that are now occupied by a self-storage facility, a low-rise business park, and a mosque.

The MSF has two sections. At the north are the buildings where trains will be maintained, and to the south is the storage yard for trains. This is sized to support an eventual full build-out of service to its maximum capacity.

The mosque will relocate to land west of the proposed Thorncliffe Park Station and will be part of a community centre into which some of the existing businesses might also locate. It is not clear yet how well this has addressed business and community concerns, although Metrolinx speaks of the situation as effectively a done deal.

Among the community’s suggestions was to shift the yard portion of the MSF to the north side of the CPR corridor, but Metrolinx rejected this saying the site had already been rejected due to employment effects. They neglected to mention that only shifting the yard would not have required the entire site. (Full disclosure: I advised some members of the community on the viability of optional locations.)

Metrolinx community relations on this site were a textbook example of how to antagonize people about a project. If, instead of a secret plan for the MSF dropped on the community and businesses at the last moment, Metrolinx had truly engaged and worked through alternative plans up front, much of the contention might have been avoided.

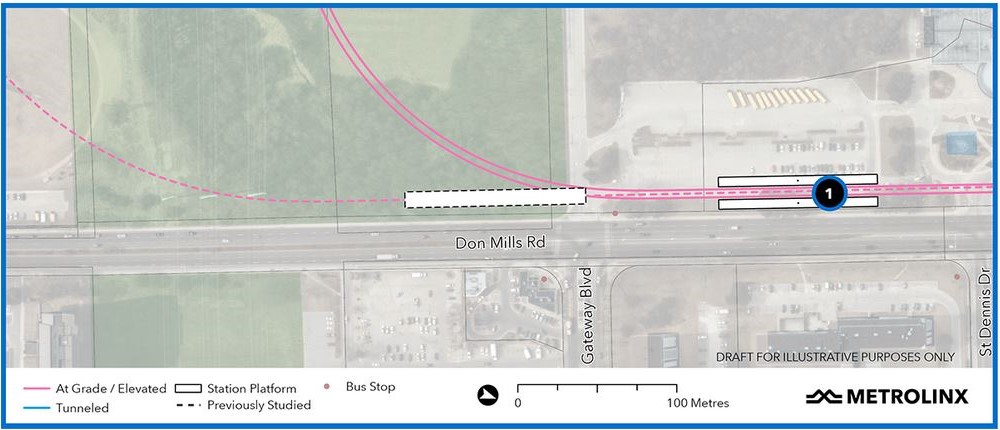

Slide 28: Flemingdon Park

Flemingdon Park Station is a “local” station for walk-out traffic from the neighbourhood to the east. A large part of this area will remain beyond easy walking distance, and a good transit link will remain essential especially for residents east of the DVP. They are more likely to be fed into Science Centre Station where there is a bus interchange.

An intriguing problem with redevelopment pressure faces the midrise areas of Flemingdon and Thorncliffe Parks. Will these areas remain affordable, or will they be replaced with larger form, expensive condos now that there is a subway station just down the street? The intensification goals of MTSAs and transit oriented communities could have unwanted consequences. A discussion of the potential effects, good and bad, of MTSAs is probably a webinar in its own right.

