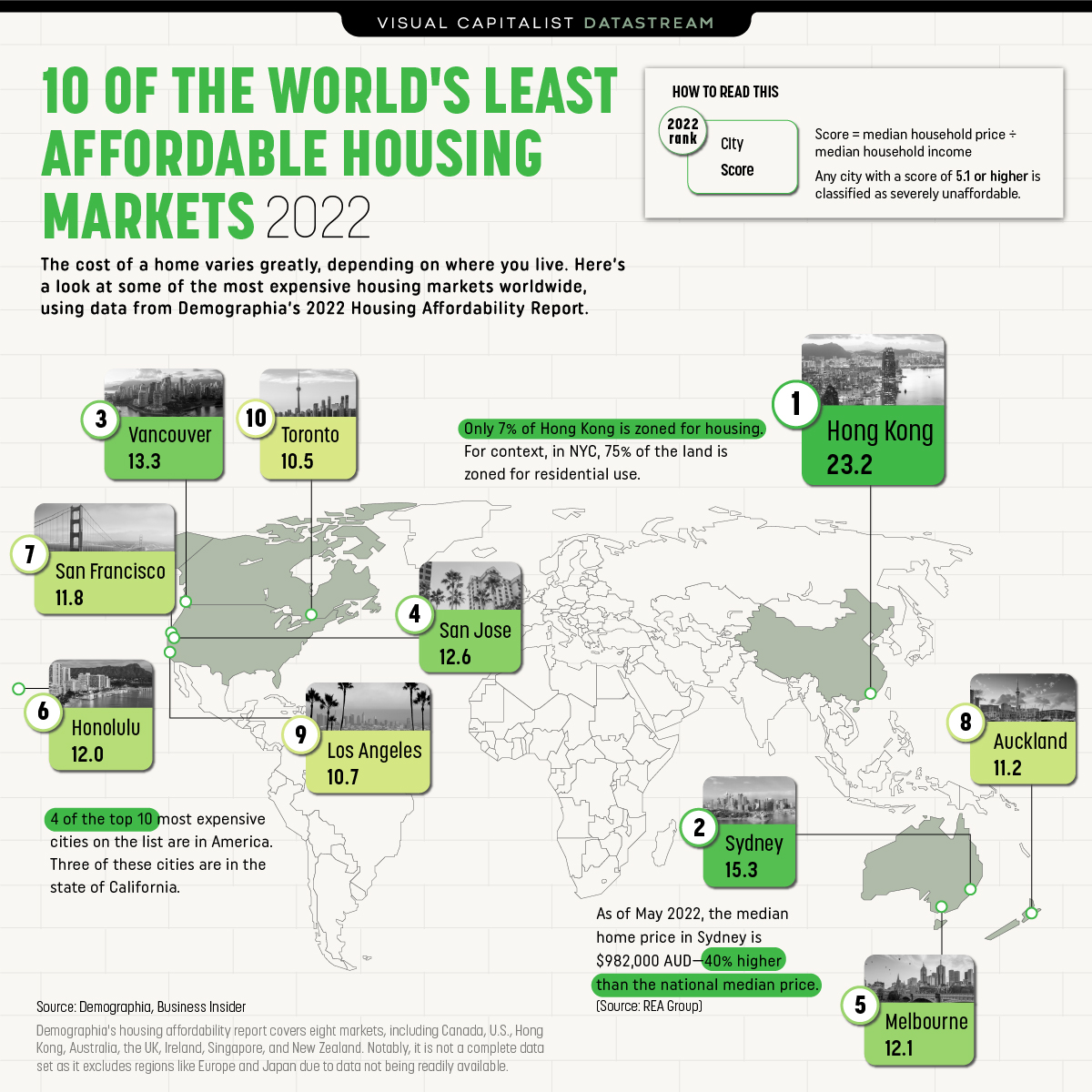

Survey Highlights

- Nearly half (47%) of urban Canadian Generation Z adults rank proximity to their workplace as a top priority for the location of their first home purchase; however, just 15% indicate that buying in or close to the downtown core is a priority.

- 40% plan to purchase their first home in a major city, while 42% plan to buy in a suburb outside of a major city. 7% expect to buy their first home in a small town and 3% expect to do so in a rural area.

- 48% of Calgary’s Generation Z adults plan to buy their first home in a major city, surpassing those who plan to do so in Toronto (37%) and Vancouver (36%).

- 7 in 10 (73%) of Canada’s urban Generation Z adults plan to buy their first home in their current city of residence or within a one-hour drive, with 41% of all respondents planning to buy their first home in their current city and 32% planning to buy within a one-hour drive of their current city.