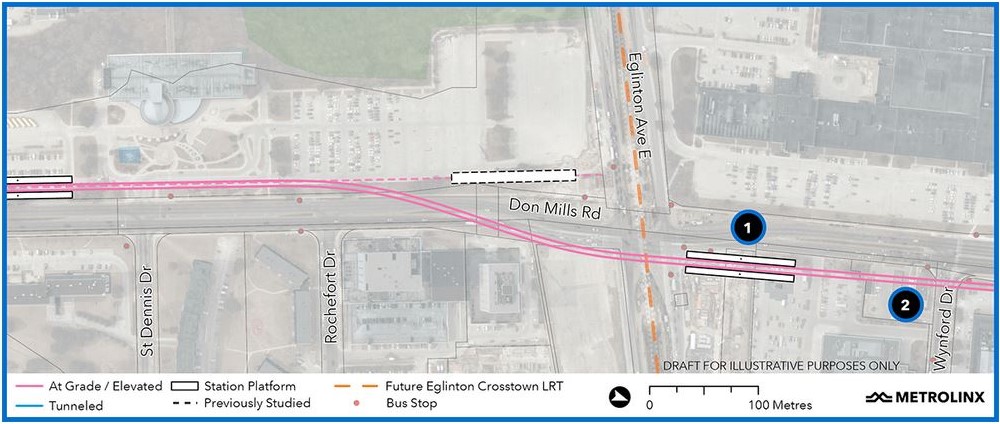

Slide 29: Science Centre Station

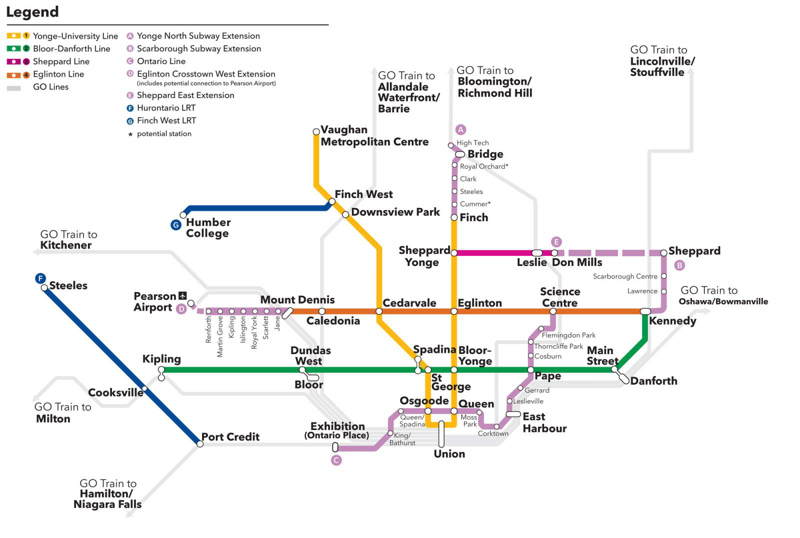

Science Centre Station already exists as part of Line 5 Crosstown which will open sometime in the coming year. There is a bus loop on the northeast corner. Transfers from the OL to buses will be simple, but to the Crosstown somewhat longer because of the relative location of the two stations.

Although the image shows no development here, large schemes are in the works. This is a “before” view that is already out of date.

The OL station was originally to be on the SW corner, but it has been relocated to the NE corner above the bus loop for a more convenient transfer. This also positions it for a northward extension as shown on the map.

Slide 30: Science Centre Station Development

Updated February 2, 2022

There is a 60.5 acre / 24.5 hectare development underway on the northwest corner, the former IBM/Celestica site. The other corners will not stay long as they are.

On the SW and SE corners, CreateTO plans a development including a new school. The view below looks southwest across the intersection. The Ontario Line guideway crosses Don Mills south of Eglinton to the station on the northeast corner (bottom centre).

That corner remains without a development proposal, but the land north of the station is a Superstore, and Loblaws/Choice REIT have been redeveloping their properties.

[End of update]

This station shows the limits of walking distances given the large existing and planned communities around it. Bus feeders will be vital to link areas around the intersection to this major transit junction.

Another important consideration here is the change in neighbourhood makeup the new rapid transit lines will bring.

Slide 31: Planning Issues

In a broader context than individual stations, there are a few issues I wanted to mention:

- Just what “relief” does the Ontario Line provide?

- A contrarian’s view of “Transit Oriented Communities”

- Catchment areas and Liberty Village

- Gentrification

Slide 32: Union Relief

The OL descended from the concept of subway relief, but it has developed an alternate justification: the relief of potential GO Transit overcrowding at Union Station. Metrolinx hopes to divert inbound riders onto the OL at East Harbour and Exhibition from GO.

Convenient transfer connections and an attractive fare structure are vital to making this work. Indeed, this idea drove the original straddle design with OL tracks on either side of the GO corridor for across-the-platform transfers. That would have limited GO trains to stopping only on the outside pair of tracks (in effect, only the “local” and not the “express” trains). The revised plan uses a concourse serving all tracks, and it turns out to be cheaper to build.

Metrolinx always talks of this diversion in terms of inbound riders, but has not addressed outbound travel. Boarding a GO train one station away from Union is analogous to boarding an outbound Bloor-Danforth train at Sherbourne or Bay when it is already filled with riders from Yonge Station.

This all begs the question of how much of the OL capacity will be consumed simply to act as a relief valve for a short distance either side of Union as opposed to its wider role in the transit network.

Slide 33: “Transit Oriented Communities”

I will take a contrarian view here and argue that simply placing dense development at rapid transit stations is not sufficient or even necessary to the success of a rapid transit line.

Two important factors affect demand.

(1) For locally originating trips, how easy is the walk to the station? Are there competing transit services or highways in the same general area? Does using the rapid transit line impose time penalties just to reach the station or to make a new transfer connection enroute?

(2) Trips can access a rapid transit station by feeder routes, and indeed it is no secret that the Danforth Subway was full in pre-pandemic times even though the built form along it is low rise. Where do these riders come from? Feeder bus routes especially on the outer end of the line.

Density does not equal demand unless the rapid transit line actually serves trips where people want to travel.

For GO Transit, this is relatively easy because they have (or had) a built in market wanting to get from their homes in the 905 to Toronto’s downtown. The railway network is ideally suited for that. However, travel to other parts of Toronto and the GTHA is much more challenging.

Rapid transit extensions have been less successful because their purpose was to generate development, no to react to a large existing demand. Only the proposed North Yonge extension to Richmond Hill lies in a long-established corridor. Demand has materialized much more slowly on the Spadina/Vaughan and Sheppard lines.

It is much harder to attract demand from residential clusters than to job-oriented rapid transit. One has a diverse pattern of origins and destinations that might lie of the transit grid, but equally well is probably better served by the highway network. The other concentrates demand at a node that suits a model of feeders into trunk routes.

The Ontario Line, to its credit, is not an extension of an existing line, but an entirely new addition to the network. As such it will provide many travel options in central Toronto that do not exist today, rather then simply shortening travel for riders in outer areas.

The Transit Oriented Communities component will see major development, mostly residential, around several stations.

Because the whole process of Metrolinx financing is shrouded in secrecy, there is no estimate of how much the transit line’s capital cost will be recouped from these developments, nor whether they will make any ongoing contribution to operating costs.

The province will use MZOs to implement the necessary permissions for these projects, and the City of Toronto has no control over them beyond moral suasion.

Slides 34/35: “Liberty Village” and Catchment Areas

This is a good point to talk about how a local rapid transit station is not the same as a GO station. Access is on foot or by feeder bus. The catchment area is defined by walking distance, local topography and available alternatives.

When we talk about “faster” journeys, this applies to an entire trip, not just to the OL component. If using OL requires a longer access, or extra transfers, riders may not turn up in droves.

A related problem is the planning lens that sees transit stations it terms of a 500-800m catchment area and the planning associated with MTSAs. This ignores the fine grained nature of older parts of the city and alternative transit services in the same area. We see this in several of the stations along the Ontario Line.