TORONTO, June 01, 2022 (GLOBE NEWSWIRE) — As employees and employers negotiate new possibilities for remote and hybrid work as the COVID-19 pandemic evolves, a newly released generational trends report by Mustel Group and Sotheby’s International Realty Canada highlights new insights revealing that future housing demand will be underpinned by an expectation for a return to the workplace and office, as well as a balanced preference for urban and suburban living amongst Generation Z home buyers.

Newly released Mustel Group/Sotheby’s International Realty Canada survey results reveal that nearly half (47%) of urban Generation Z adults in Canada’s largest metropolitan areas rank buying a home “close to work” as being a top priority for the location of their first home purchase, although just 15% indicate that purchasing in or close to a downtown core is a priority. Proximity to work is surpassed only by neighbourhood safety as a key location characteristic, with safety being cited by 56% of survey respondents overall. Other priorities for a first home locale include proximity to a grocery store (39%), transit friendliness (36%), living close to family (35%) and walkability (34%). According to survey results, the lowest neighbourhood priorities for a home purchase are cycling friendliness, cited by 8% as a key factor, and living near nightlife such as clubs and bars, reported by 5%.

Survey findings also reveal an almost even distribution between urban Generation Z adults who plan to purchase their first home in a major city, reported by 40%, and those who plan to buy in a suburb outside a major city reported 42%. Approximately one in 10 expect to buy their first home in a small town (7%) or rural area (3%). 8% remain undecided as to the community type of their first home.

Furthermore, survey results reveal a preference for urban Generation Z first-time buyers to remain in or close to their current cities of residence. 41% plan to purchase their first home in their current city of residence while 32% plan to buy within a one-hour drive of their current city. A further 11% plan to buy further afield but within Canada; this includes 6% who plan to buy their home more than a one-hour drive from where they currently reside and 5% who expect to purchase in a different Canadian province. A nominal 1% plan to buy outside of Canada, while 13% are still unsure where they will buy their first home.

“Location, Location, Location: Generation Z Trends Report” is the third report in a multi-part series based on Canada’s first in-depth study of the housing intentions, aspirations and preferences of Generation Z. The report is based on a survey of 1,502 Generation Z Canadians who are over the age of majority and between the ages of 18 and 28 in the Vancouver, Calgary, Toronto and Montreal Census Metropolitan Areas, and focuses on this cohort’s priorities and criteria for the neighbourhood and location of a first home.

Previously released research by Mustel Group/Sotheby’s International Realty Canada reported that 75% of urban Canadian Generation Z adults say that they are likely to buy and own a primary residence in their lifetime. Approximately half of urban Generation Z adults are most likely to purchase a higher-density housing type as their first home, with 25% reporting that their first home purchase will likely be a condominium, 18% saying that their first home will be an attached home/townhouse and 7% stating that their first home purchase will be a duplex/triplex. 39% reported that they are most likely to buy a single family home as their first residence. According to earlier reports, 37% of urban Generation Z adults in Canada expect to purchase their first home in less than five years, while 43% anticipate buying between five and ten years from now. 30% expect the purchase price of their first home to be $350,000–$499,999, while 26% expect to pay $500,000–$749,999.

“Previously released results from Mustel Group and Sotheby’s International Realty Canada survey of urban Generation Z adults have already revealed that young Canadians have a high level of confidence in real estate and intend on purchasing a home,” says Josh O’Neill, General Manager of Mustel Group. “This new report uncovers insights into where they plan to buy their first home, and the factors that are driving this important life decision.”

According to Sotheby’s International Realty Canada experts, surprising divergences have emerged in the neighbourhood and location preferences of different generations of home buyers as pandemic restrictions ease, and as engagement in social and community activity renews across the country. Evolving workplace and work-from-home preferences are driving new and evolving trends not only in the workplace but in housing demand, particularly amongst Canada’s youngest generation of first-time home buyers.

“During the pandemic, the desire, need and ability to work remotely influenced and enabled some Canadians to relocate to outlying suburban or recreational regions to achieve more space and a more desirable lifestyle. This helped drive record real estate sales activity across the country. While the question of work-from-home flexibility remains a defining workplace issue for the foreseeable future, attitudes about remote work amongst employees and employers are shifting as pandemic restrictions relax, and there are differences in perspectives between generations that will affect housing demand,” says Don Kottick, President and CEO of Sotheby’s International Realty Canada. “Younger Canadians are more likely to prefer a hybrid of working in the office and working from home, compared to older Canadians who are more likely to prefer remote work. Our research signals that for Generation Z, buying their first home in a neighbourhood close to their workplace will remain a top priority, regardless of whether they plan on purchasing in a major city or suburb. This has significant implications for how cities and suburbs should approach planning in order to enhance the quality of life and housing for future generations.”