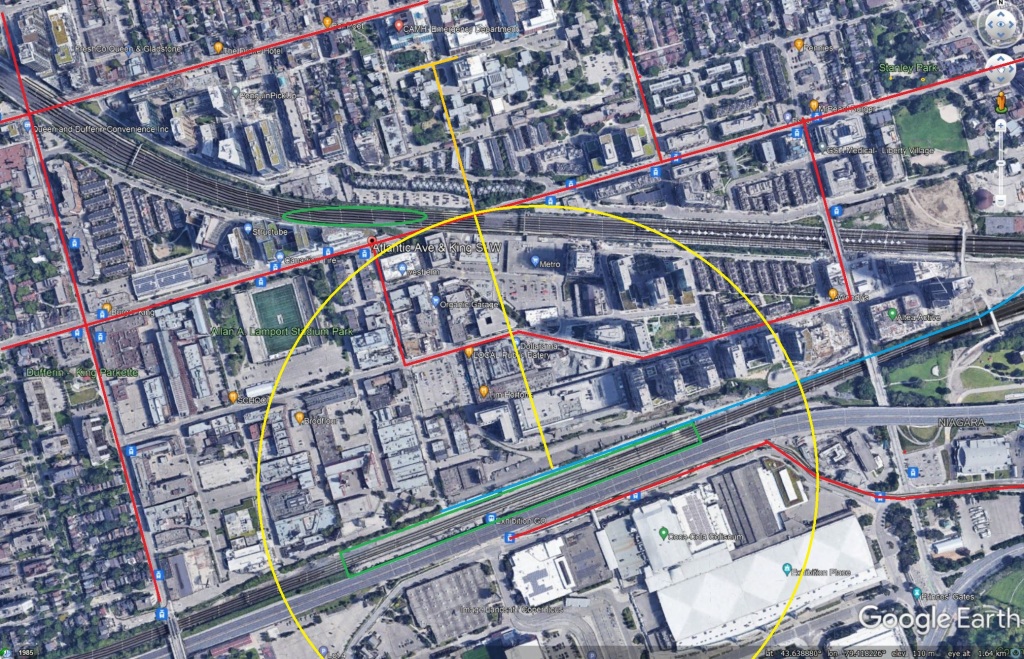

This map spans from the GO corridor at the south with Exhibition Station in the green box. The Ontario line in turquoise is immediately adjacent. TTC services (Harbourfront/Bathurst, King, Queen, Ossington, Dufferin) are shown in red. The green oval is at the future Liberty Village GO station on the Weston corridor.

The yellow circle marks a 500m radius from the station. The orange line extending further north shows the extent of an 800m radius, the “rapid transit” definition for an MTSA. Two issues are evident: (1) much of the developed area is outside of the 500m radius because the station is at the edge, not the centre of the development, (2) half of the circle lies south of the corridor where nobody lives. TTC services, and another GO station, will compete for riders.

Most other stations do not have the “half a circle” problem of geometry, but these circles do overlap as shown on the graphic for this webinar at the top of the article. This is rarely a problem for commuter rail stations, but planning for them and for local transit are two quite different matters.

Slide 36: Gentrification

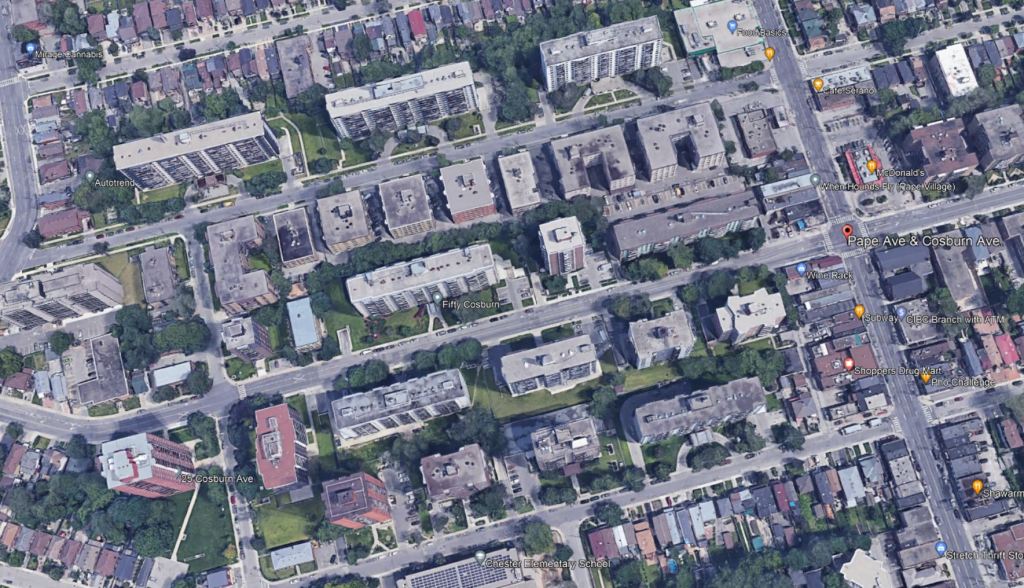

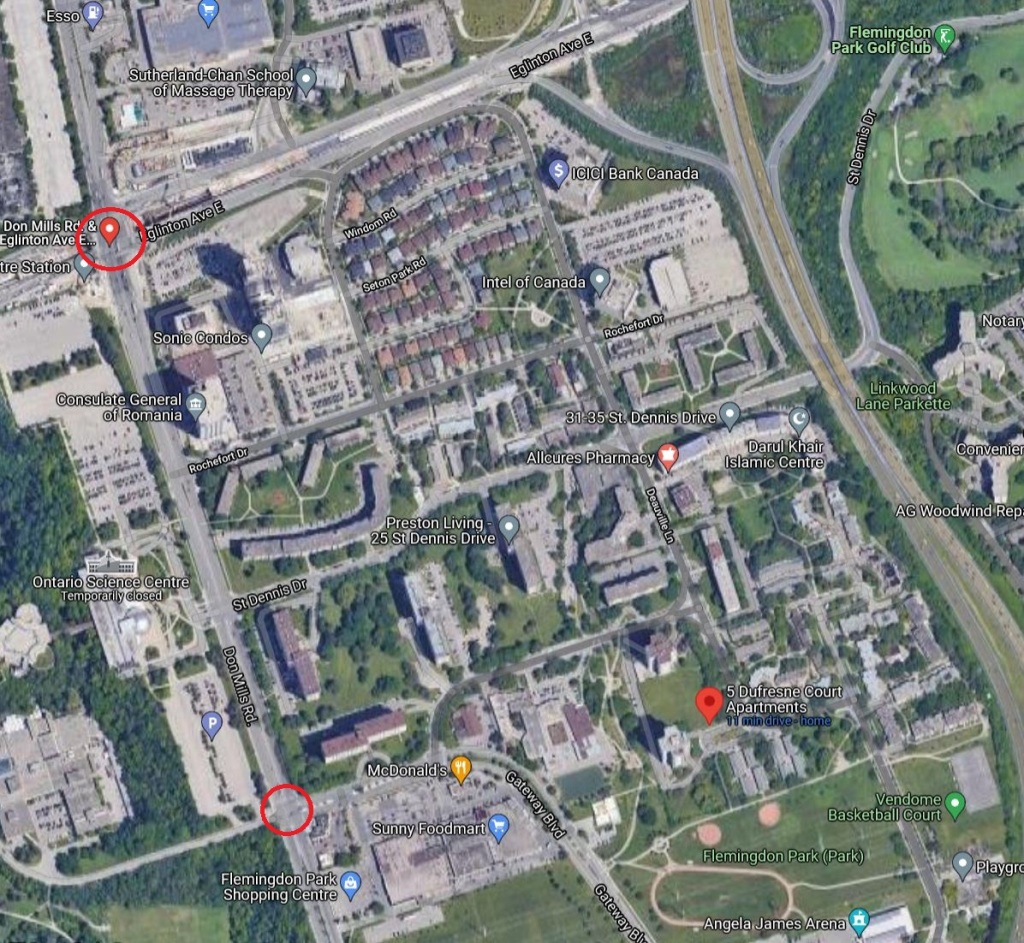

A side effect of rapid transit construction and the provincial mandate for greater development density near transit stations is that many existing neighbourhoods will be targets for new development. A particular example is the western part of Flemingdon Park.

Unlike Liberty Village which was an old, underused industrial district, Flemingdon Park is a large, existing residential neighbourhood.

The photo shows the area between Don Mills and the DVP from Eglinton south to the Hydro corridor. Two thirds of this (the portion to Deauville Lane) is within 500m of either Science Centre and Flemingdon Park Stations (red circles). If we expand the reach to 800m, everything to the DVP is included.

Many of the buildings here are low-rise rentals, and already there are condo development proposals that will affect these units.

Gentrification of areas around transit stations will be a pervasive part of our transit plans in coming decades, but this will do little for the cause of affordable housing and could, in some cases, worsen the situation.