Kottick cites research from the Angus Reid Institute that reveals generational differences in Canadians’ workplace preferences, with three in ten (29%) of 18 to 34-year-old adults reporting a preference to work from home entirely, compared to two in five (42%) of those over age 54 saying the same. Statistics Canada also reports that as of April 2022, 19% of Canadian workers usually worked exclusively from home, down from 24% in January 2022; however, the share of employees working at home whether exclusively or through a hybrid arrangement varies significantly across Canada’s metropolitan areas.

“As the cost of housing and the cost of living becomes increasingly challenging for young people in major cities, government, the real estate industry and the private sector will be challenged to consider Generation Z’s demands for real estate close to their workplaces, and in communities, they can afford,” says Kottick. “This may require planning for a future where jobs and office spaces are distributed beyond downtown cores and hyper-concentrated business centres in central municipalities, with smaller peripheral municipalities and suburban areas playing a more significant role in hosting both commercial and residential real estate opportunities.”

Market Highlights

Vancouver

In a metropolitan area that saw its employment rate climb to 64.4% in April 2022 as its unemployment rate held steady at 5.4%, newly released Mustel Group/Sotheby’s International Realty Canada survey results reveal that a significant percentage of Vancouver’s Generation Z adults are integrating plans for working outside of their homes into considerations for their first home purchase.

As in the case of other metropolitan areas, Vancouver’s Generation Z adults rank buying a home “close to work” as being a top priority for the location of their first home purchase, with 43% citing this as a major neighbourhood consideration, however, only 11% indicated buying in or close to the downtown core as being a priority. Neighbourhood safety is the only location characteristic to surpass proximity to work as a priority neighbourhood consideration and was reported by 54% of Vancouver survey respondents as such. Other leading location priorities include proximity to family (40%), transit-friendliness (39%), proximity to a grocery store (38%) and walkability (31%). The lowest neighbourhood priorities for a home purchase are cycling friendliness, reported by 7% as a key location consideration, and proximity to nightlife such as clubs and bars, reported by 6%.

While 36% of Generation Z adults in the Vancouver metropolitan area plan to buy their first home in a major city, 44% say that they will do so in a suburb outside of a major city. 9% plan to buy their first home in a small town, while 4% plan to purchase in a rural area. 6% are still undecided on the community type of their first home.

Survey findings also show that a significant proportion of Vancouver’s Generation Z first-time home buyers plan to remain in or close to their current city of residence: 45% plan to purchase their property in their current city of residence while 28% plan to buy within a one-hour drive. 10% will buy their first home more than a one-hour drive from where they currently reside, while 3% plan to buy in another Canadian province. 0% plan to buy outside of Canada, however, 13% are still unsure of where they will buy their first home.

Calgary

Bolstered by the revitalization of the local economy which has propelled the employment rate to 66.7% as of April 2022 even as the unemployment rate declined to 7.2%, Generation Z adults in Calgary are amongst the most optimistic of Canada’s major metropolitan markets about their prospects for primary homeownership. Encouraged by housing prices and costs of living that remain affordable relative to other major Canadian cities, 78% report that they are likely to own a home during their lifetime, with 53% indicating that they are “very likely” to do so, according to previously released Mustel Group/Sotheby’s International Realty Canada reports.

According to newly released survey results, Calgary’s Generation Z adults rank buying a home “close to work” as being a leading priority for the location of their first home purchase, signalling their expectation of working outside of the home in some capacity. 47% report proximity to work as a major neighbourhood consideration, however, just 16% indicate that buying in or close to the downtown core is a priority. Other leading priorities for a home location include neighbourhood safety (62%), proximity to a grocery store (49%), as well as walkability (34%) and proximity to parks and nature (34%). The lowest neighbourhood priorities for this generation in Calgary when buying a first home are proximity to schools, reported by 8% as being a key factor, cycling friendliness (9%) and proximity to nightlife such as clubs and bars (9%).

Calgary’s Generation Z adults are more likely than those in Toronto and Vancouver to buy their first home in a major city at a rate of 48%, compared to 37% of their counterparts in Toronto and 36% of those in Vancouver who plan to do so. 38% of those in Calgary say that their first home will be purchased in a suburb outside of a major city, 4% plan to buy their first home in a small town and 5% plan to buy their home in a rural area. 4% remain undecided.

Mustel Group/Sotheby’s International Realty Canada survey findings reveal that a significant percentage of Calgary’s Generation Z home buyers plan to do so in their current city of residence, at a rate of 48%, while 25% plan to buy within a one-hour drive. 4% plan to buy their first home more than a one-hour drive from where they currently reside, while an additional 6% specifically plan on doing so in another Canadian province. 1% plan to buy outside of Canada, while 12% are still unsure of where they will purchase their first home.