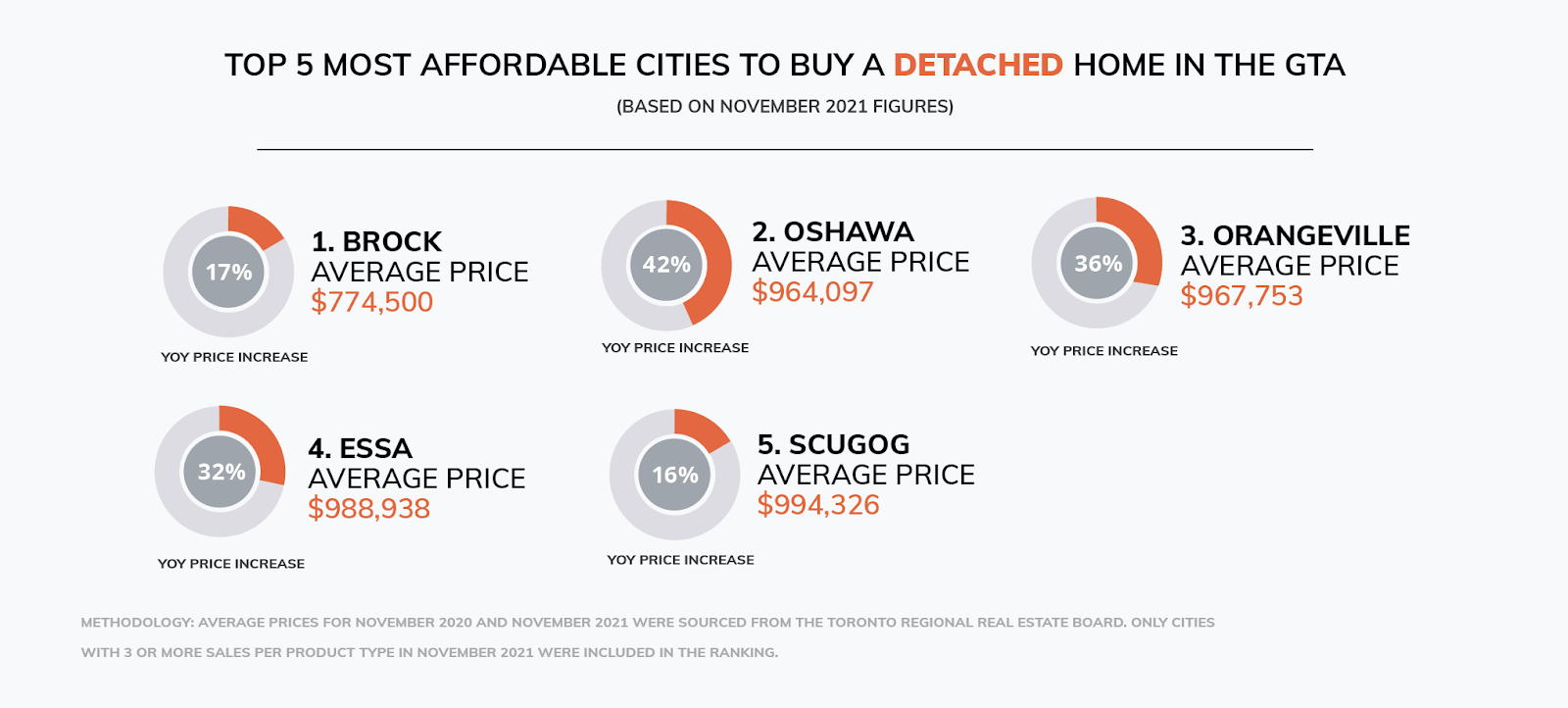

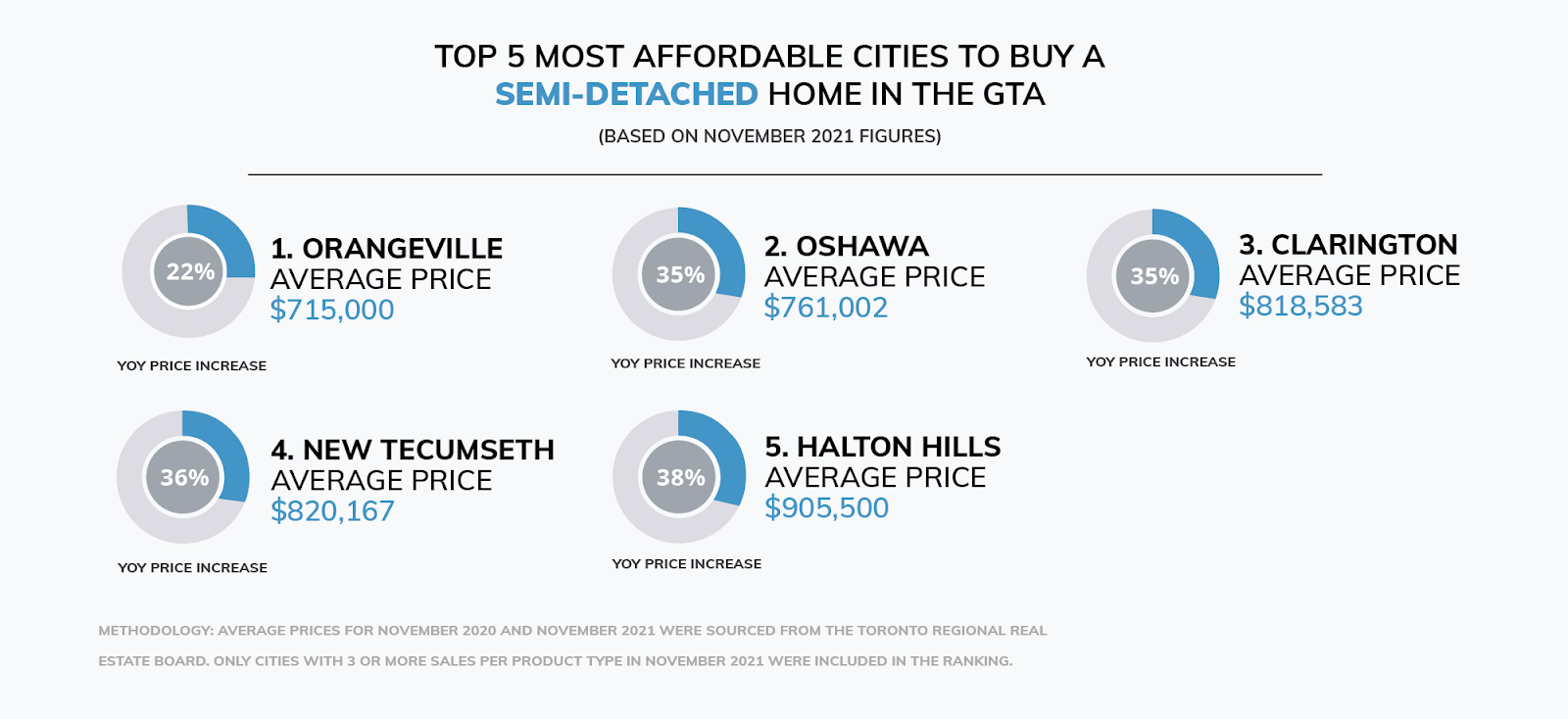

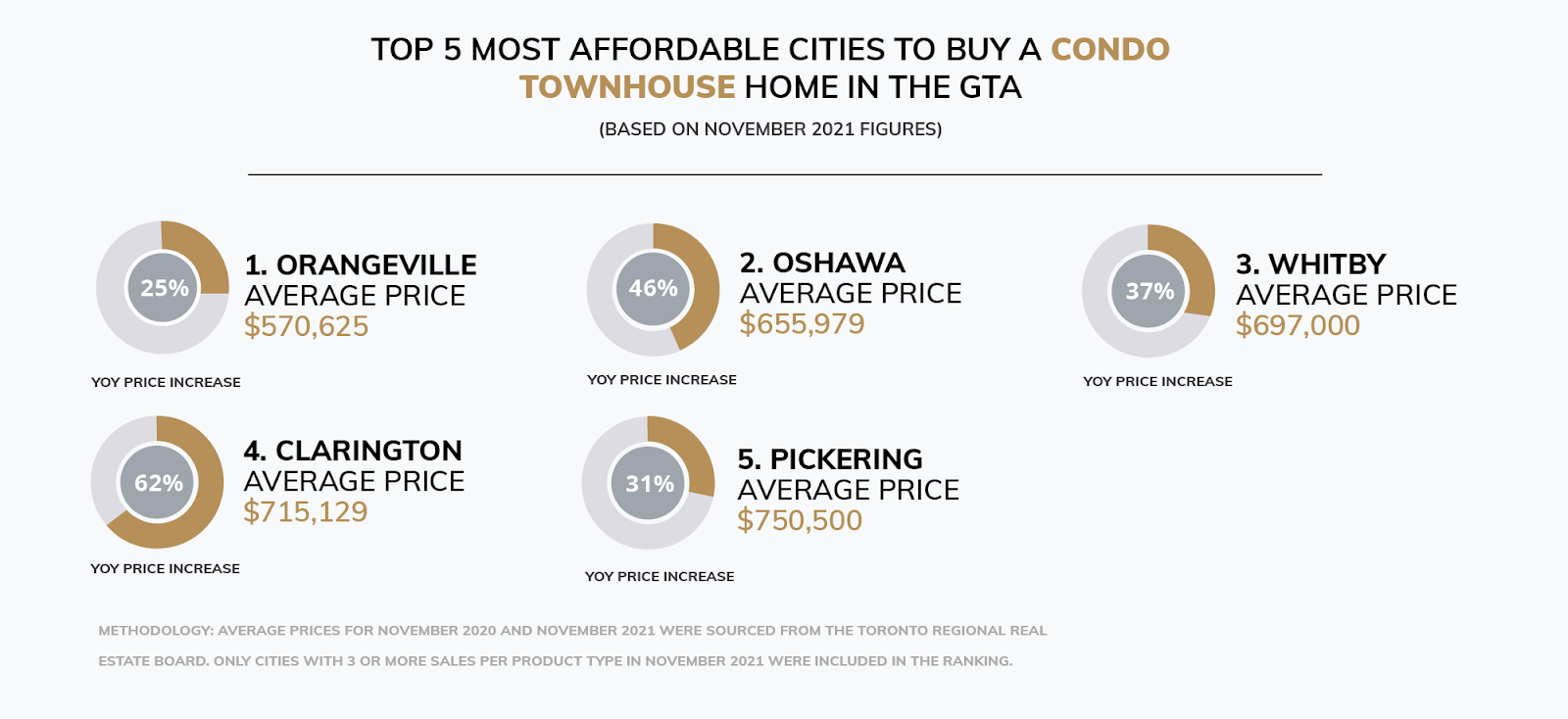

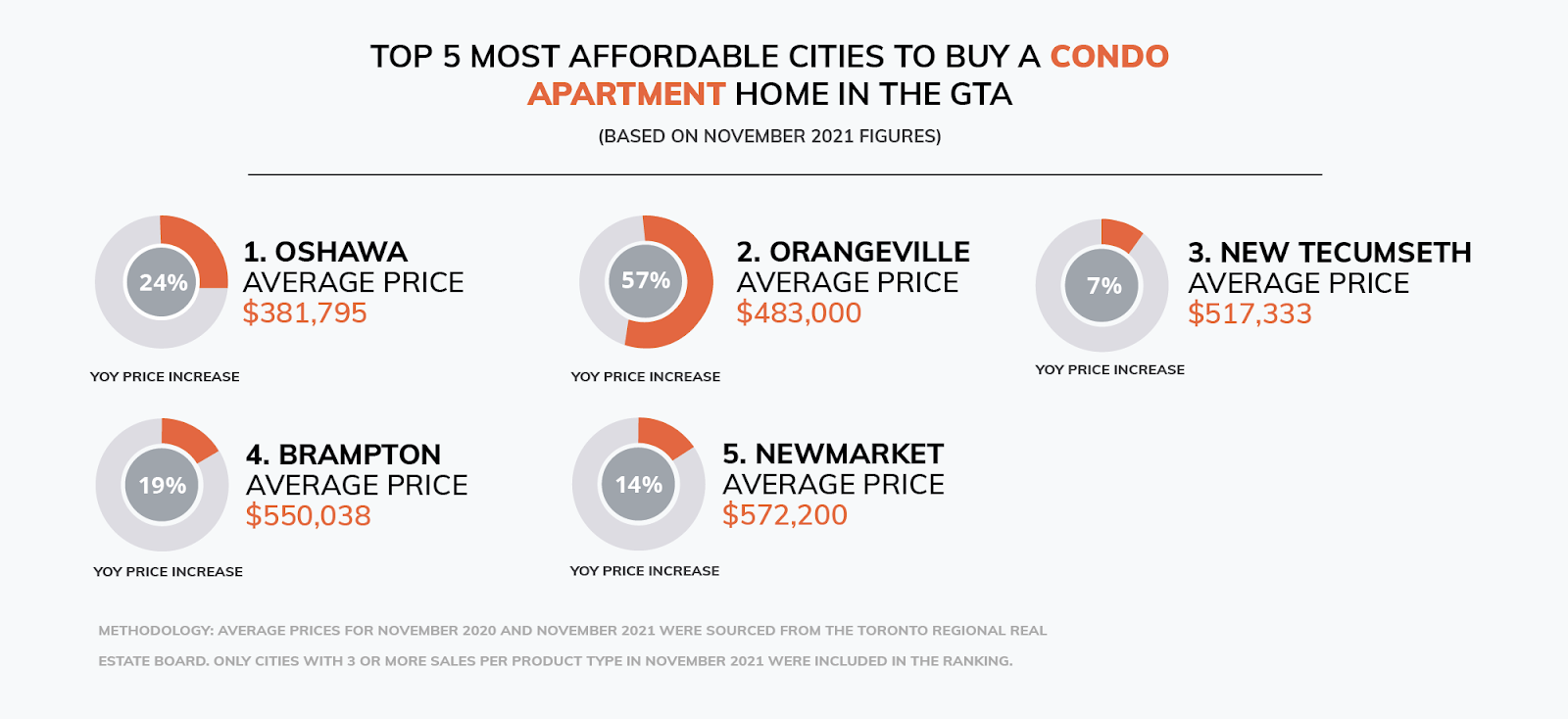

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2