Toronto

According to newly released survey findings from Mustel Group/Sotheby’s International Realty Canada, Toronto’s Generation Z adults are not only primed for homeownership, the majority are also ensuring that their first home purchase integrates plans for a return to the workplace or office.

While the employment rate of the nation’s largest metropolitan area economy rose to 63.5% in April 2022 and the unemployment rate fell to 6.3%, newly released survey results reveal that Toronto’s Generation Z adults rank proximity to work as a top priority for the location of their first home purchase, indicating clear anticipation of their return to the workplace or office in some capacity. 46% report that buying a home close to work is a key consideration for the purchase of their first home, however, only 16% report that buying in or close to the downtown core is a key location priority. As in the case of Vancouver and Montreal, neighbourhood safety is the only location characteristic to outstrip proximity to the workplace as a priority consideration for the location of a first home purchase, reported by 56% as such. Other top priorities include proximity to a grocery store (39%), transit friendliness (35%) and walkability (35%). For Toronto’s Generation Z, the lowest neighbourhood priorities for a home purchase are cycling friendliness (9%) and proximity to nightlife such as clubs and bars (3%).

37% of Toronto’s Generation Z adults plan to buy their first home in a major city compared to 42% who say that they will do so in a suburb outside of a major city. 8% plan to buy their first home in a small town, while 3% plan to purchase in a rural area. 10% remain undecided on the community type of their first home.

Findings from the Mustel Group/Sotheby’s International Realty Canada survey reveal that a significant percentage of Generation Z home buyers in Toronto plan to do so in their current city of residence, at a rate of 40%, while 36% plan to buy within a one-hour drive. 7% plan to buy their first home more than a one hour drive from where they currently reside, while an additional 3% specifically plan on doing so in another Canadian province. 1% plan to buy outside of Canada, while 13% are still unsure of where they will purchase their first home.

Montreal

In Montreal, 79% of Generation Z adults say they are confident that they will buy a primary residence in their lifetime with 37% expecting to buy their first home within five years and 46% expecting to do so in five to ten years, according to a previously released Mustel Group/Sotheby’s International Realty Canada report. Newly released survey results now indicate that they are poised to do so with a return to the workplace and office in mind. The results are released at a time when the employment rate in Montreal rose to 63.3% in April 2022, while the metropolitan area’s unemployment rate fell to 4.8%.

Generation Z adults in Montreal report that proximity to work is a leading priority for the location of their first home purchase, signalling that working outside of the home in some capacity is anticipated by this cohort. While 50% report that proximity to work is a major location factor in their home purchase, just 17% say that buying in or close to the downtown core is a priority. Other top location priorities for a home include a neighbourhood’s safety (57%), proximity to a grocery store (38%), being close to family (36%) and transit friendliness (35%). For this generation of home buyers, buying in a cycling-friendly neighbourhood or one that is close to nightlife such as clubs and bars, rank as the lowest location priorities, with 8% and 6% indicating that these are priorities respectively.

43% of Montreal’s Generation Z adults report that they plan to buy their first home in a major city, while 41% say that they their first home purchase will be in a suburb outside of a major city. 7% plan to buy their first home in a small town, while 2% plan to buy their home in a rural area. 8% remain undecided on the community type for their first home purchase.

According to Mustel Group and Sotheby’s International Realty Canada, 38% of Montreal’s Generation Z home buyers plan to do so in their current city of residence while 32% plan to buy within a one-hour drive. 5% plan to buy their first home more than a one hour drive from where they currently reside with an additional 8% specifically planning to buy their first home in another Canadian province. 3% plan to buy outside of Canada, while 14% are still unsure of where they will purchase their first home.

The report is based on findings from a survey employing an online methodology using a robust panel of 1,502 Generation Z adults between the ages of 18 and 28. in the Vancouver, Calgary, Toronto and Montreal Census Metropolitan Areas (CMAs). The panel is maintained to be representative of the Canadian population and provide high quality data. Panelists are recruited by a double opt-in method from large databases of reputable channels using industry standards of panel quality assurance, validation, verification and best practices for panel management. The sample was weighted to match Statistics Canada census data based on age, household income and home ownership within each CMA and to bring the total sample into proper proportion based on relative populations. While margins of error only apply to random probability samples, the margin of error on a random probability sample of 1,502 respondents is ±2.5 percentage points, 19 times out of 20, and ranges from ± 4.5 to 5.4 points for 325 – 476 respondents). Data for this report series was gathered from October 25 to November 10, 2021. Please note that percentages cited may not add to 100% due to rounding.

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2

Maziar Moini, Broker of Record - Home Leader Realty Inc.

300 Richmond St. W., #300, Toronto, ON M5V-1X2